We've amped up our research efforts around Dufry (DUFN-CH, ADR=DFRYF) since first going long last month on 2/6 (at CHf 52) , and are convinced that this name is the Mother of all Reopening plays…and then some. Click Here for our note outlining our original Long call on the stock. Today we're adding the name to our Best Idea Long list, and despite the 23% gain since we first made the call, we think this name is a 3-bagger over 3-years, with many ways to win. We think that (Advent and Alibaba-backed) Dufry will prove itself to be the consolidator of the global luxury travel retail industry, and will put up earnings nearly 2x pre-pandemic levels over a TAIL duration. That's definitely not in the stock today.

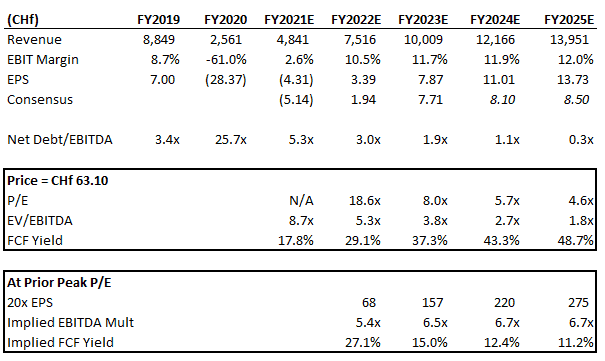

The Elephant in the room is that current financials for DUFN look simply atrocious. After all, this is a travel-centric stock and travel has come to a standstill. 2020 sales (reported last week) were down 71% and the company lost CHf 28 in EPS -- not good when you’re sitting on CHf 4.5bn in (recently restructured) debt. Clearly anyone investing in DUFN today has to look through a lot of turmoil in the numbers as they exist today.

But at today's CHf 63.50 price, you're buying the name at sub-5x earnings, 2x EBITDA, and a ~40% FCF Yield. Simply put, it's a business that is moving upscale much the same way RH is building a global luxury home furnishing brand, but this business has the benefit of a) customers that are literally locked in the store for an hour, b) ZERO Amazon competition, c) being a globally diversified monopolist in each market in which it operates across multiple retail formats. In other words, it's a dominant travel retail luxury consolidator with fierce barriers to entry that is trading like a poor quality beaten-up share-losing US apparel retailer. The economic disconnect between where the stock is trading and the ultimate value we expect Dufry to create is astonishing.

We've developed an exhaustive model on the name over the past six weeks, which is critical for our research efforts given the complexity of the company, and think that both the top line and bottom line recovery will be faster than the consensus thinks.

We're going to present our multi-faceted case on Dufry in a Deep Dive Black Book on Tuesday, March 30th at 10am. Dial-in and video information to come.

Aside from pent-up demand from the Leisure traveler globally, we think that Dufry will win incremental concessions as a) municipalities increasingly put airport operations into the hands of private operators who want/need to develop a luxury shopping experience for a captive customer, b) the local undercapitalized mom and pops that control 90% of the global market increasingly look for a way out given the devastating impact of the travel slowdown during the pandemic, and c) Dufry upscales its portfolio into more luxury boutiques and malls which not only takes up its margin structure, but also makes it a more attractive acquisition target for the likes of LVMH and Kering, both of whom we expect to be more acquisitive post-pandemic.

Keep in mind that it's doing this on a streamlined cost structure as Dufry is cutting CHf400mm from its cost base. Another factor that US investors don’t appreciate is that with 40% of the business in Europe, the company is subject to significant restrictions around laying off employees under virtually any circumstances. But with the pandemic, most of Europe relaxed employment standards allowing companies like DUFN to adjust costs to match revenues. This is a company that was largely built through a series of acquisitions and is anything but lean. This cost-cutting program is good for 400-500bps in margin or about CHf 4.00 in EPS – notable given that it was a 3%-5% margin business pre-pandemic.

In addition, we think that the Street's numbers are egregiously underestimating the growth that the Dufry/Alibaba partnership will yield in the Chinese market, which we have going from 6% of the mix today to 22% within five years. This partnership should yield an incremental CHf 400mm in EBIT over a TAIL duration -- or CHf 4.00 per share. Keep in mind that pre-pandemic this company was earnings CHf7.00 per share, and the addition of this partnership is likely to be accretive to EBIT by ~60% by year 5. The cost cutting program and the Alibaba deal alone (combined = CHf 8.00 in EPS) gets us above pre-pandemic earnings. In the end, we're getting near CHf14 in EPS by year 5 of our model.

If we're breaking through historical peak 8% EBIT margins, we think it's fair to at least test DUFN's historical peak earnings multiple of 20x. While that leaves little upside based on its current depressed earnings base, it adds up quickly by the TAIL end of our model. If our model is even close to being right, this stock is going to double, and then double again over a TAIL duration.

Full details around our thesis and our model to come when we present our deck on March 30 at 10am.