Conclusion: We continue to see weakness in the consumption trends when government spending is stripped away. Slower growth is likely going forward.

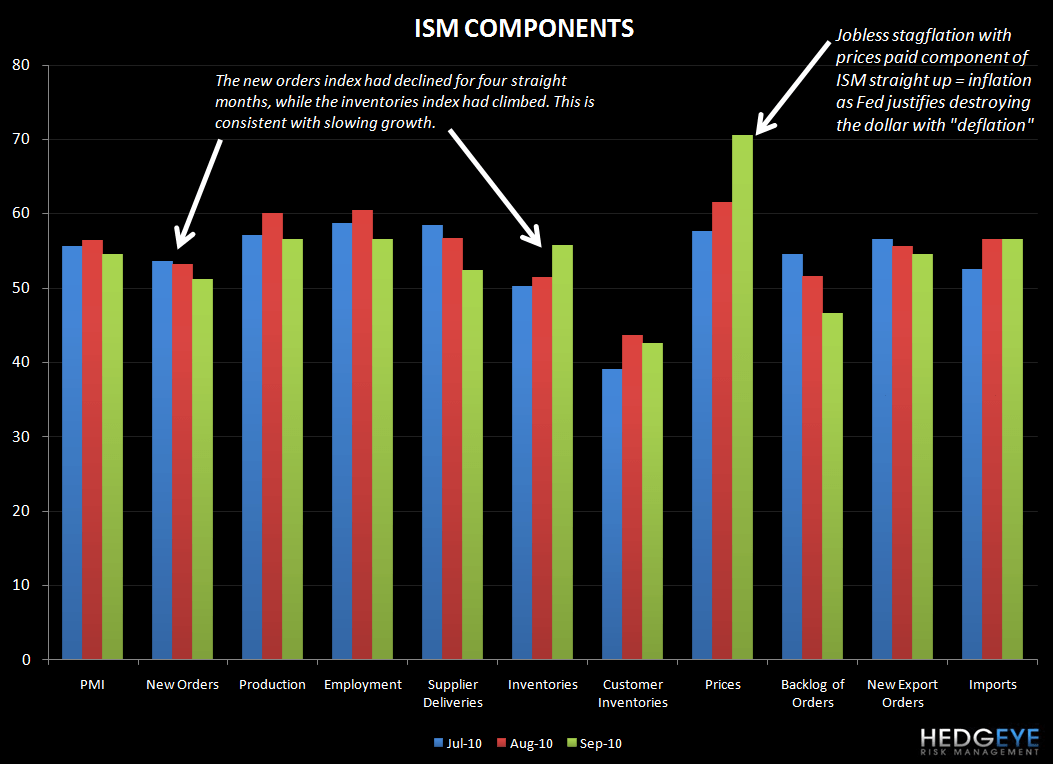

Commerce Department figures released today show that consumer spending rose in August while ISM and consumer confidence data have flashed to the downside in recent releases. See our conclusions below and a chart of ISM component shifts in the most recent months.

INCOME - Consumer spending in the U.S. rose 0.4% in August; the gain exceeded the 0.3% increase projected the Bloomberg consensus. Incomes were up 0.5%, the biggest advance this year (propelled by the incorrigible hand of Washington). Transfer payments jumped 1.6%, indicating that the government’s crutch is still a core factor in this “recovery”.

Hedgeye conclusion: there will be a rocky road transitioning from the government supporting consumer spending to the “real” economy.

ISM - The ISM print was better that feared, still growing in September, but at the slowest pace in 10 months. The I SM factory index dropped to 54.4 from 56.3 in August. Bloomberg consensus forecast a decline to 54.5.

Hedgeye conclusion: A sequentially lower ISM print in October is likely.

CONFIDENCE - The University of Michigan final index of consumer sentiment fell to 68.2 from 68.9 in August, but up significantly from the preliminary reading of 66.6 issued last month.

Hedgeye conclusion: Maybe there was a fat finger in Michigan! The bottom line is that confidence is not improving, but people are spending more thanks to gifts from Washington.

Howard Penney

Managing Director