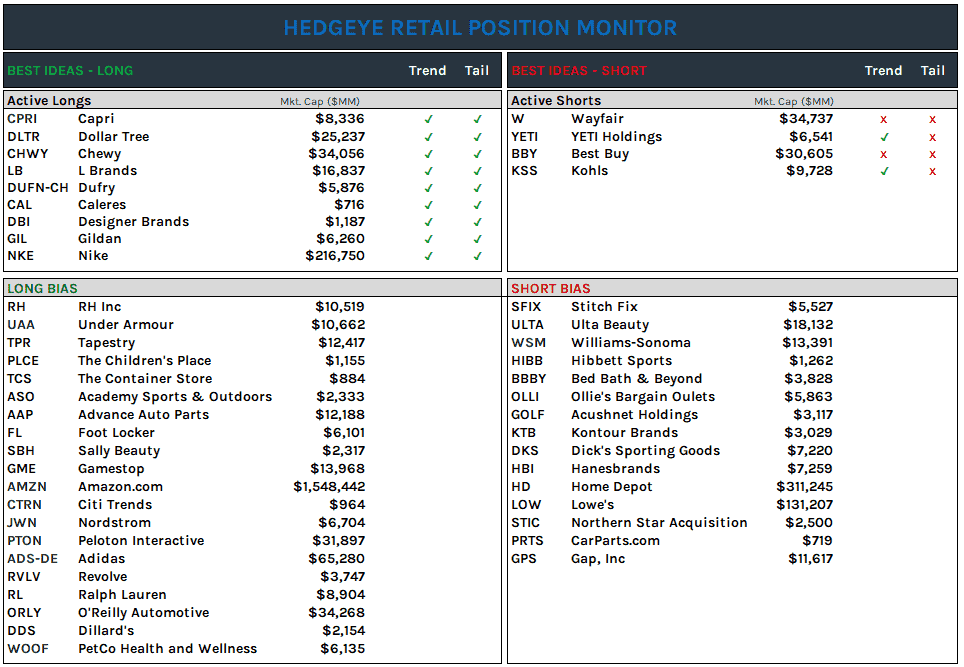

CAL | New Best Idea Long. Street Models Asleep at the Switch. Poor coverage + Stimmy + Dress FW Recovery + Renegotiate 1,100 leases + $100mm cost cuts + de-levering = $4 in TAIL EPS Power = $40+ stock vs current $18.88. The Street’s numbers are off (low) by a factor of 2x.

Signet (SIG): Removing SIG from Short Bias. We hadn’t been pushing this one short side recently, and we were wrong to add this one to the bottom of our short bias just before the pivot to Quad2. Re-vetting the call after this week’s earnings print we don’t think the timing is right for this one short side. Consumer spending has recovered faster than expected, stimulus rounds are supporting sales, and any credit risk has been pushed well out into the future given improved credit quality. Tack on the return of special occasion events and celebrations to drive jewelry demand, as well as a return of foot traffic to shopping centers, the Trend fundamental setup is bullish. Management guided Fiscal 2022 (this year) to be similar to 2019 in operating profit, and this Quad2 market seems comfortable giving that EPS number a P/E about 2x of what was assigned in ’19, currently at 15x street EPS. Though we also think there is upside to EPS numbers vs guidance. We see EPS around $4.50 to $5.10 vs the street currently at $3.92, with the majority of upside in 1H. Short interest on the name has come in a lot, but still sits a relatively high 13%. The Trend setup is net bullish, and though we think the Tail here is still bearish, we’ll wait until the setup make more sense short side to potentially re-add to our bias list.