I know, we all have bigger fish to fry than to keep tabs on labor unrest in Bangladesh. But it is getting to a point where it could further crimp apparel margins in the supply chain’s of US retailers and brands.

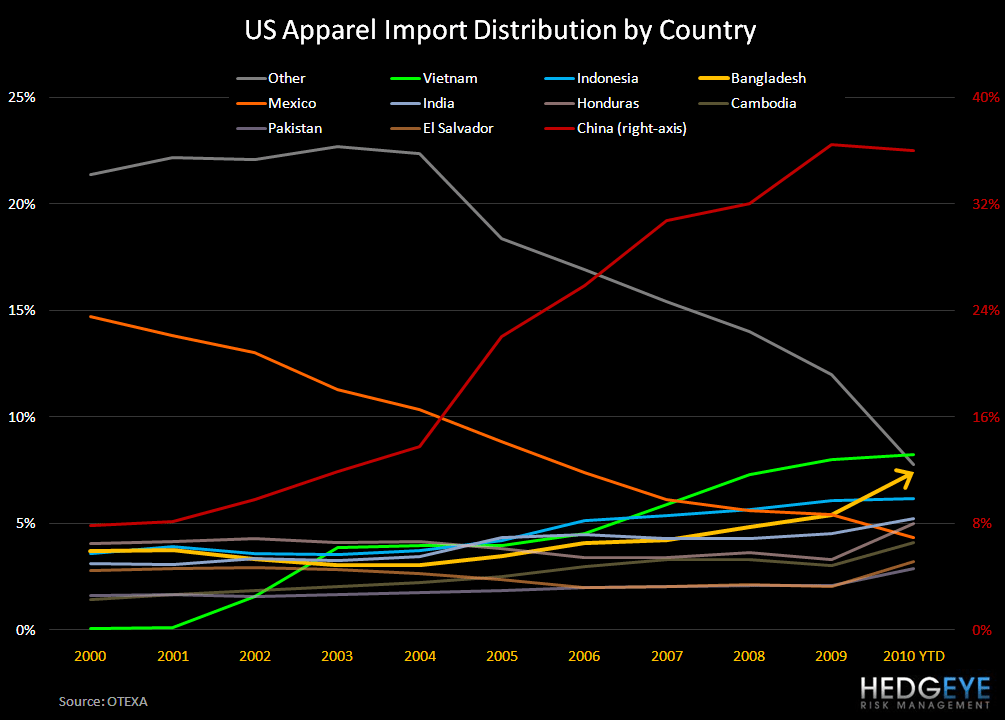

Though not a whole lot of people care, Bangladesh carries the distinction as being the fourth largest source of finished apparel goods for US retailers – garnering about 7% of the market. Furthermore, so far in 2010, Bangladesh has had the sharpest upward trajectory of any sourcing nation – arguably taking share from China, the 800lb gorilla (35% share).

But in response to rampant local cost inflation (nevermind $0.80/lb.+ cotton) workers in Bangladesh went on strike on June 23rd, demanding $75/month versus the prior rate of $23. The government’s National Wage Board stepped in and mandated $43 (a 72% increase), but that’s not been enough for the entire workforce to resume production.

Let’s assume that only a quarter of this capacity is still on hold. That still suggests that 1.5-2% of the global capacity for apparel is taken out temporarily (until the cost structure is fixed).

One could argue that China could step in and regain share. Perhaps they will. But let’s face facts…China outwardly stated that it wants to shift focus away from exports and towards more local consumption. The only way it will pick up slack capacity is if it will be at a meaningful price hike.

It’s all the same thing to us. It spells apparel inflation. The assumptions we need to make on the demand side of the ledger are tough enough. But on the cost side too?

And the Street STILL has the industry blowing through peak margins next year.

C’mon…It’s time for a reality check.