The guest commentary below was written by Jeffrey Snider, Head of Global Investment Research at Alhambra Investment Partners. This piece does not necessarily reflect the opinion of Hedgeye.

It was very cold across much of the United States in February in parts of it that usually don’t freeze up – literally and figuratively. While electricity in Texas garnered most of the attention, the weather was just as bad in many other states across the typically mild wintering South. Undoubtedly, last month was an exception to the seasons’ status quo.

|

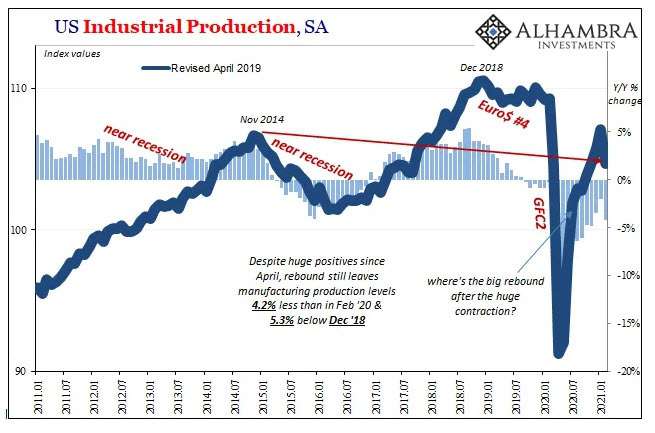

The frozen electrical grid absolutely placed a kink in the energy sector, at least, but had it caused such a disturbance that the entire national economic system quaked in its aftermath? Economists and analysts didn’t really think so, at least when setting a few of their February projections. A modest dip was thought perfectly natural, but then the Federal Reserve last week paid out much more than modesty in its updated sharply declining Industrial Production numbers (where total output is still less than it was in 2014). |

Now the central bank’s Chicago branch is piling on the downside. According to its National Activity Index, national activity in February 2021 might’ve been decidedly awful. How bad? A huge miss, down at -1.09. Even considering the cold spell in Texas, and its ice-cold electrical spillovers, analysts were still thinking the headline might only dip moderately from January’s rather hot “stimulus” overheated +0.75.

How to miss so badly? Two points on the CFNAI is like night and day, summer versus the depths of winter.

|

They are, of course, blaming “adverse weather” but it can’t just be that. The portion of the index relating to production contributed -0.85, which is atypically more severe than atypical cold, but the personal and consumption components also dragged nearly as much (-0.29 in February after adding +0.27 in January). |

Of course, the US and the rest of the global economy is already in one, so it might seem like splitting hairs. The issue is less about when the NBER might make “its” determination that last year’s contraction may have ended, or when it will end up ending, and more about the shape of recovery following its deep bottom; acceleration rather than flattening.

Such a possibly outsized stumble this far into the trough isn’t unheard of, either (see: October 1982), but unless the number really is weather-related it (like IP) gives off the impression of a less-than-full-on rebound (flat).

We already know that the global “recovery” last year lasted barely a few months – at most – before it dissipated into shrugged mainstream confusion (though still confident about inflation, somehow), and even Federal Reserve Chairman Jay Powell acknowledged the stumble also last week in his one-year anniversary whitewashing. In so doing, though, Powell said that, in the Fed’s modeled views, things are already back to rebounding again:

With the arrival of vaccines, the outlook is brightening.

|

That’s the thing with these things; the outlook is always brightening. What about some sunshine right now? Like 2018 when it painfully hadn’t, at some point the boom better actually boom in the present and not remain some forecasted dream always beyond the horizon, beyond our reach. How much brighter can it truly be if a cold spell (admittedly a harsh one) can leave such a substantial dent in the economy’s recovery(like) processes? Here we are back in 2014 again, lamenting something like that year’s unusually severe Polar Vortex which “somehow” knocked the entire global economy sideways despite the claims, by most of the same people, it was already rip-roaring its way toward, “they” said, overheating. |

Seriously, here we are with the cold weather nonsense all over again when, before 2008, economic commentary and meteorology had always related two separate, very distinct disciplines. I wrote back in April 2014 how ridiculous this was, how the attributed negative effects of that Polar Vortex weren’t attributed right at all (as the data for that period was coming in rough), they were a warning that 2014’s anticipated, fired-up economic take-off may have already been aborted:

An economy that is actually accelerating will show it conclusively across numerous and disparate economic accounts and estimates. And it will be fully insulated from snow and winter. A real recovery will not be bothered or interrupted because of a Polar Vortex, though it does offer very convenient cover to what is an obvious and durable downslope.

When the economy is really going, it just doesn’t have time to slow down for the weather or anything. And the period immediately following a recessionary trough is usually when this is the way it goes; at least historically. The post-2008 period has been curiously unusual in that fashion, too, which is why there have only been a series of “L”s rather than “V”s around the world.

|

Because it has been a planetary result, it isn’t limited to the US economy which in sentiment seems one thing (robust, strong, awesomely supported by effective central bankers and stimulus checks) though in reality is entirely something else. Sentiment (and rhetoric) right now, like 2014, is sky high; all indications about the economy, also like 2014, is that it isn’t nearly there, not yet. |

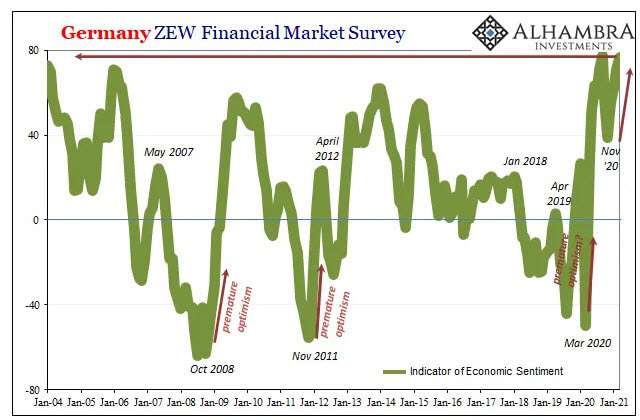

The most obvious and perhaps potently absurd example is provided by the smell of the German zoo (sorry, ZEW).

As has been the case since before COVID, all the way back to the ECB’s QE restart in September 2019, these observers in Germany keep thinking the world economy is on the cusp of firing on all cylinders while – at the very same time – confessing, month after month, year after year, how it isn’t happening nor does it appear even close at hand.

|

The ZEW’s sentiment index is supposed to be looking forward 6 months, except when the calendar eventually flips six times the economy ends up nowhere near the intended, expected hastening. This, too, is repeating post-2008 pattern of premature optimism unbacked by the underlying. I think it can get pretty cold in Germany, as well. |

The world keeps being led around by “this time”; as in, this time it’ll all work and therefore work out (inflationary). Recognizing anyway the far harsher history where the last time (all the previous “this times”) it didn’t, optimism unlike true economic resiliency somehow always dips a bottomless reservoir of faith.

Even deep wells can freeze over.

|

Right now in 2021 is when that faith is supposed to be paying off, not in the next set of forward-looking distant hopes. Instead, another poignant stumble. Everything is allegedly going right, from vaccines to government reopening to government stipends to central bank accommodations, the whole ball of wax is supposedly lined up just perfectly. |

If we’re talking the same sort of meteorology yet again in an economic context, what are we really talking about? Sentiment is great for DSGE models and media stories, but it hasn’t kept the economy warm enough when it’s really been needed.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Jeffrey Snider, Head of Global Investment Research at Alhambra Investment Partners. This piece does not necessarily reflect the opinion of Hedgeye.