“And remember, no matter where you go, there you are.”

-Confucius

I’ve learned, un-learned, a re-learned this lesson in trading markets many times in the last decade - Don’t Do Dogma. The larger your risk management and research team becomes, the harder it gets to adhere to that discipline. The more research edge you have, the more confident you tend to become. This breeds confirmation bias and risk.

A disciplined risk management approach to allocating capital is a process best learned by doing. I don’t learn much when my team is right on the research - I work with winners who wakeup expecting to be right. I learn the most when our positioning to express that research is wrong.

This gets to the heart of a structural problem with our industry. There is a huge difference between being right on the research and right on your timing, sizing, and positioning. Our industry pays a “star” premium for conviction in best research “ideas”, but pays much less for the risk managed expression of those ideas. This is good. It provides a tremendous opportunity for us to evolve our profession.

“No matter where you go” this morning, “there you are.” I have my coffee and my notebook, and markets are trading for and against my positioning. Without a repeatable risk management plan, I’m not sure what you do when you login every morning. Different strokes for different folks, I guess, but when it comes to grinding through the morning’s macro data, my research process has a very low standard deviation.

Conversely, as you may have noticed, my decision making process has a very high standard deviation. Sometimes I make too many Hedgeye Virtual Portfolio and Asset Allocation moves, sometimes I make too few. I learned this playing hockey more than anything else, but there is a time to be moving your feet, and there is a time to wait in the weeds – goals get scored when your timing is right.

Yesterday the US stock market was down, so I took that as an opportunity to cover some shorts and buy some longs. Because our macro research is bearish on both the US Dollar and the SP500 doesn’t mean I have to be bearish at every time and price on everything USA (we’re long XLU, Utilities).

In modern day risk management, it’s critical to contextualize both time and price within the framework of different investment durations. That’s why we have developed the TRADE, TREND, and TAIL process. It helps us communicate our research findings in a way that isn’t Duration Dogmatic.

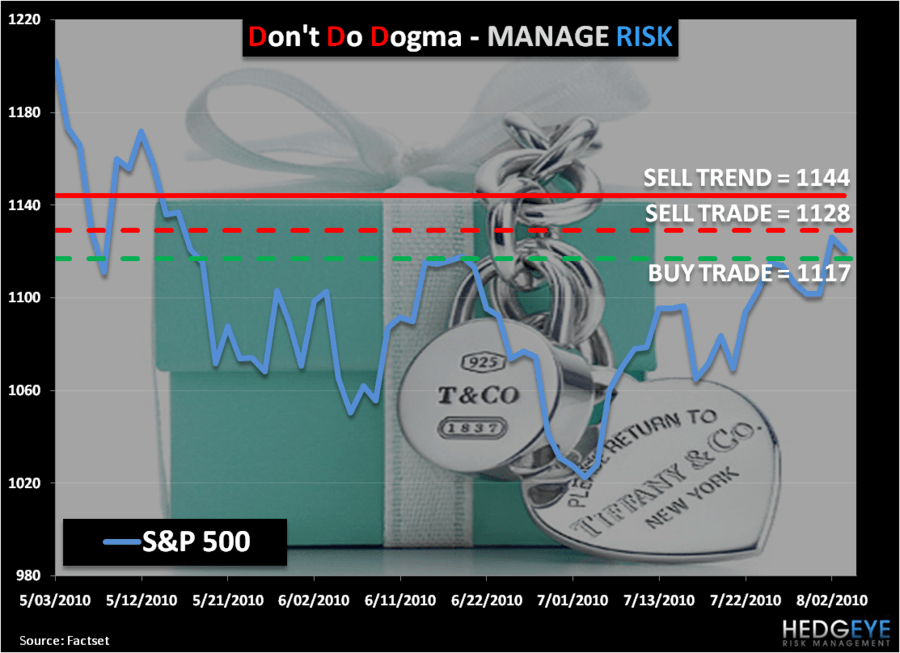

The SP500 has only had 1 up day in the last 6 trading days. That 1 up day was of consequence however, because it took out the immediate term TRADE line of resistance of 1117. Whenever resistance becomes support on any of our 3 core investment durations (TRADE, TREND, and TAIL), I start moving my feet.

The setup for this morning is the same as it was as I was changing my positioning into yesterday’s close. Inactive investors dogmatically call this “trading” – I call it proactively managing risk. You trade today in order to set yourself up for tomorrow.

We went through this on our Macro Monthly Strategy conference call yesterday (if you’d like the slides and replay, please email ), but it’s worth repeating – the Bear Market Macro lines for the US Dollar Index and SP500 are $84.32 and 1144, respectively. These are my intermediate term TREND lines of resistance. These back-test with the highest success rate of any duration in my model.

Bearish TREND doesn’t always mean bearish TRADE. To the contrary, bearish TREND often insulates bullish trading inasmuch as bullish TREND formations can perpetuate bearish immediate term trading. Bull and bear markets get both overbought and oversold.

If the US stock market gets banged up today, there are no rules saying that this bullish immediate term TRADE support line of 1117 in the SP500 can’t become resistance again - and quickly, with no downside support to 1089. Don’t get frustrated with how short term that sounds. Embrace it. Managing risk doesn’t occur in a baby blue Tiffany box.

The conclusion of all this is always on the tape. Yesterday I invested 6% of the Cash position in our Asset Allocation model, taking Cash down from 79% to 73% by adding a long position in International Equities - Indonesia (IDX) – and adding another 3% to our long position in the Chinese Yuan (CYB).

The risk in all of this is that 1117 doesn’t hold, because that means anything I covered or bought yesterday will have likely been executed on too early. In real life investing, being too early means being wrong. Don’t Do Dogma – that’s for marketing presentations about investing.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer