Below is a chart and brief excerpt from today's Early Look written by Industrials analyst Jay Van Sciver.

|

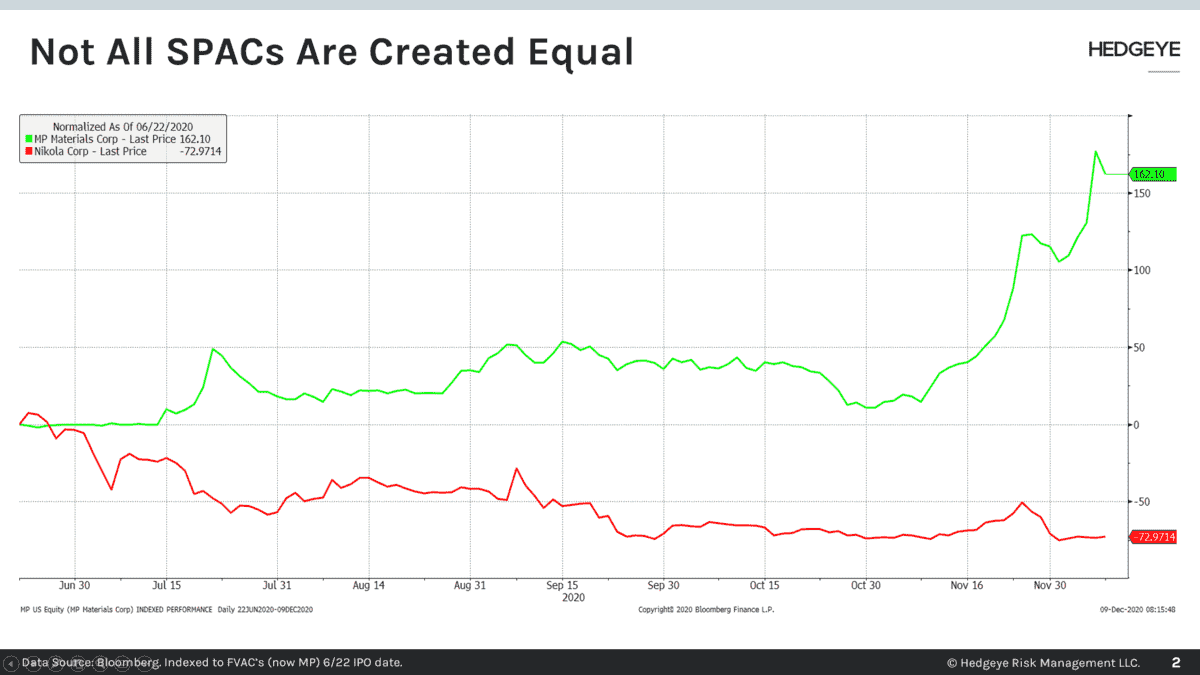

It is worth reviewing the SPAC process. When a SPAC raises money, buyers get an asymmetric deal: you will like the merger the SPAC finds, or you can get your cash back. Once the SPAC finds a deal, there is a ‘vote’ that is largely a pre-ordained ‘YES’. A key for the sponsor and target alike is to have a share price over that ‘cash back’ redemption price heading into the redemption deadline, typically >$10. This is a period of uncertainty and ambiguity, often providing the best entry opportunity. Weak longs keep the share price closer to the redemption price; after all, if those weak longs are willing to take their $10 back, they’d certainly rather sell in the open market at, say, $11, especially as the optionality fades near de-SPAC. The best performance period for SPACs is often the few weeks after the merger closes. Weak holders have exited; the remaining shareholders chose to remain. Ambiguity and uncertainty collapse into a uniform desire to promote the newly public company. The SPAC gets a shiny new ticker, an industry designation, and a much larger market cap. Institutional investors see it dumped into their ‘universes’ and ‘benchmarks’. Options may become available, or at least become more liquid. This confluence of positive changes generates upward pressure, typically during 3 to 4 weeks of often wild trading. |