Overview

We expect ONEM to report strong results after the close today. As we’ve been highlighting in recent weeks, there are several ongoing tailwinds.

Several sources have indicated flu vaccinations have been very strong so far in 2020, which we have also seen in ONEM’s Claims Index data. Flu vaccinations are positive for ONEM visit trends in their own right, but also are likely to come with additional services at the time of the visit, and boost Net Patient Service Revenue. We have also seen a solid pace of provider growth throughout the quarter as well as a positive app download trend. Both of these indicate that reported membership is likely to come in well ahead of guidance and consensus.

Based on the provide and app trends, we expect membership could be well ahead of their full year 2020 guidance of 505K-515K, not just ahead of the 486K-496K guidance range for 3Q20. We expect revenue to come in at close to $90M for 3Q, slightly ahead of the high end of the guidance range. The company has not given full year 2020 guidance beyond membership.

ONEM’s membership number is a significant metric because it is the clearest indication of the longer term opportunity for ONEM in their markets. Our analysis shows ONEM has captured a high single digit market share in their core markets of New York City and San Francisco, but only levels ~ 1% elsewhere in their network. Upside to the membership in 3Q20 offers a credible path to future membership at levels multiples higher than today’s values, and with it, valuations multiples higher as well.

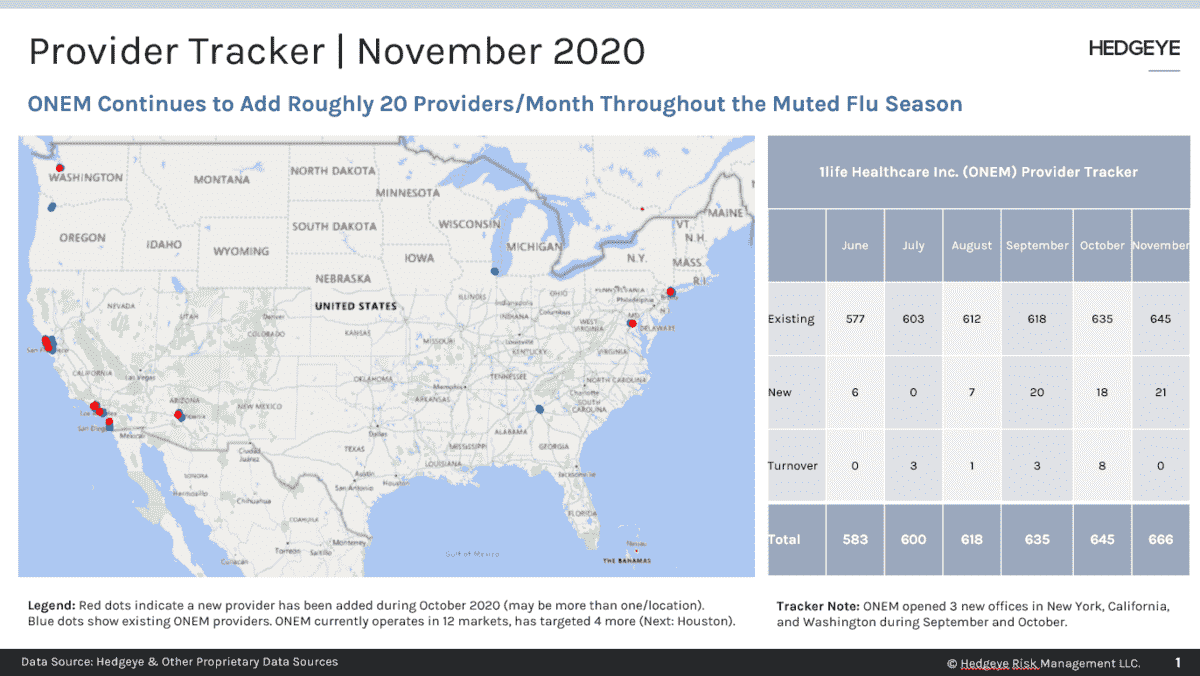

Provider Tracker

Census Data

App Download Data

Key Assumptions

All data available upon request. Please reach out to with any inquiries.

Thomas Tobin

Managing Director

Twitter

LinkedIn