Summary:

Global payments is a direct beneficiary of the ongoing, and now accelerated, global secular shift towards electronic payments, in addition to being a well-resourced, well-run player poised to grow market share in a consolidating industry. Moreover, the company has successfully evolved its traditional merchant payment processing business over the years to now include a 60% contribution from high growth, higher margin e-commerce and omnichannel, integrated payments, and vertical market software solutions. In addition, with its newly acquired issuer business set to benefit from increased bank outsourcing, as well as a tripling in its addressable market from a recent partnership with Amazon Web Services offering a cloud-based platform for smaller issuers, we find ourselves able to look past the near-term choppy waters presented by the domestic holdup of additional federal relief funds, the worsening employment situation, and returning global COVID restrictions. Lastly, we take confidence in the 2021 EPS target of ~$8 shared by management on the call, which came in above the pre-3Q earnings consensus figure of ~ $7.60 and is achievable through the realization of cost efficiencies and the company's new share repurchase authorization. GPN remains a Best Idea Long.

The Details:

Global Payments reported 3Q20 diluted non-gaap EPS of $1.71, drawing level with its pre-merger self one-year ago and surpassing the $1.66 average street figure derived from 33 estimates ranging from $1.52 - $1.82. The company's earnings beat was fueled by top-line overperformance and better-than-expected margin expansion.

On a combined basis, total revenues fell -4% y/y, driven by a -6.1% decline in merchant solutions revenues and offset by +7% growth in the company's business & consumer solutions segment as the prepaid card business continues to capture some of the effects of direct-to-household stimulus, the cyclical rise in debit spending, the accelerated secular migration to cashless payments, and easier comps from the lapping of CFPB headwinds.

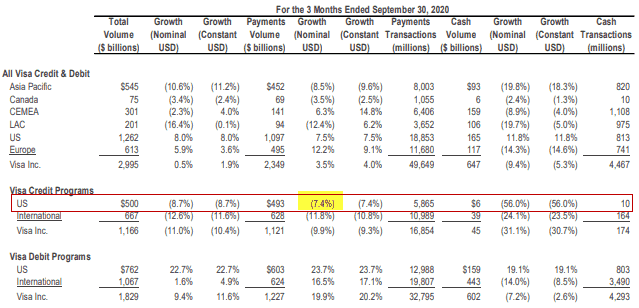

Third quarter merchant revenues, improving +15 points sequentially from down -21% in 2Q20, outperformed the -7.4% y/y decline in U.S. credit volume reported by Visa, which management had previously flagged as a useful tracker for its merchant segment. The positive decoupling points to the success of the company's fast-growing technology-enabled portfolio, composed of three equal channels: omni-channel, partner software, and owned software vertical markets businesses. Global's technology-enabled portfolio now represents 60% of merchant revenues compared to 40% in 2018.

Within the merchant segment, management noted that e-commerce volume, excluding travel, was up mid-teens; meanwhile, integrated solutions (partner software vertical markets business) revenues returned to positive growth in the third quarter.

Elsewhere, the company's issuer solutions segment saw revenues decline -2.4% y/y, a +220 bp sequential improvement as transaction volumes recover and traditional accounts on file continue to grow in the mid-single segments. Excluding its commercial card business, hard hit by limitations to global travel and representing 20% of the issuer portfolio, the company's issuer segment revenues were up in the mid-single digits on a combined basis. On the call, management highlighted 33 wins in the issuer segment over the past 18 months as well as a pipeline of 11 new-client deals, 7 of which are competitive takeaways.

On the cost front, adjusted operating margins, led by a +500 bp improvement in the issuer segment, expanded +240 bps y/y to 41.1% as the company continues to drive efficiencies across its merchant and issuer business segments while also benefiting from the immediate and significant cost actions taken in response to the pandemic.

As a result, the company raised its TSYS merger cost-synergy target by $25 million to $375 million by 2022, while also claiming to be on track to deliver at least $125 million in annual run rate revenue synergies and a further $400 million in additional annual run rate expense savings related to the pandemic..

The company concluded by announcing an increased share repurchase authorization to $1.25 billion and sharing its target for adjusted EPS of $8 in 2021.