European restrictions lead to Q4 miss (TAP)

Molson Coors reported Q4 EPS of $.40, missing consensus expectations of $.77 by a wide margin. Constant currency sales decreased 8.3%, worsening from -3.6% in Q3. Management said, “Europe alone accounts for 92% of our fourth quarter topline [miss] to plan.” Government restrictions in Europe and the U.K., in particular, caused the shortfall. Europe accounts for 15% of revenue but contributed 61% of the revenue decline for the year and 92% for the quarter. North American sales decreased 0.8%, even with Q3, while volumes declined 6.9%. The U.S. grew 1.9%, with volumes down 6.2% compared to shipment declines of 2.3%. In Europe, revenue decreased 39.4% in constant currencies worsening from -15.3% in Q3. EBITDA of $375M missed consensus expectations of $481M.

The company’s tall can supply returned to normal. The company has shifted its innovation and growth initiatives to its challenging seltzer portfolio consisting of Topo Chico, Coors Seltzer, Vizzy Hard Seltzer, and Proof Point. It has also added distribution of Yuengling in the West, Zoa (non-alcoholic seltzer), Hexo (cannabis drinks), and La Colombe (coffee drinks). The core beer business remains in secular decline that is accelerating from hard seltzer share gains. It seems management understands the challenges for its brands and has partnered with several smaller brands for help, offering innovation distribution. The on-premise business will get a lift when vaccines allow governments to lift restrictions, which will give the company a reprieve for a year. Management guided 2021 revenue to grow MSD%, and EBITDA growth is expected to be flat. The EBITDA miss in Q4 and guidance were both worse than we modeled. TAP is on our short bias list.

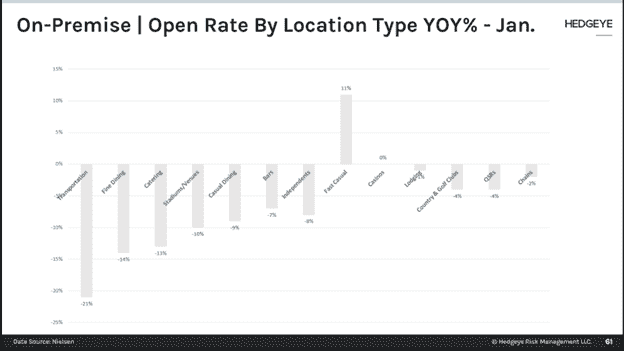

On-premise open rate differs by location (SYY)

In nearly three-quarters of the states, bars and restaurants have reduced capacity limits in place due to the pandemic. Not all on-premise sectors were impacted the same. The hardest hit is the transportation based outlets like bars and restaurants inside airports and other terminals. 21% of transportation based outlets remained closed in January 2021 compared to the prior year. Fine dining’s open rate is 14% lower, while fast-casual is 11% higher. The open rate for casual dining is 9% lower, while QSRs are 4% lower. Independents are 8% lower, lagging the chains that are 2% lower. Benefiting from the shift away from on-premise, off-premise retailers saw a 17.9% or $13.5B increase in sales in 2020.

The beer category has a strong January (SAM)

Off-premise beer category sales increased 15.7% in the YTD period ended January 23, according to Nielsen. Hard seltzer sales accelerated slightly to 88% growth from 84.3% in the previous four week period. White Claw sales grew 39.9%, and Truly sales grew 132%, while Bud Light Seltzer grew 307% in the four week period. Imports grew 17.5% YTD, craft grew 19.4%, domestic super premiums grew 18.5%, and FMBs ex seltzer grew 18.5%. Boston Beer’s Twisted Tea grew 51%, while Samuel Adams grew 5.2% over the four week period.

The National Beer Wholesalers Association’s monthly Beer Purchasers’ Index (BPI) was 66.4 in January, up from 64 in December. A reading of 50 or higher indicates expansion, while below 50 indicates contraction. The FMB/seltzer segment had a reading of 90 in January, up from 80 in December. Premium lights and imports were both at 59, down slightly from December. The contracting segments include 48 for premium lights, 43 for craft beer, 35 for cider, and 45 for below premiums. U.S. brewers shipped 5.2% more beer volume in December.