FINL’s earnings of $0.31 after the close yesterday came in considerably lighter than consensus estimates at $0.35 causing shares to trade sharply lower in the aftermarket. After taking a closer look at the numbers, here are a few notable callouts ahead of the company’s call this morning:

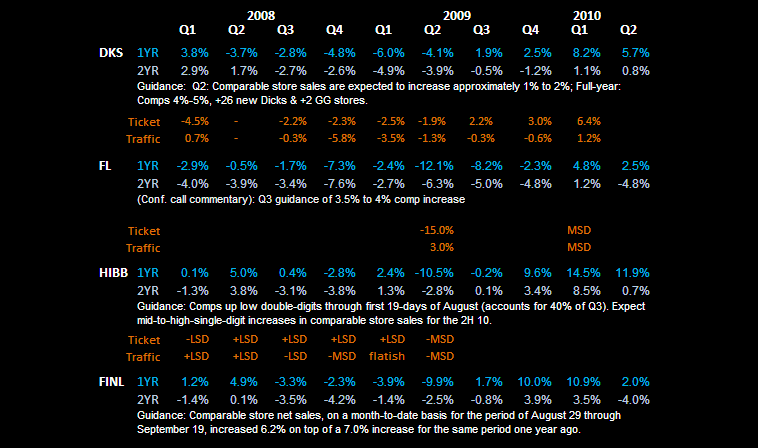

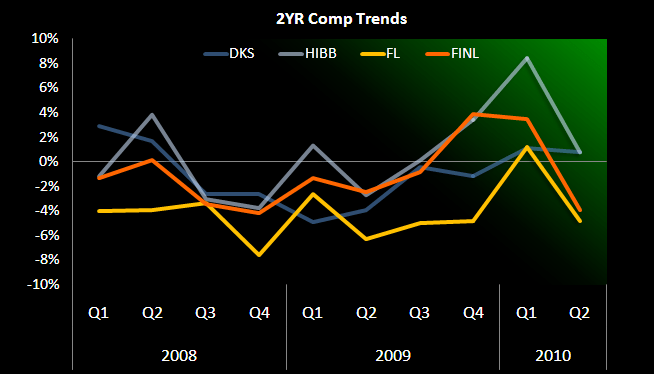

- Top-line growth of +1% marked a clear divergence between on and off-mall players in the space with both DKS (+9%) and HIBB (+14%) posting solid numbers while results out of FINL and FL (-0.3%) lagged their off-mall counterparts considerably.

- Inventories down only -2% relative to +1% sales growth resulted in the most significant SIGMA turn in the space following several quarters of significant reductions in inventory. Similar to top-line trends, within the four company peer group, Q2 was evenly split between those building inventory (DKS +4% & HIBB +2%) versus those reducing inventories (FL -5% & FINL -2%). While top-line trends lagged for mall-based players, inventories remain tighter. With sales in August and into September improving materially, this is a good scenario and likely to continue to keep promotional activity in check.

- The comp (+2%) is reflective of just how soft Q2 was during June and July. Additionally, while the early read on Q3 was positive with comps up +7% in the first 3-weeks of June, it’s important to consider that comps were considerably more difficult on a 1-year basis due to the timing of stimulus checks in ’08 - see the monthly comp trend table below. Comps up +6.7% on a +7% comp in the same period last year so far through September 19th is consistent with what we are seeing in weekly data trends.

- Footwear comps up +2.0% were in-line with softgoods comps up +2.1% in Q2.

While comps are catching our eye once again, we are confident that industry weakness in June and particularly July was the primary cause of a weaker comp relative to consensus expectations. We’ll have additional color after the call at 8:30am EST.

Casey Flavin

Director