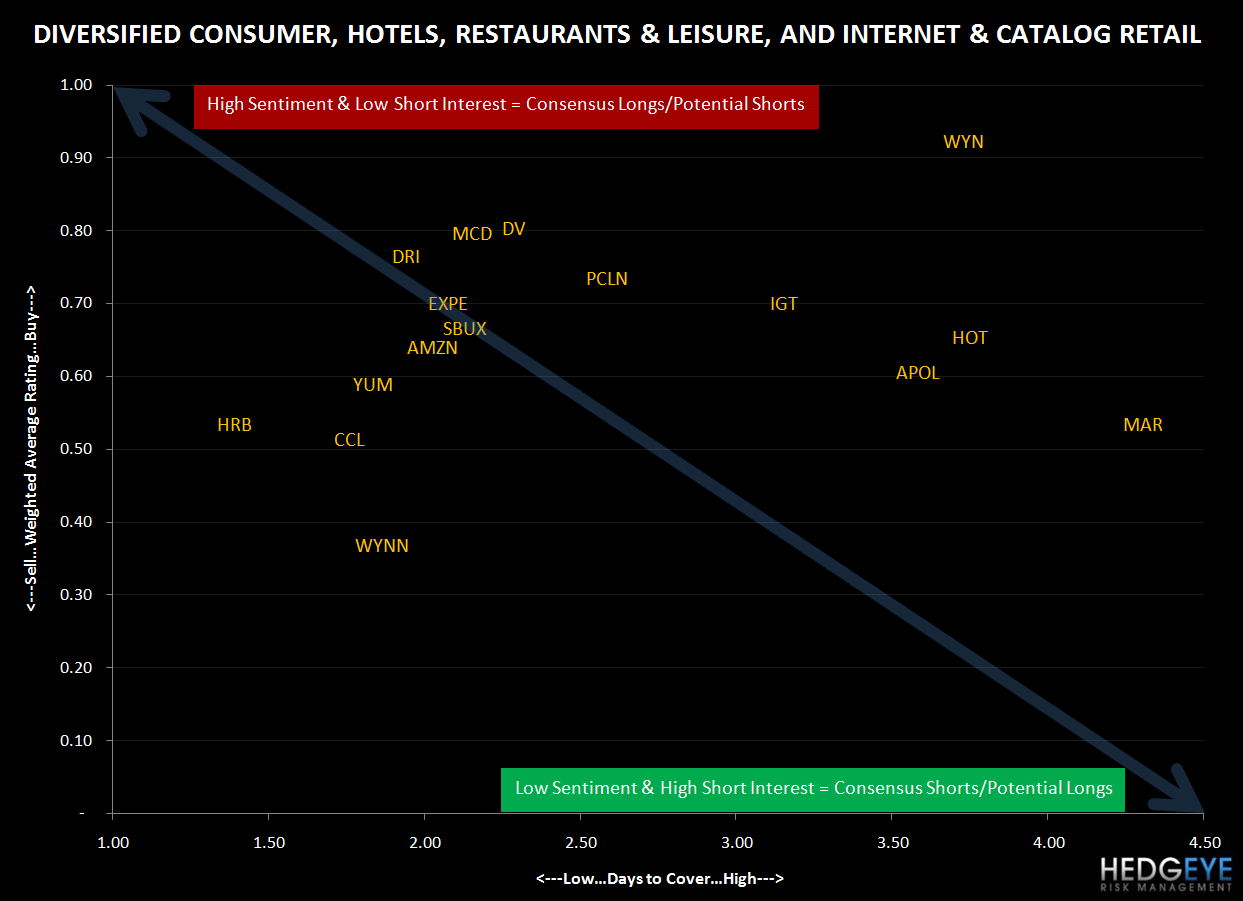

One of the first screens we use to identify potential long or shorts is sell-side sentiment versus short interest, which is expressed via the days to cover ratio.

Looking at the data since I penned my DUPE(d) Early Look on June 29, 2010, it is clear that the trends for the American consumer are not getting any better. We are getting closer to 4Q10, which is the quarter in which significant pressure on the consumer should become more evident. We estimate that consumer discretionary spending could be down as much as 3% in 4Q10.

As of the close yesterday, Consumer Discretionary was the second best performing sector year-to-date and one of only three sectors that is up year-to-date (XLY up 4.9%). The other two sectors are Industrials (XLI up 7.4%) and Consumer Staples (XLF up 2.1%). While easy comparisons and “corporate” fiscal austerity have helped the performance of consumer stocks, the best days of this cycle are behind us.

Today, the XLY is the best performing index, up 1.4% at the time of writing. The positive consumer sentiment is being driven by the increase in mortgage applications, following a surge in refinancing. In theory this should help consumer spending. Also, restaurant sales trends are looking better with the Knapp-Track showing an increase of +0.9% (Traffic of -1.7%) vs. -8.3% last year; this is the first increase in 26 months. Of the ten best performing names in the XLY today 6 are retailers. Expedia is the worst performing stock in the XLY sector.

As a reminder, the DUPE(d) thesis looks like this…

Double-Dip: The housing market and the broader economy are on the precipice of a double dip; housing prices have already started to decline and the economy has slowed significantly quarter-to-quarter in 2Q10.

Unemployment: Weekly Jobless Claims have not shown any material improvement over the past six months.

Prices Paid by the Consumer: While reported inflation by the government looks to be under control, the Hedgeye Inflation Index tells a different story. The Hedgeye Inflation Index focuses on the part of the economy showing inflation that impacts the consumer, specifically the spread between the prices of things they buy and what they earn.

Equity and Real Estate deflation: We believe that the debasing of any currency (even the Almighty Dollar) ends badly. A lack of austerity in government policies and our politicians’ aversion to facing facts are not helping the long-term outlook for equities.

Looking at the Hedgeye Sector Sentiment Monitor, the street has become more optimistic about the XLY relative to six months ago; sentiment on the XLY stands at 60.01 vs. 56.53 six months ago and 58.9 for the S&P 500.

Within the Consumer Discretionary index, the three most loved sectors are Diversified Consumer, Hotels Restaurant & Leisure and Internet & Catalog Retail. Narrowing it down further within those sectors, the most loves names are Darden (DRI), McDonald’s (MCD), Starbucks (SBUX), Expedia (EXPE), Amazon (AMZN) and Devry (DV). Collectively, these stocks have a 16.2% weighting in the index, with MCD representing 7.8%.

Howard Penney

Managing Director