Another serving of underwhelming, garnished with stagnation and drizzled with emergent structural damage as the pandemic payroll apocalypse now spans 8 months.

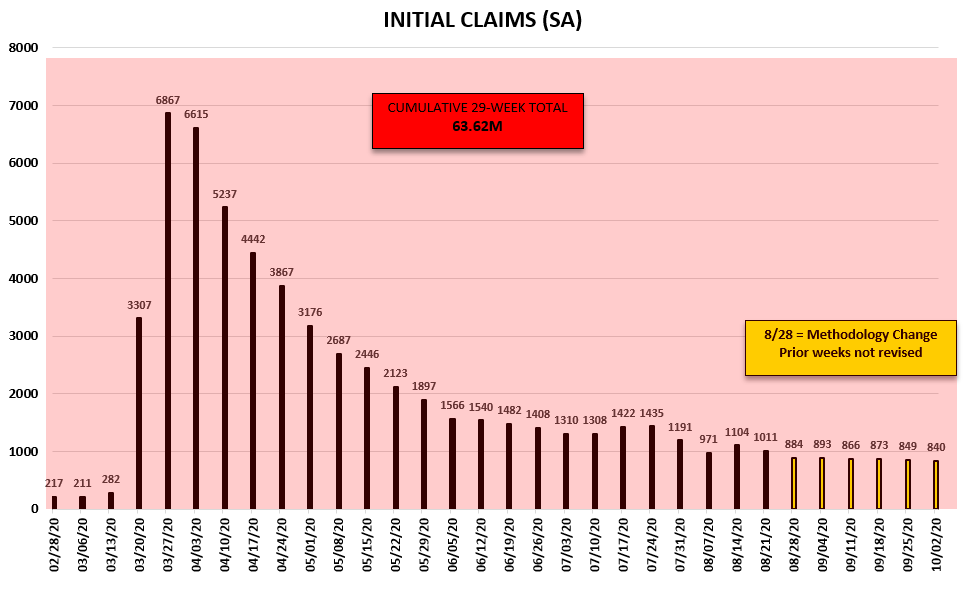

Initial Claims rose W/W (both SA and NSA) while Continuing Claims (lagged 1 wk) and Total Claimants (lagged 2 weeks) both fell by 1M. CA still sits as a (downward) distortion with Claims applications and processing still on pause (which matters given its size & relative contribution)

PEUC Claims (Pandemic Emergency Unemployment Claims), meanwhile, rose by +154K W/W and +328K in the last two weeks. Recall, PEUC Claims should be the metric to monitor as the flow out of regular state claims into the 13 weeks of extended benefits offered under PEUC will show up here … assuming individuals are aware of the benefits and that states can fully and smoothly transition people over, which remains a dubious assumption.

Further recall that regular state benefits typically last 26 weeks and we are now thru week 29 of the Claims cataclysm. With the PEUC data lagging by two weeks, it reflects flow dynamics for week 27.

In any case, attempting to triangulate, with precision, the extent to which Initial Claims are falling due to ‘organic’ improvement or because we are simply running out of large numbers of people to fire and/or because states have moved towards catching up with processing backlogs (which results in multiple counts) is difficult to divine.

Convictedly distilling the extent to which Continuing Claims are dropping because Individuals are being recalled/hired or because they have exhausted benefits and may/may not have transitioned to PEUC or extended State benefits is similarly difficult.

Ultimately, attempting to precision parse the weekly data probably represents superfluous analytical activity.

At this point, some bigger-picture framing probably captures most of what matters:

- We are now 29 weeks into the Payroll plunge, the median duration of unemployment was 18-weeks as of a month ago (reflected in Sept NFP report) while the number the number of people unemployed for 27+ week rose by +781K.

- The benefit eligibility roll-off has already begun and will progressively build. Enhanced UI benefits ($600/wk) ended at the end of July and extended benefits ($300/wk) sourced from redirected FEMA funds are also now largely exhausted.

- Payroll gains continue to slow, PP funds are exhausted, 2nd wave layoffs in both direct and adjacent industries continue to manifest, Permanent Job Loss continues to stop function higher and Household Consumption Capacity fell meaningfully in August as gains in wage income failed to offset the expiration in enhanced jobless benefits (Wage Income + Unemployment benefits = -6.5% M/M in Aug).

- The deterioration to zero or negative sequential growth in Retail Sales, Industrial Production, Durable goods and Revolving Credit all reflect this same reality.

In short, the sloth speed emergence of the collective income cliff that everyone knew was coming has begun to manifest more discretely. In its wake is the shifting risk for a more acute stall in the labor/consumption recovery absent further stimulus.

Frankly, you, the Fed, Congress and any casual observer has been fully aware of the probable procession of income dynamics and the attendant risks for months.

So as structural damage becomes more entrenched and the psycho-emotional toll cumulates and income security deteriorates for millions, it should come as little surprise that in queue we have …. $25B … for airlines … maybe.