Overview

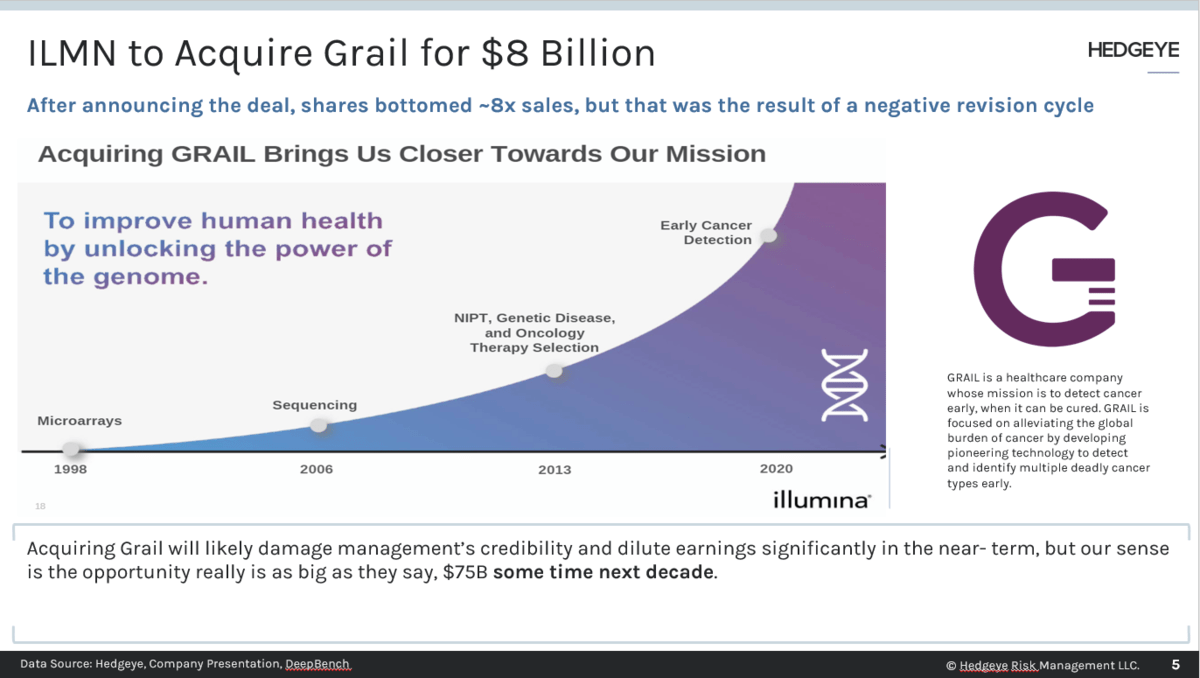

We spoke with a former senior executive at a molecular diagnostics company (>6 months removed) and came away thinking, “Wow, for $8B, Illumina (ILMN) better know something about that Grail data well beyond what they are saying.” It’s not hard to imagine that they do know [much] more than they are letting on, but we can’t ignore the underwhelming reaction to the data far from the experienced professionals we’ve spoken with. Our contact reinforced the notion that “it’ll be really hard” for ILMN/Grail to prove utility based on the published sensitivity and specificity data.

Takeaways

- Early detection is the biggest market but will be the most difficult to penetrate. Key questions include: What will clinical pathways look like? How will payers respond? As of now, none of the sensitivity data are good enough.

- Guardant’s (GH) management team has done a good job to date (developing tech and their approach to the market). They are focused.

- Signatera makes sense – the data are great (early detection of MRD works); however, the big question is whether positive, early results will lead to better outcomes/OS.

- Again, we heard about the importance of utility for doctors and payers. The doctors need data and guidance on what to do with positive test results, and payers want to see data that helps support the cost/benefit of liquid biopsy tests.

Field Notes

What's the groundwork/framework for Liquid Biopsy as you see it?

- There are three main applications, and evidence for analytical validity, clinical validity, and clinical utility is needed for each.

- Early detection. Grail, Exact (more recently), Thrive, and Guardant are among the leaders here. It’s the biggest potential market, but also the most difficult.

- Treatment selection (relatively straightforward) – what targeted drug is needed?

- Monitoring for residual disease/recurrence. While this could be two different categories, they are sort of the same thing (different time frames).

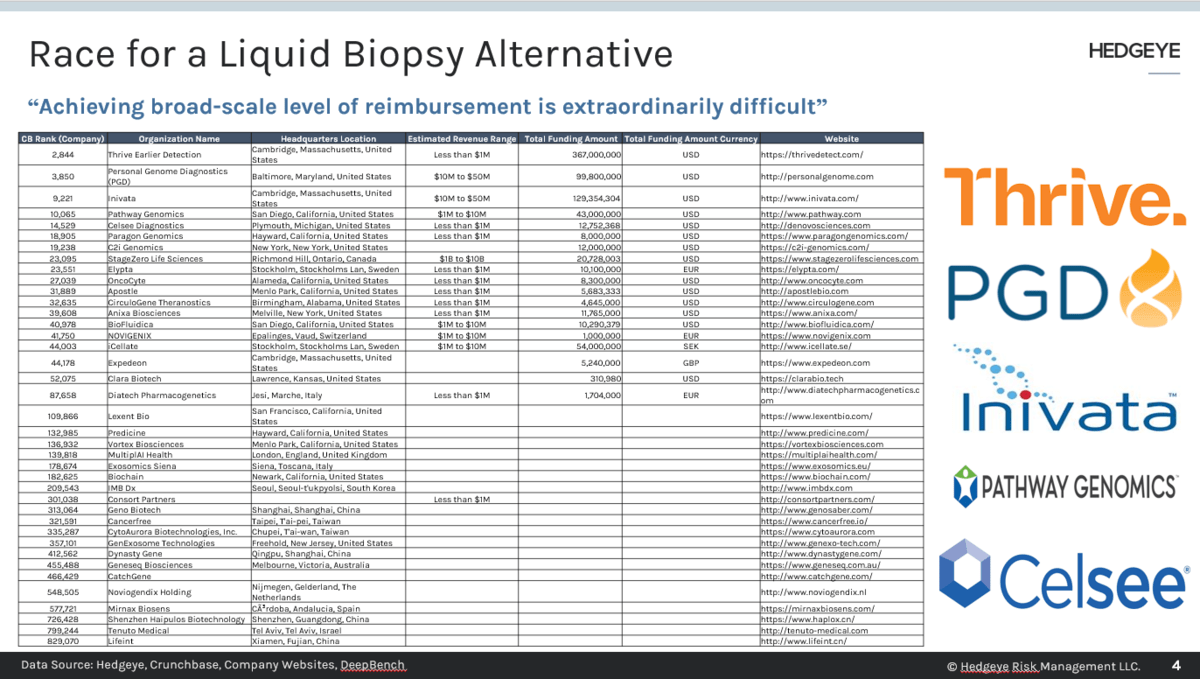

- Differentiating between those 3 is important because of payer response. Dx companies must get private payers on board. It’s usually tough going until a company gets into the sweet spot (>70% reimbursement), and then you can just “print money” (hire more salespeople, compound it). Getting to that broad-scale level of reimbursement is extraordinarily difficult.

How should we think about Grail given that context?

- I think the $8B number works if we’re talking about the entire field of early cancer detection. The real question is: “What’s the path to get there?” Based on the data thus far the path isn’t clear. The four key data points: sensitivity, specificity, negative and positive predictive values.

- Grail “took heat” for high specificities without deference to positive predictive values. In a screening situation, it’s not clear that the validity or utility hurdles have been met.

“It looks like the test has a long way to go.”

- Detecting cancer in stages 0-1 is where the most good can be done; however, this is extraordinarily difficult b/c there are so few molecules in circulation. Detection rates go up significantly in stages 3 and 4. At that point, what’s the use? There’s no utility because the patient is already in the doctor’s office for imaging or pain.

- I don’t think ~50% sensitivity is helpful, especially from a payer’s perspective. AACR data - letters to the editor – showed a + predictive value of ~49%, which means you’d miss a lot of the cancers due to low sensitivity. And, when there is a rare + test, there’s a 50% chance that it’s false (i.e., a doctor would send a patient for additional screening/work and only find something ~50% of the time).

Is this like 3D mammography where you’re putting women through testing, then biopsies, adjuvant therapy, etc. and there’s no survival benefit? It’s so early – maybe the body could be resolving the cancer?

- Early detection is tricky. The problem with it = we may not ever see a survival benefit. Regarding the second part – I’m not sure. It’s possible that the body could resolve it. The bigger issue is where you can find the early stages of cancer.

- The best applications might be pancreatic, ovarian, and lung because there’s no routine screening, which means the cancer is unlikely to be caught before stage 3. If you’re trying to show utility, and have decent sensitivity at stage 1 or 2, there’s a chance. Grail has published some data by stage, but it’s not big enough by the tissue of origin and stage.

How does methylation fit into the tissue of origin question? Guardant bought Bellwether, so we presume it’s important…

- It is, look at Exact. Epigenetic change – that impacts the ability of the gene to produce a protein, once methylated, you can read the gene, etc. By looking at certain genes, which methylated, you can reverse engineer for the tissue of origin.

- Guardant has more interesting data than others. Exact’s data showed a big jump (in sensitivity – 83%), but it’s small and circumspect, enriched by having the 6 cancer types. That figure will come down. It looks like the distribution is skewed toward later stages (3 and 4), but they didn’t break it down.

Think it’s possible to find polyp detection or early colon cancer in blood?

- It’s going to be hard because there isn’t much in circulation w/ a polyp. Maybe some adenomas, but there isn’t much circulation in that part of the body (it’s just the way the blood flows to the colon). That will make sensitivity difficult. The clinician still wants the patient to get a colonoscopy, but if the pt doesn’t want to, Cologuard helps check a box.

- The issue is that doctors want to use something w/ high sensitivity. They don’t want to tell a patient there’s no cancer, then have something materialize. The downstream MUST be innocuous and effective. Colon cancer is perfect because a patient can go get a colonoscopy (in the grand scheme, it’s a “palatable” procedure).

- Pancreatic cancer is another good one to think about. The shift to imaging is not 100% but is doable for pancreatic (and ovarian) cancer.

- Guardant360 has been successful w/ lung cancer, because you can’t get a biopsy or many of the patients (can’t get to the tumor to know).

Note: Another issue is small patient populations. The high risk BRCA group is not a massive number. If the COGS is ~$100 (EXAS has ~80% gross margins on a $500 test), then maybe there’s a market for Galleri for routine screening. That said, if it launches in ’21 and FDA approval follows in 2023-24, it’s hard to see big utilization – it’s just not clear how to use the test, yet.

- Another worry is MDs making money doing different procedures (if the procedures are in-line before the test). Who are the decision makers? If the patient is the decision-maker, and it’s a woman at a well-visit, I think she’d pay cash for an blood test to screen for ovarian cancer.

How would you show utility?

- I’m not sure – looking at the criteria listed above, you can see why you wouldn’t want to start with a pan cancer test. I’m not sure how you show utility, but Grail spent $1.9B thus far and there must be some data that nobody has seen, and who knows what it says. Who where the people at ILMN evaluating the Grail deal? ILMN is a great company but understanding of commercialization in the Dx space and reimbursement is not their strength.

Guardant, Guardant360 & Insurance Coverage

- Guardant has done a good job developing tech and I like how they approached the market. Management seems focused. Everything has been done very well to date.

- It looks like Guardant is still 40-50% lung based on the data – MDs aren’t adopting it for solid tumors, yet (despite a broad coverage determination – 12 tumor types). Some of that is physicians’’ behavior, some of it is who the salesforce is calling on (most specialize in lung – not sure if the team is being retargeted or its size increased).

- As an aside, it’s interesting to note that Medicare is ahead of all payers by 4-5 years on covering treatment selection (nowhere else in healthcare is this true).

- Medicare covers a high % of pts with these cancers we’re talking about. If you get me to critical mass – that 70%+ coverage level by having Medicare plus a couple of other payers, I can get a long way down that TAM. Prostate cancer and colon cancer have a high % of Medicare. Analysts should think about that when modeling this… private pay in lung doesn’t matter.

- Medicare can’t cover screening unless it’s USPSTF – it’d take an act of Congress. The way the law is written, screening is only for people that have disease. Exact got lucky with its FDA approval two weeks before the ACA and USPSTF was updated.

ArcherDx - Invitae

- On the concept of detection, monitoring, I’m not sure that it does get at that. It’s more of a kit-based approach, but the tech doesn’t lend itself to a kit, in my opinion. More validation work for payers is needed.

Signatera – Natera

- The science is sound – I think what Natera is doing makes sense. The utility question is an issue. A prospective study showing that early detection of recurrence leads to better survival, which is not trivial to execute, would help.

- MRD detection works. The Kaplan-Meier curves look fantastic, but the real question is “What do you do if you know?” If early detection of MRD doesn’t lead to increased survival, why? What if there are no other effective drugs/treatment options? Then, the doctor can’t do anything and the patient knows.

Do you worry about where the regulatory framework is going?

- Things have taken a dramatic turn over the past two months or so. HHS put out its statement that said the FDA cannot/does not have authority to regulate LDTs… this was/is a huge change.

- Since the mid-90s, they’ve had authority but haven’t used it, and there’s good legal arguments for why the position was never challenged in court – the FDA always backed down. If they lost, they’d have no ability to regulate.

- This all comes down to politics – HHS and FDA are not seeing eye-to-eye. With the new memo out there, CLIA is “in charge” in a parallel regulatory structure (unless legislation passed, which exists). If Biden wins, there’s a chance legislation moves forward that gives the FDA more power. He might not get 60 votes, but he could exceed 50. Absent that, the FDA is dead in the water. They even announced that they are no longer doing EUAs for COVID tests.

- All that said, seeking FDA approval for a test is a “great path” for reimbursement. While private payers don’t always follow suit, the FDA doesn’t look at utility, and getting Medicare coverage goes a long way.

Please reach out to with any feedback or inquiries, questions for future field work, or requests for underlying data.

Thomas Tobin

Managing Director

Twitter

LinkedIn