PSS reports this Wednesday. They're gonna miss. I know it. You know it. Anyone else that's bothering to look at the retail tape this week knows it. I'd love to end this little intro with "...and Mr. Market knows it too." But that would be a JV mistake I simply won't get sucked into.

There's only one time in the many years I have tracked PSS that I have seen sentiment worse -- and that's just after PSS levered up to do a dilutive deal about a week before the credit crisis began. Fast forward a couple of years, and the deal has proven to be the right move. The acquired business has more than doubled, debt to EBITDA is down to nearly 1x, and the cash flow in the business today (even with the core struggling) is ample enough to buy back 15% of the stock.

So let's step back a minute and drill down on what's really wrong. I could argue all day about valuation, and that the sum-of-parts math suggests that the market is only paying 2-3x EBITDA for the base business. But the reality is that the bear case that has frustrated so many people over so many years finally has some teeth. There's finally the 'I told you so' factor. And that, of course, is that the core business can't comp, the business is overexposed to Asia from a sourcing perspective, and at face value it is tougher to model the earnings upside that used to exist in the models of many.

Let's look at the facts…

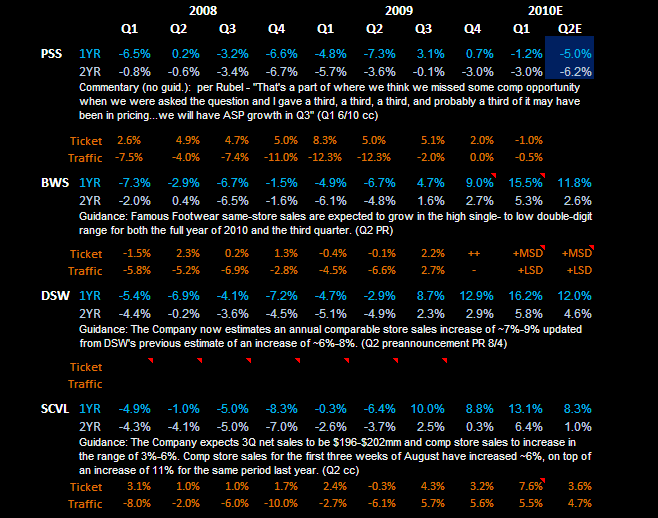

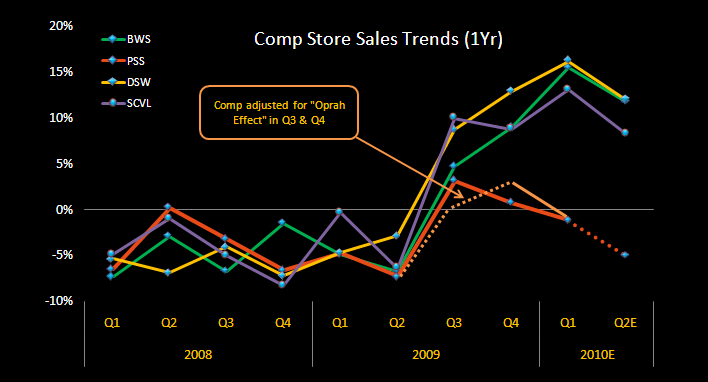

1) Not only did PSS undercomp its peer set by about 500bps over the past three quarters, but in the latest quarter, the trajectory of the comp diverged meaningfully (to the negative side).

2) A perplexing trend has emerged. When consumers trade up (and we see higher-end retailers do well), PSS has not benefitted in its mix or price. But as consumers trade down (and Dollar Stores and Discount Stores score) we’re not seeing Payless participate.

Now…there are some offsetting factors over the past year that need to be considered.

A) At this time last year, PSS’ back-to-school push was aggressive – big time. The company went in with a $7-$8 intro price point at the same time Wal-Mart started to get out of footwear. PSS upped its SG&A and went on full offense. Unfortunately, it didn’t work. The reality is that the consumer was in a spot where they weren’t going to show up – regardless of price. So PSS either ‘over-SG&A’d’ or under-priced. I’d argue the latter.

B) As it to relates to trends, keep in mind that the PSS model differs from most peers in that its proprietary brands very rarely – if ever – catch a fashion trend when they are on the upswing. PSS will usually benefit when the trends explode into the mass market and crush ‘em on price. Last fall and winter, it was short on boots. Early this year it was late on Toning. Same thing with Sandals a couple years back. There’s a couple of sub-themes here…

- Expect broader distribution of boots at PSS this fall. It’s about 6%-8% of the PSS mix, and carries about 2-3x the average price point.

- Same for Toning. It will go from 1% of business early this year to 5-6% by 4Q at a $29.99 price point. Our sense is that this business is already above plan.

C) Why A Late ‘Trend-Catcher’? It’s perfectly fair to question why PSS should be late in catching trends. One reason is that the company took the percent of proprietary brands up by 3x over 5 years to almost 75%. With in-house R&D teams instead of third-party sourcing, the lead time requirements grow, short-term flexibility declines, and the risk factor in being wrong on product goes up materially. I think that this is why PSS has been so tight with inventory (and Gross Margins have steadily been heading higher) as having increased product risk AND inventory risk layered on top of that is a risky game that no retailer in their right mind wants to play.

We can debate the facts, but one thing that’s unquestionable is that PSS is at a key point in its decision tree. Management needs to think outside the box on this one.

1) Does this mean that Payless increases its outside brand exposure – in effect reversing what has been part of the bull case on margins for 3+ years?

2) Does it start to produce ‘take-down’ versions of Saucony and Sperry to sell at Payless stores (kind of like how Nike and Polo both design and sell certain product into Kohl’s)?

3) Does PSS need to step back and really ask itself if it needs 4,800 stores? If the answer is Yes, are they in the right locations?

4) Does the low-income consumer really care one way or another about trading up to better brands at a place like PSS?

I don’t like to say this often, but I’m not certain what the right answer is -- yet. The only thing I am certain of is that something meaningful must change. That makes this one of those ‘trust management to do the right thing’ stories. Everyone will have their own opinion there, but again, let’s look at some facts. Just 3 years ago, the big question was around Saucony and Sperry. Check out the following.

A) At the September 2008 analyst meeting, Saucony and Sperry had combined revenue of about $250, and Matt Rubel said that they should be $500mm combined by 2010. Today, they exceed $500mm (my math is $550ish). Over this time period, the business went from 7% of revenue to 15% today.

B) As it relates to profitability, the leverage is clear when the revenue doubles on the fixed-cost portion of the business. Translation = Saucony and Sperry went from 5.5% of EBIT then, and is around 20.5% today (based on our math).

C) Recent trends have been solid, to say the least. Saucony continues to gain share aggressively, with growth coming specifically from the Specialty Running channel. As it relates to Sperry, trade shows are showing more strength in boat shoes for Spring. But more importantly, at the recent Atlanta Shoe Market in mid-August, buyers noted frustration that the brand was only accepting ‘futures’ due to ‘overwhelming demand.’

I’m not highlighting this to justify that there’s another part of the business that’s doing so well and that we should ignore the other 80% of cash flow. But in what I outlined as a ‘trust me’ story, these guys rank pretty high on my ‘give them the benefit of the doubt’ list. They’ve earned it.

We’ll hear Matt Rubel give his take on this at the Analyst Meeting in October. Until then, we have a sloppy print next week, extremely poor sentiment, what’s likely to be a downward earnings revision, and pretty much nothing else for people to get excited about on this name. Furthermore, there’s no doubt in my mind that we’re about 3-4 months into a major shareholder rotation, which will probably take us through year-end.

Do I think that Saucony and Sperry alone are worth $10 per share today? Yep. That suggests that the 4,800 chain, licensing business, and potential growth if the team gets this right are all worth about $3.50 per share, or $625mm if we give all the net debt to the stub. This thing is cheap on almost valuation metric possible. But I realize that that’s not enough if you’re looking at the next month.

But I think that by year-end, we’ll have a better mix AND pricing on the base business, continued growth success in PLG, a more clear strategy that the newer shareholder base can sink its teeth into, and most importantly – a roadmap that $2.50 in EPS is a reality.