OK…pivot here. I was cooling on NKE over the past quarter because I was too concerned that the Street’s estimates were catching up to ours and there wasn’t as much upside. But the company’s guidance on top of an extremely complex quarterly modeling cadence over the next five quarters just changed that. Score one for modeling junkies. I’d be buying NKE here. The catalyst calendar for the rest of this year is ripe.

To be clear, Nike didn’t exactly ride in on the wings of victory this quarter, as the quality of the earnings beat was absolutely horrible. It missed revenue by 6% -- which is the biggest top line miss in over a decade for Nike. Sales were down 2% in constant currency, with the top line weak in the US due to port congestion hampering product flow, and both Canada and Europe due to store closures associated with Covid lockdowns. But the company significantly lowered Demand Creation (sales and marketing expense) to offset the weak top line to put up $0.90 per share vs the Street at $0.76 and our estimate of $0.88. I can’t stress this enough… I absolutely hate when companies miss revenue and ‘save the day’ by pulling marketing or R&D out of the model. That’s called ‘over-earning’. Great companies should do the opposite – double down on R&D and branding when revenue cools. Nike just over-earned. Plain and simple. I can count on one hand the number of times I’ve said that about this company.

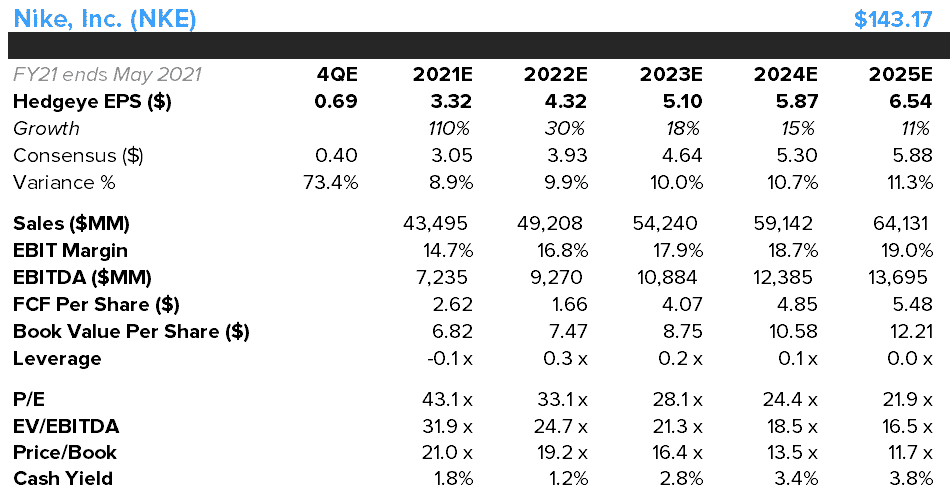

In fairness, there’s not a demand problem, as gross margins looked good -- +130bps vs last year due to strength in high-margin China (which grew by 51%), more full-price selling globally, and continued incremental shift from wholesale to digital, which was up 54% in the quarter (kind of a ‘meh’ growth rate vs 80%+ in prior 2-qtrs, and my only real fundamental knock on the quarter). Digital now stands at 21% of total sales by my math, and if you believe the management team (directionally, I do) it will be closer to 50% in 5-years. That’s a massive Gross Margin tailwind as Digital is 1,000bp gross margin accretive for Nike. In our model, we’ve got gross margins pushing 50% by 2025, driving EBIT margin to a new peak of 19% -- which is a stunning number for a company in this business. The consensus is bullish at 17% -- but not bullish enough.

Back to the quarter… On top of the poor earnings quality, management had a ‘stealth’ 25% guide down for 4Q. The press, and even some analysts, won’t pick up on that because it wasn’t explicitly stated. But the key is that Nike just set itself up for what we think will be a colossal 4Q (May) EPS beat. We’re coming in at $0.69 per share for the May quarter, but based on the annual targets the company threw out on the conference call, we think that people will back into a 4Q number of around $0.40 per share (it’s currently at $0.53). If we had to play the higher/lower game on our $0.69 – we’d go higher, as the underyling momentum in the business and the pent-up demand could make revenue double in 4Q vs mgmt guide of 75%.

The stock is only down 3-4% in after-hours trading, which shows the love affair that people have with this company, and the stock. Nike is trading at its highest multiple of earnings, EBITDA, Sales and Free Cash Flow in history, the Old Wall Buy rating ratio has never been more bullish in the history of the company, and less than 1% of the float is shorted – a historical trough. From a valuation and sentiment perspective, this name is priced for perfection, and this quarter was far from perfect. I’d like to say ‘buy on weakness’ – tho I can hardly call -3% weakness. But I will keep NKE on our Best Idea Long list into what I think will be a sharp upwards revision cycle starting with the next quarterly print. Then we get the product hype around the Olympics – when Nike usually trades well and is front and center with the consumer – just in time to put up a year of what I think will be 30% earnings growth – well above the Street’s 18%. Simply put, Nike is expensive, and it should be.

Over a TAIL duration, if our 19% EBIT margin is right, we’re looking at $6-$7 in EPS power on top of a bullet proof balance sheet. And while I won’t argue multiple expansion from the current 43x pe, I think you get paid here by earnings growth alone. The margin and return characteristics coupled with the direct control of the Brand will more closely resemble a luxury goods company than a company that sells kicks at Foot Locker. So 40x $6.50 gets to $260 – discounted back to a 12-month value suggests a $192 stock in a year. While I think there are other recovery names that offer up a better return profile, I’ll definitely take Nike’s upside – especially given how I think the catalyst calendar will play out over the next year.

-- McGough