This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

The summer of 2020 is all about picking winners and losers in the COVID-19 lottery. This is especially of concern since government agencies such as the Federal Open Market Committee and US Treasury get to do the picking, a classic example of crony capitalism in practice.

Counting and sizing the winners and losers will inform the macro perspective in the weeks and months ahead. The Treasury just released a list of the largest participants in the PPP program, but the market is no longer the biggest factor in selecting winners and losers.

We can recall a decade ago going to see one of the bigger lawyers in the New York commercial real estate community. A young graduate who had worked for a small developer fixing and flipping homes in the Hamptons wanted to get into big time commercial real estate development. He sought guidance.

The lawyer viewed his resume and advised the young man to stop seeking a position in development, but rather look for work in restructuring. "We're not doing development any more kid," he advised. "It's about restructuring now." Then as now.

Many observers are predicting a November victory for Presidential candidate Joe Biden (D-DE), a phenomenon strangely similar to the predictions made about Hillary Clinton four years ago. Recall that both democrat candidates were largely invisible, then and now.

Meanwhile, the frequently overexposed President Donald Trump is doing the sort of things that incumbent presidents do to win re-election, namely being nice to Teamsters. “The US Treasury department has reached a deal to bail out YRC, a struggling US trucking company, with a $700m loan using funds from the $2.2tn stimulus legislation passed in March,” reports The Financial Times.

The loan gives the Treasury a 29% equity stake in YRC, which Treasury Secretary Stephen Mnuchin describes as a key Pentagon vendor. Now YRC is a key vendor for just about everybody, right? And did we mention the loan saves 30,000 jobs including the jobs of 24,000 Teamsters?

Moving from the sublime to the tragic, appraiser Miller Samuel says that purchases of co-ops and condos in Manhattan tumbled 54% from a year earlier to 1,357. In a report published last week with brokerage Douglas Elliman Real Estate, Miller Samuel says this was the biggest annual decline since the two firms started keeping the data three decades ago.

While the world of high-end Manhattan residential real estate is certainly not looking very promising, the outlook for employment continues to be a big bone of contention. Recent strong gains in jobs have caused some analysts to claim that the headline unemployment rate is at best distorted to show an overly optimistic picture of the labor market, and at worst a downright lie perpetrated by President Trump to manipulate public perceptions.

Bryce Gil of First Trust Advisors retorts: “It’s crucial to point out that even though the level of the unemployment rate would have been higher in June, its decline would have been larger. The official rate fell 2.2% in June, from 13.3% to 11.1%. With reclassification, the decline would have been nearly twice as large, falling 4.2% in June, from 16.3% to 12.1%. Given that it's the change in the unemployment rate that matters for financial markets when gauging the strength of the economic recovery, reclassification reinforces the optimistic outlook.”

Good news on employment would be really great right about now, but we continue to worry about anecdotal reports that suggest a second wave of job losses impends in 2H 2020 and that this wave could be a significant obstacle to economic recovery.

Those parts of the economy that are reopening are not nearly sufficient to provide jobs and livelihood to millions of people who worked in the services sector. And many employers who did protect workers for the past few months are running out of cash. We won't mention the names out of compassion for the losers.

Another positive is that corporate bond issuance is likely to hit records in Q2 2020, however, the leverage loan market is headed in the opposite direction. Issuance across the U.S. syndicated loan market plummeted in the second quarter, Thompson Reuters reports, this “as the asset class navigated a slow recovery from the novel coronavirus that left borrowers scrambling for cash to keep their businesses alive while economies around the world gradually reopen.”

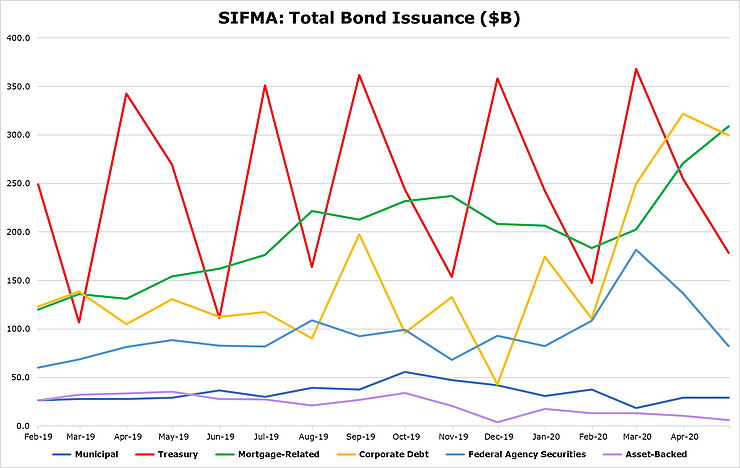

The chart below shows SIFMA issuance data through May, seemingly affirming the concerns we’ve discussed in past weeks with Ralph Delguidice and others about the damage done to asset-backed securities (ABS) markets.

While straight corporate bond issuance is up and mortgage related offerings are also surging to over $300 billion per month, ABS and other issuance is down.

The purple series showing ABS issuance is essentially a zero. Anecdotal reports suggest that corporate bond issuance in June was above May levels. Residential mortgage issuance also hit new volume records, suggesting a record $3 trillion annual run rate for new residential mortgage production in 2020.

Of note, the residential mortgage sector will be a big bright spot in Q2 earnings for some banks and financials, but players such as JPMorgan Chase (JPM) may benefit less because the larger banks have stepped back from retail home lending. The latest changes made by Ginnie Mae with respect to loan eligibility (“The problem with Ginnie Mae's new restrictions”) may further hurt the appetite of larger banks to finance distressed government-insured loans.

Follow-on equity offerings and even convertibles were strong in June, again suggesting that the flow of secondary equity and debt offerings from banks and corporate issuers will continue. A proliferation of IPOs and even special purpose acquisition corps (SPACs) suggests a “V” shaped equity market is forming, but will the economy follow suit? We are a seller.

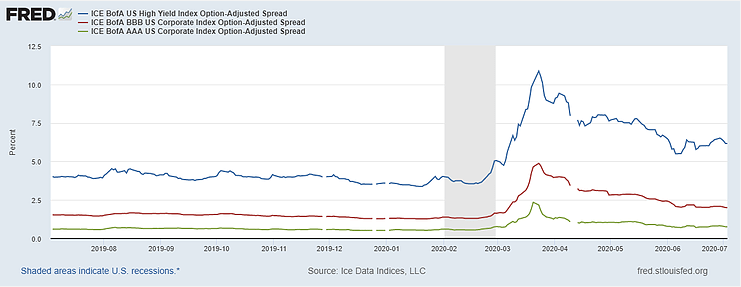

Torsten Slok at Deutsche Bank (DB) argues that COVID19 peaked two months ago and that the number of news cases continues to fall along with the VIX. He notes, however, that “the speed of progress is slowing.” Slok also observes that despite record corporate bond issuance, dealer inventories of corporate debt remain low. And high yield credit spreads are stable, as shown in the chart below.

As we suggest in the National Mortgage News comment above, maybe the Fed can stop buying MBS now? Indeed, while we continue to worry about an increase in unemployment as the credit default process ripples through the corporate world, market indicators are relatively strong – even if earnings are unlikely to meet the challenge. Thus, there is multiple expansion for stocks, but no earnings growth -- or earnings at all.

The good news is that the credit markets continue to function.

The bad news is that the cost of credit is rising dramatically and is already at highs seen a decade ago.

We expect the June data to be horrendous in commercial real estate and corporate credit, but we also note again that credit spreads remain tight and markets are functioning for deals that make sense. Yet the tenor of things is decidedly deflationary.

“Is the corporate money now sitting on the sidelines available to stimulate the economy; grow the value of financial assets; or to eliminate debt?” ask Dick Bove of Odeon Capital Group. “If the answer is the last option of the three, this would not be good for either the economy or the financial markets.”

We kind of agree with Dick when it comes to the credit situation. We stand at an Irving Fisher moment, when our leaders either take collective action to fight deflation, as we did in the 1930s, or we stand back and watch as “market forces” led by the private equity industry do the work.

The candidate that wants to win in November needs to start talking about restructuring and renewal, the twin national priorities that will assert themselves in coming months to the exclusion of aught else.

It’s fine to buy time with PPP and other measures, but much of America’s economy needs to be restructured and made productive again.

Reauthorizing the Hoover-era Reconstruction Finance Corp with receivership powers and a mandate to work with the Federal Courts and the Federal Deposit Insurance Corp to resolve insolvencies and fund new, restructured companies and banks is the obvious first step.

Which of the two candidates, Trump or Biden, will first figure out this looming economic and political reality?

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.