NOMD’s investor day sets an achievable five-year goal

Since being founded five years ago, Nomad Food’s first investor day set an EPS target of €2.30 by 2025. The growth formula (depicted in the chart below) begins with LSD% organic sales growth with modest margin expansion driving EBITDA growth of MSD% plus cash deployment through acquisitions and share repurchase. Over the next five years, the company expects to generate €1.5B in cash.

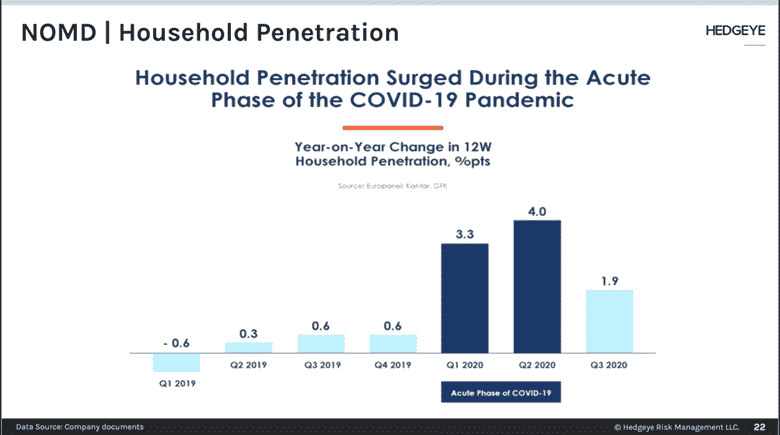

The three drivers of growth are the category tailwinds for frozen food, scaling the brands across multiple platforms, and the development of Green Cuisine in the plant-based protein category. Two-thirds of households across all of Nomad’s markets purchase their brands every year. During the pandemic, consumers purchased more of Nomad Food’s frozen brands. Household penetration went from 0.5 points to 4-5 points during the pandemic's peak, as seen in the following chart. Even as restrictions have eased in Western Europe, penetration levels continued to grow above pre-pandemic levels. The company’s goal is to retain 25-30% of new users in 2021. Online grocery sales have also been a tailwind during the pandemic. Online sales have increased from 5% to 8%. Frozen food over indexes online (likely due to fewer spoilage concerns), and brands outperform online. Green Cuisine’s market share is now 7%, and it is the third best selling plant-based brand in the U.K. The plant-based category is also growing, up 26% in 2020.

A 15 to 20x multiple on $2.72 (€2.30) would represent a future target share price range of $40-54. That represents some multiple expansion for a company that has not yet received proper credit for 15 consecutive quarters of organic growth and successfully integrating acquisitions.

Grocery Outlet’s comp slow (GO)

Grocery Outlet reported Q3 EPS of $.50 vs. consensus of $.23. SSS increased by 9.1% vs. consensus estimates of 8.7%. Gross margins expanded 40bps, 20bps higher than consensus estimates. SG&A expense slightly deleveraged. Inventory increased by 16.8%, slightly more than the COGS increase of 15.4%. As we noted previously, the company will start to grow the store base on the East coast with 3-5 planned in 2021.

Shares are indicating lower this morning due to the sales deceleration in Q4. Management’s guidance is for SSS to be up MSD% for the rest of Q4. We think there are several reasons behind the sales underperformance compared to the conventional grocers, which we currently estimate to be ~4%:

- Grocery traffic trends in California lag the rest of the country. Management said the deceleration in Q4 was from basket size and not traffic.

- Conventional supermarkets are benefiting from being a one-stop grocery destination. As vaccines are distributed and consumers increase their shopping trip, the trend favoring conventional supermarkets will reverse.

- Online sales contribution. As a close-out retailer Grocery Outlet has not pursued e-commerce due to inventory management complexities and the inherent sell-out nature of close-out deals. This causes Grocery Outlet to miss out on a comp boost but avoids the margin drag.

Despite looming restrictions, U.K. grocery sales decelerate slightly (NOMD)

Kantar reported take-home grocery sales in the U.K. grew 9.3% for the 12-week period ended November 1. In the four-week period ended November 1, sales grew 9.4%, decelerating from 10.6% in the previous four-week period. The growth rate was highest in Wales, where restrictions were tightest, up 15%. Wales had its “firebreak” restrictions from Oct. 23 through Nov. 9. In England, new national restrictions took effect on November 5 and will extend until December 2. Frozen food was the strongest category, growing 14% in the 12-week period. The UK is Nomad Food's largest country by sales, representing 31% of overall sales.