Two changes to our Position Monitor this week...

GOOS: We’re punting Canada Goose (GOOS) from our Long Bias list. In July we pivoted from short to long GOOS given our view that management was making the right decisions as it relates to distribution and brand segmentation, and near-term expectations were rightsized to the point that would likely lead to earnings upside. For a couple of months, that held true. But our sense is that sales this holiday aren’t exactly knocking the cover off the ball, and are likely to exacerbate the company’s finished goods inventory, which has been a problem for Canada Goose for much of the past two years. The stock is up 32% since our Long pivot vs 15% for the S&P – and while we’ll hardly consider that a big win, we think the stock is back to a point where an unexpected inventory bloat matters again – especially with short interest testing 2-year lows. We don’t think it’s an outright short here at $30, but we see the risk reward as fairly balanced. Definitely not a long with the current setup.

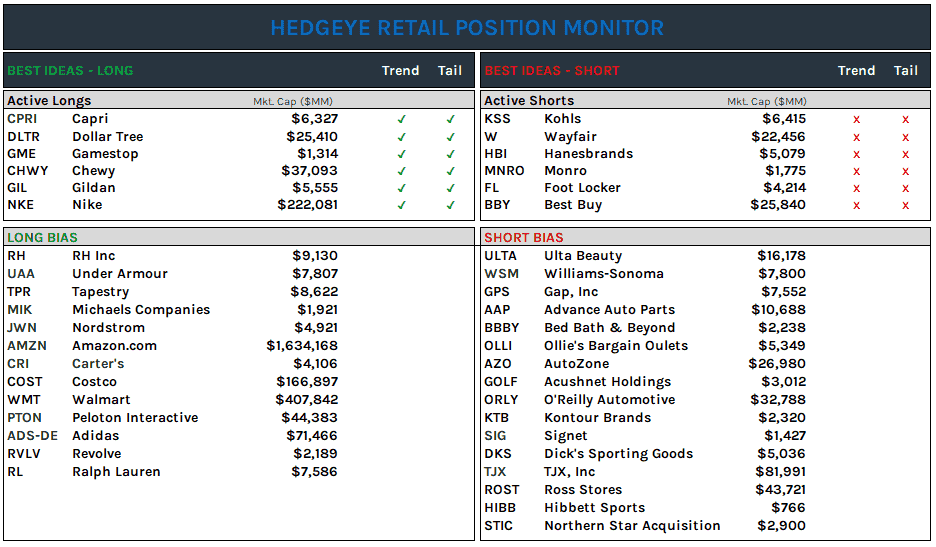

STIC/BARK: Adding Northstar Acquisition Corp/Barkbox to short bias. Barkbox is coming public via SPAC ticker STIC (to become BARK). The original deal value was at $1.6bn citing an attractive valuation to peers like CHWY, which we think is flawed logic. Merger is planned for 2Q21. The current SPAC ticker is trading at $14.50, implying ~$2.9bn cap at 202mm proforma shares outstanding. BARK not profitable on adjusted EBITDA even within the 2020 online marketplace where demand/customer acquisition came at historic low costs and growth ramped across nearly every ecommerce business. The EV to this year’s sales is about 4.3x. The comparison to CHWY on valuation is misguided. CHWY is building an ecosystem to serve and sell pet owners any goods or service they might want for pets. Barkbox is mainly a subscription of a monthly box of stuff you may or may not want. It makes sense that it saw accelerated growth this year as the pet category accelerated in 2020 and the shift to online consumption accelerated as well. But the addressable market and sustainable profit opportunity is nowhere near that of CHWY. The model would more closely resemble BirchBox, which runs a similar subscription sample box in beauty. BirchBox tried to sell itself in 2018 reportedly shopping itself to Walmart and QVC. Nobody wanted to buy it, Viking global ended up taking a majority stake with an incremental $15mm on top of its prior ownership. The Barkbox presentation is missing some important details around churn, cohort performance, and customer lifetime value that would be important to assess whether this company has a chance to continue its growth path and whether it can ever generate profits anywhere close to the levels needed to justify this valuation.