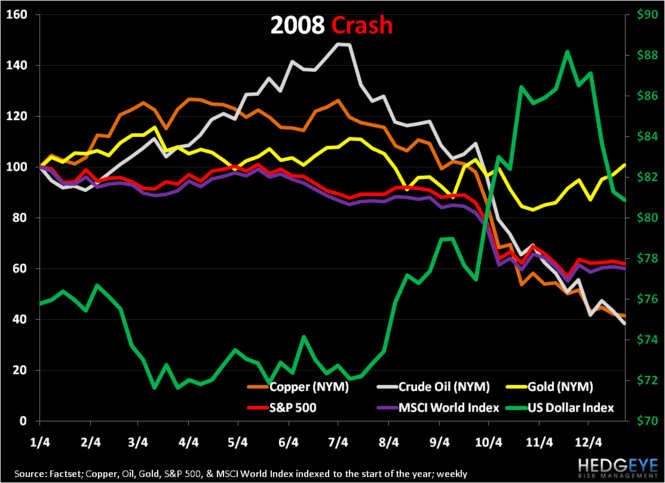

These charts were extracted from a larger MACRO SELECT post (available to RISK MANAGER SUBSCRIBERS), dubbed "CHINESE DEMAND CONTINUES TO SLOW . . . COULD THE CORRECTION TURN INTO A CRASH?" from August 11, 2010.

These charts were extracted from a larger MACRO SELECT post (available to RISK MANAGER SUBSCRIBERS), dubbed "CHINESE DEMAND CONTINUES TO SLOW . . . COULD THE CORRECTION TURN INTO A CRASH?" from August 11, 2010.

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.