With the collective national attention myopically and understandably fixated on election drama, a somewhat equivocal ISM Services print will not divert attention or refocus any narratives, but it’s worth a quick highlight, particularly as it comes on the heels of a decidedly underwhelming ADP Payroll print for October.

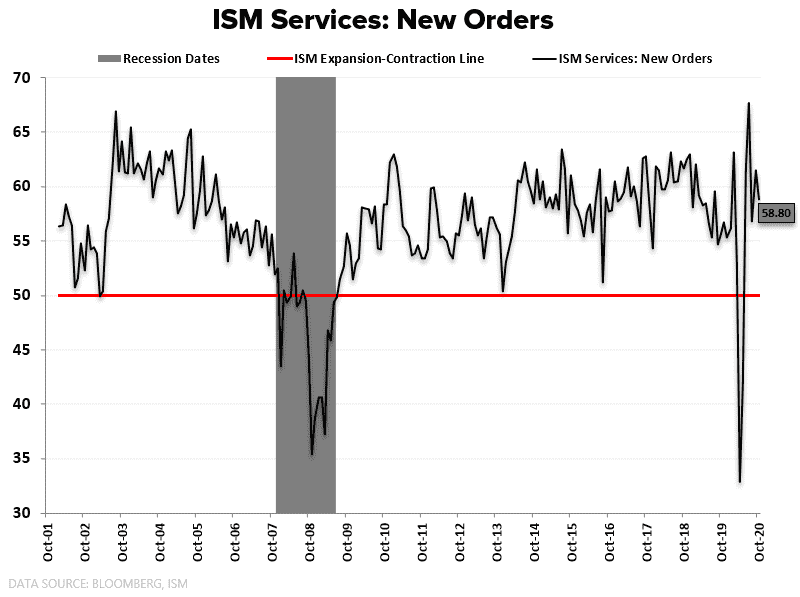

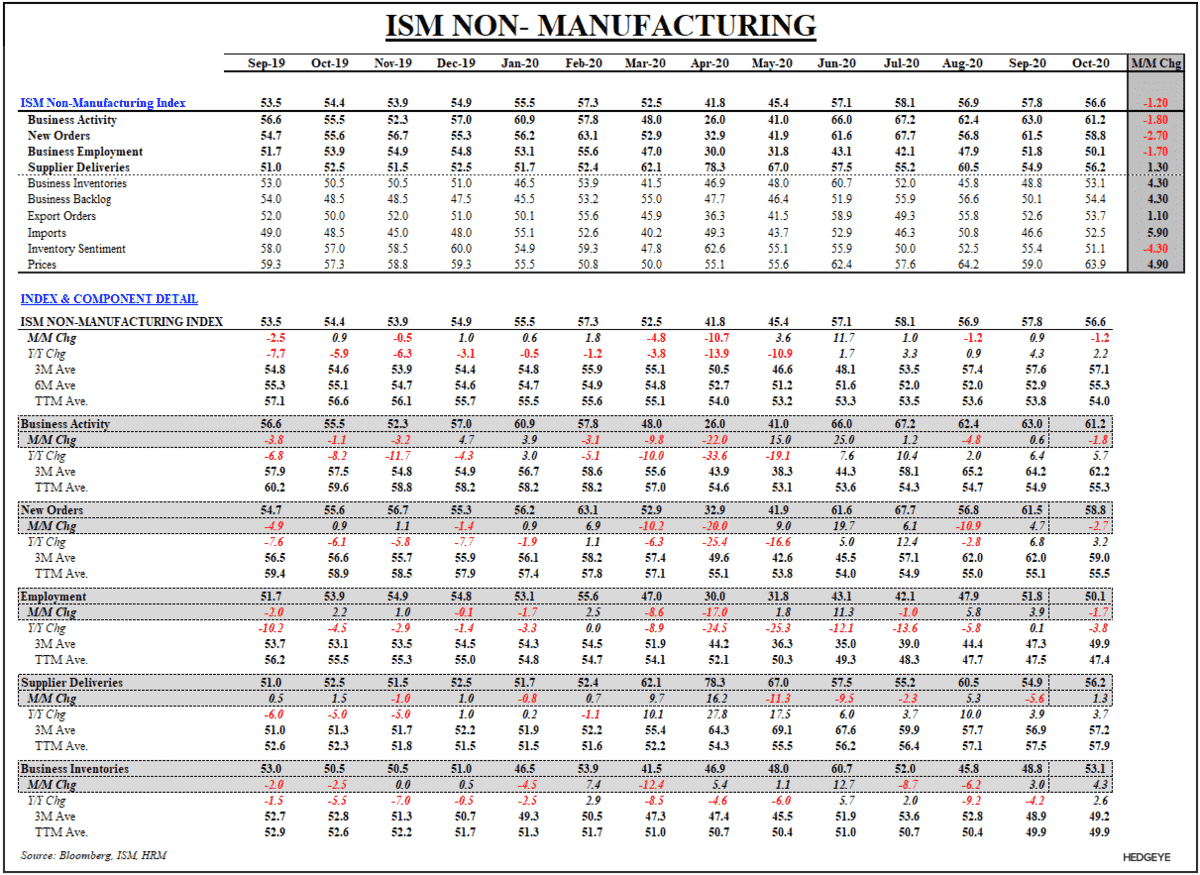

Headline Services ISM dipped -1.2 pts to 56.6 – undershooting estimates and marking the lowest level since May – with each of the primary sub-indices registering sequential declines.

Note that with Prices rising 4.9 pts and holding near 2Y-highs, the data imbue a Quad 3/Stagflationary flavoring to the start of the 4Q high-frequency feed.

The moderation carries the same raft of explanatory context that has accompanied marginal deceleration in domestic activity indicators as we’ve traversed past, and now through, the main thrust of the mechanical rebound + COVID fatigue phase of the recovery.

It remains relatively straightforward …. Industrial/Manufacturing activity (which was a relative beneficiary of WFH/Lockdowns/Reduced Mobility and the associated shift away from Services Consumption and towards Goods Spending) has selectively recovered but stalled below pre-lockdown levels in the aggregate.

Meanwhile, labor market gains have slowed, PPP funding and enhanced jobless benefits have expired, stimulus funds and the associated savings accumulation has begun to be drawn down and permanent job loss continues to rise … all as shelved stimulus and the combination of impending winter and resurgent virus numbers threaten to pull the rug out from under a Services economy still in trudging and fragile recovery.

ADP EMPLOYMENT ...

Meanwhile, on the labor side, ADP payrolls came in at +365K for October, missing consensus estimates for +749K by a mile

Convictedly cross-walking the ADP estimate to NFP expectations has become an increasingly acute exercise in Tasseography but in the simple interest of serving as a distraction from the political theater … consider that if ADP is ballpark correct on the Private Payroll side, the Headline NFP data will be close to flirting with zero as Temporary Census workers fall out of the count (roughly -150K, at least) and drag on the reported October total.

To be clear, both Services Activity and net Employment gains remain in expansion but are flashing a fledgling transition to less good. The prevailing risk is that the confluence of fading momentum and the risk set above fuel a further transition in the direction of deterioration.

Of course, with today’s iteration of thesis drift ('gridlock is good') seeing asset prices spike amidst a fading of the (formerly positive catalyst) pro-cyclical blue wave trade in favor of (the converse but also, apparently, positive) growth and duration exposures – it’s a poignant reminder of the active detethering of the economy and markets, that investors have not voted to repudiate narrative drift and analytical expositions are still back-fitted to explain prices, not the other way around.