August was better month than expected for those keeping the same store sales score. The reality of the underlying results however, is that demand doesn’t really appear to be changing, better or worse. There are a couple of key takeaways to be mindful of. Across the board, when given a reason to shop, the consumer appears willing to spend. This applies to August in a couple of ways. First, as it pertains to back-to-school and back-to-college. Retailers across the board with exposure to this event cited on plan or better results so far in this key (but drawn out) selling season. Is this enough to propel the quarter to upside on its own? No, but it clearly demonstrates the consumer still has the propensity to spend when given an “event” or reason to do so. Secondly, those retailers with improved or new products are seemingly able to drive sales as well. Case in point is Limited Brands. The company’s focus on new product introductions at Victoria’s Secret coupled with heavy marketing were key in driving above-plan and above-expectation results for the month. Monthly innovation in the bra space is working, hands down.

Unfortunately, today’s results don’t really enhance clarity or visibility as we look out towards the remaining months of the year. The back-to-school season, while off to a solid start, is also inherently volatile given the large amount of variables impacting mom’s decision to shop. Here’s what we know. In areas where school is already back or close to it, demand has been stronger. Yes, this another sign of consumers buying close to need. In states with tax-free events response has been strong. Keep in mind that these events inherently create volatility and pull demand forward in some cases. Promotional activity was frequently cited as “aggressive” or “high”, which should not come as a surprise, especially when it comes to teen apparel. Regional trends are mixed, likely influenced by the timing of when kids return to school. California and Florida (areas with the easiest compares) were mentioned positively by several retailers, although this is a trend that has been underway for several months now. Finally, the weather was not a help this month. Extreme heat has in some cases put a damper on early sell-through of Fall apparel. It has also helped those that still have some Spring/Summer goods left (i.e. shorts, tees, and sandals). For the most part, almost every retailer at this point is hoping for a cool-down.

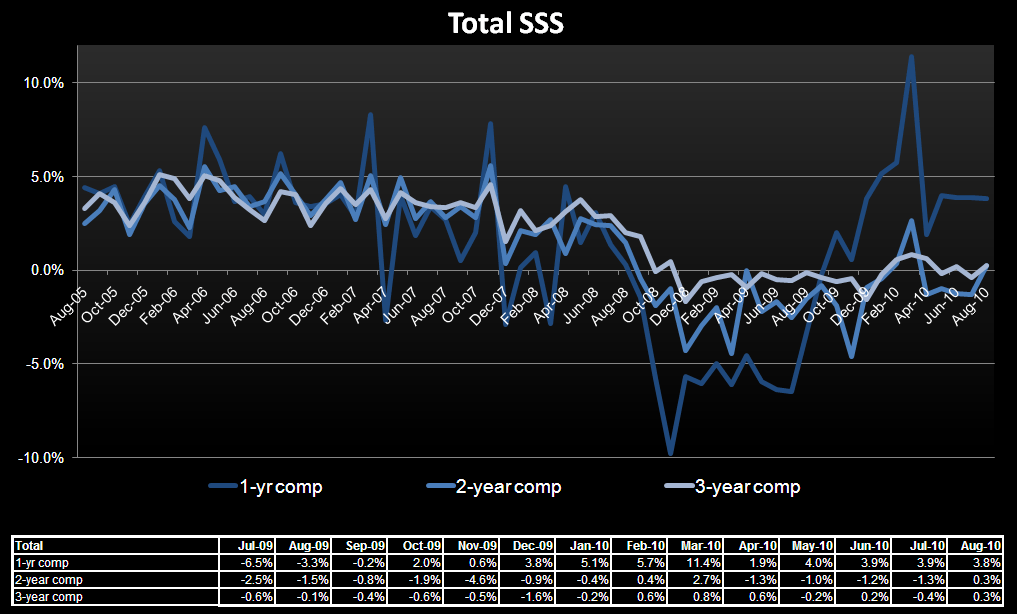

Bottom line, when we look at our monthly same store sales index, it remains stuck in a sideways trend. The 2-year monthly industry comp did tick up sequentially to 0.3% from -1.3% in July, but the range of monthly results still hovers around flat. With earnings reports now complete, guidance reset, and expectations generally tempered, it’s no surprise that these results appear to be optically better than one would expect. The reality is that underlying sequential demand remains essentially unchanged, at least if you’re using same store sales as a way to keep score.

Additional company callouts:

- Hard to believe but AEO noted a strong response to key back-to-school categories including knit caps, denim, and sweaters. Sounds like their customers must be stocking up or are completely oblivious to the heat.

- ARO noted that stronger results were reported in peak back-to-school regions, mostly in the South and West. As a result, management also expressed that it believes consumers are shopping closer to need.

- Costco noted that TV sales remain under pressure, with both unit and sales comps declining by mid single digits for the category in August. On the positive side, softlines were a big positive divergence for the month and increased by a mid-teens percentage. Key drivers of this business were housewares, home furnishings, domestics, jewelry, and men’s apparel. On the inflation front, average sales prices for meat were up mid single digits and produce was flat y/y.

- Gap noted that the company’s current Black Pants merchandising effort in women’s was a key performer in the month. For men, khaki’s and woven shirts were top categories. Baby and kid’s overall outperformed adults.

- JC Penney noted that back-to-school sales performed well during the month, led by strong double digit increases in sales of backpacks. Similar to other retailers, JCP also noted that sales were stronger in regions with earlier back-to-school start dates indicating purchases are being made closer to need. While still early in its turnaround process, the home category was cited as having a positive performance online in the home category. Recall that JCP’s online biz is about 50% home related.

- Kohl’s noted consistency within its monthly results. All regions and product categories produced positive increases for the month. Home was the strongest category, increasing by high single digits. The Southeast region also outperformed, increasing by double digits. Kohl’s also showed a notable increase in transactions, which increased by low double digits.

- Nordstrom highlighted jewelry, dresses, and women’s shoes as leading categories for the month. August also marked the 12th month in a row of traffic increases for the department store retailer.

- Ross Stores continues to highlight dresses, home, and shoes as leading categories for the off price retailer. All three categories produced sales increases in the low double digit range.

- Limited noted that is has been and will continue to be less promotional than last year. The company is eliminating a Fall sale even this year and continues to see substantial merchandise margin improvement as a result of less clearance and promotional activity.

- Target noted continued strength in its food categories, registering an increase of low double digits for the month. Other above-average categories included health and beauty, men’s apparel and women’s apparel- all of which increased by mid single digits. Electronics were cited as a weaker category for the month (similar to prior months).

Eric Levine

Director