“You can get further with a kind word and a gun than you can with just a kind word."

Capone - The Untouchables

Yesterday’s intraday rally in the US stock market was decorated with rumors of Spanish politicians prancing around talking about successful “stress tests” and Ben Bernanke pulling out the “quantitative easing” gun. Thank God for the modern day Triumvirate of Fiat Fools (BOJ, ECB, and the Fed). Without professional politicians deciding our fate, what hope would we western capitalists turned socialist turtles have left?

Hope, of course, is not an investment process; neither is hanging your hat on economies that allegedly only work with financial aid’s heavy hand of Big Keynesian intervention. Fear is the cement that provides the Fiat Triumvirate its political platform - and their podium is shaking.

I couldn’t make this up if I tried, but one of the top headlines from Bloomberg this morning takes the fear mongering by Fiat Fools running global monetary policy to new heights:

“Bank of Italy Says Financial Crisis Fosters Mafia”

As Western governments continue down the political path of scaring the hell out of you, be afraid fellow citizens, be very afraid – the Fiat Guns of quantitative easing and piling Debt Upon Debt Upon Debt will continue to kill both your domestic currencies and employment prospects.

This Italian headline, by the way, didn’t come from Rome’s version of Drudge. The manic media’s guns came out after the Italian Central Bank’s Deputy General Director, Anna Maria Tarantola, made explicit fear mongering statements that would make Julius Caesar’s messengers proud:

“The crisis has given organized crime room to thrive because access to credit has become more difficult… Whoever holds large amounts of cash, like crime groups, can make investments that aren’t possible for others. They can now invest in fully legal businesses.”

Wow. I guess cash really is king. Maybe we should start to take the government’s word for it and up our asset allocation to cash before Michael Corleone sends Timmy after us…

The catalysts for Spaniard and US Federal Reserve rumors were centered around 2 very clear and present dangers:

- Ben Bernanke’s semi-annual Revisionist Forecasting Report to the Senate of Modern Day Rome (today).

- Results for the made-up European “stress tests” that already have a prescribed (positive) outcome.

If there is one thing that the Fiat Fools have taught modern day risk managers who trade markets, it would be not fighting the Fiat Gun of intervention that they hold so dearly in their heavy government hands.

That’s why 32% of companies in the so called “great earnings” season of the US can miss the revenue line for the Q2 reporting period to-date, and you can see a monster intraday reversal of earnings oriented stock market weakness turn into a melt-up of short covering. As Max (James Woods) said in “Once Upon A Time In America”: “This country’s still growing up. Certain diseases, you’re better off having when you are still young.”

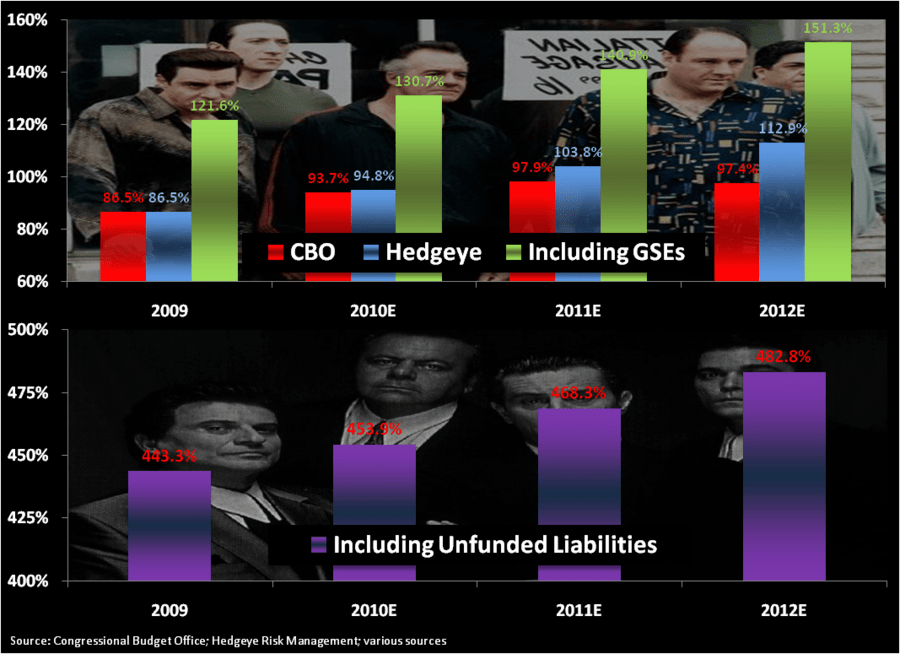

We have no idea what Ben Bernanke is going to say about quantitative easing programs today, but we do understand the basic algebra associated with adding more US debt to the US DEBT/GDP ratio (email if you want to see how we get to triple digit percentage US DEBT/GDP ratios for 2011; slide 11 of our Q3 Macro Themes presentation is in our Hedgeye Picture of The Day).

If he pulls out the Fiat Gun, at least we’ll continue to get paid on the short side of our US Dollar (UUP) position!

Back to the non-rumor mill oriented macroeconomic facts, Japan’s quarterly loan index plummeted in July to minus -17 (lowest since 2004) from minus -10 in the prior period. Japanese stocks closed down for the 6th day out of the last 7, taking the Nikkei to -12% for the YTD.

All the while, the great Japanese “quantitative easing” experiment that has spanned 2 decades reminds me that living in fear on the short side of a conflicted and compromised government balance sheet is no risk management life to live.

As Carlito said in Carlito’s Way, "there is a line you cross, you don't never come back from. Point of no return. Dave crossed it. I'm here with him. That's means I am going along for the ride. The whole ride. All the way to the end of the line, wherever that is."

My immediate term support and resistance lines for the SP500 are now 1059 and 1103, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer