Below are updates on our twenty-four current high-conviction long and short ideas. We have removed Cummins (CMI) and Alibaba (BABA) from the short side of Investing Ideas this week. We have added ZoomInfo (ZI) to the short side. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

SFM

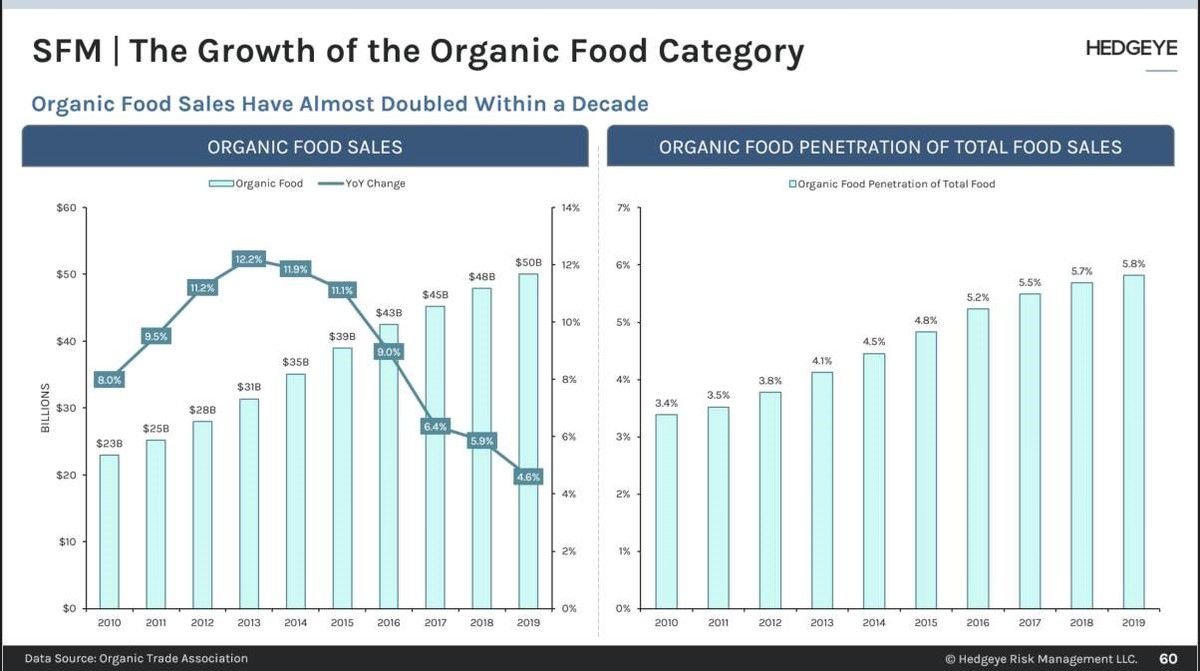

Sprouts Farmers Market’s (SFM) focus on food that is natural, fresh and organic will benefit from consumers looking to eat healthier as a result of the pandemic. Core categories of fresh produce, and vitamins are seeing strength from long-tailed changes in customer behavior.

The company’s smaller store format with higher returns unlocks an open-ended store growth opportunity. Organic food has grown much faster than conventional food over the past decade as seen in the chart below. Sprouts is positioned in the faster growing part of groceries. Its HSD% store growth, accelerating SSS and inflecting margins at a mid-teens P/E multiple is an attractive anomaly.

CHWY

An important question around Chewy (CHWY) is how does it differentiate from Amazon and protect share vs powerful competitors. The differentiation comes from the fact that Chewy is focused in a single category. It’s site, logistics, and customer service are all designed to better serve pet owners. If a consumer is looking for a quick convenient price driven shopping experience, perhaps Amazon is the way to go.

But if the consumer wants help in the decision process, needs some curation of product recommendations specific to his or her pet needs, and wants more confidence in quality of the product and the experience, then CHWY makes more sense. The pet space is one that has seen higher levels of humanization of animals in the home, meaning the owner considers him or herself to be a parent, and the pet an important member of the family.

In that context, the value proposition that CHWY presents is far superior than Amazon, especially with the consumer likely to spend the most money on their pets.

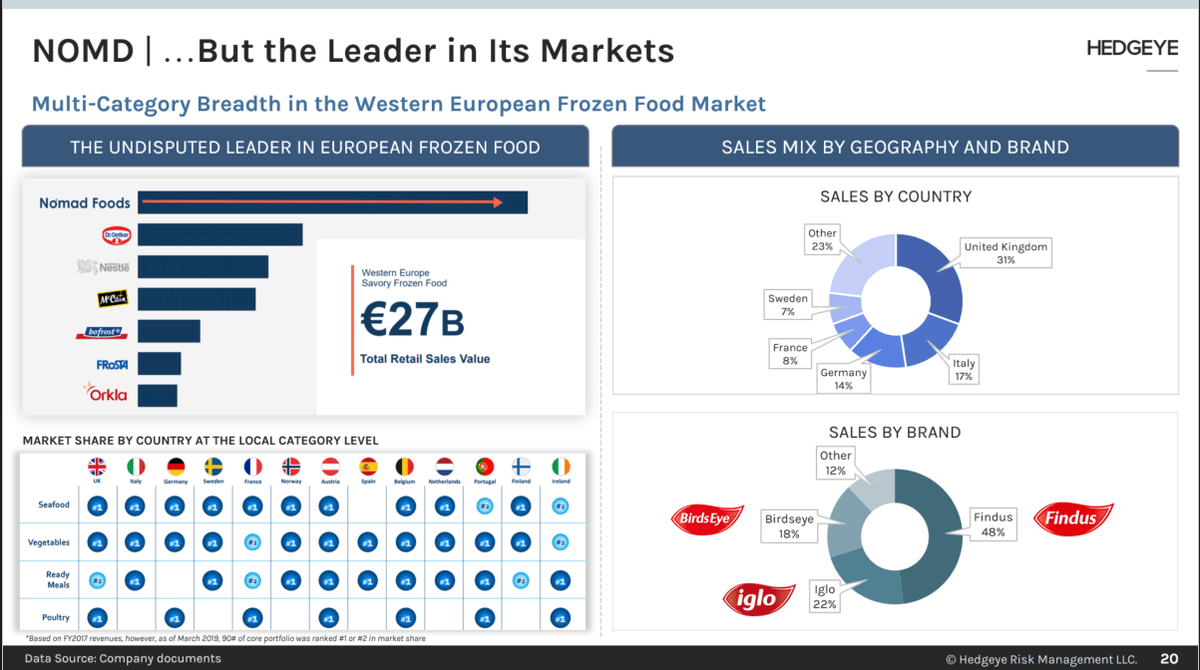

NOMD

UK supermarket sales increased 13.7% in the 12 weeks ended June 14 covering the pandemic period, according to Kantar. In the most recent four weeks ended June 14 sales accelerated to 18.9% from 17.2% sequentially.

The frozen category has outperformed the rest of the supermarket in the UK as in the US. INNOFACT, a German market research firm carried out a consumer study on behalf of the German Frozen Food Institute. According to the study 98% of household purchased frozen food prior to the pandemic.

A third of those surveyed intensified their use of frozen food during the pandemic. The top three categories that saw increased purchases were vegetables, fish and pizza. 18 to 39 year olds rated frozen food much more positively than before the pandemic. For 72% of the respondents the most important reason for purchasing more frozen food is the long shelf life. Vegetables, fruits, potato products, fish and bread rolls received the highest ratings.

14% of respondents said they would purchase frozen food more often.

Nomad’s business mix by country can be seen in the slide below, with the UK at 31% and Germany at 14%.

CAG

Total grocery sales increased ~10% in the week ended June 7 according to IRI, three months into the pandemic. Center-store edible growth outperformed with a growth of 13.7% driven by meat and produce while deli and bakery were offsets. The fresh food perimeter of the store grew 11.2%, outperforming the entire store.

Frozen food growth of 20.4% continued to lead center stores and fresh foods. This is despite the continued out of stocks in frozen foods. According to IRI, assortment variety was down 7.7% in frozen food. The assortment availability was worst in frozen pizza -19.8%, followed by frozen fruit -9.5%, prepared vegetables -15.9%, and frozen entrees -13.4%. The outperformance of frozen food continues to point to consumers still in stocking up when it comes to grocery purchases.

Frozen and refrigerated foods are roughly 40% of Conagra’s (CAG) sales.

FLO

Grocery sales continue to be elevated during the pandemic. Two departments in the grocery store that have underperformed are the bakery and deli section. In some stores those departments are closed. Both departments also involve the most interaction with store employees which may also explain the weakness.

Flower Foods (FLO) packaged bakery items likely benefited from customers skipping the bakery departments. Flower Foods is the second largest producer and marketer of packaged baked foods in the US. The company is well positioned to benefit for the continued strength in the grocery channel.

ZM

When we presented our ZM Long a few weeks ago we used our Invoice tracker to predict Billings and Revenue growth for Zoom's April + July quarters. The lofty level of our estimates caught the most amount of pushback from clients and yet ZM still put up a billings # that was 2x what we had thought for F1Q and fulfilled our expectations for F3Q billings already in F1Q.

Management decided to guide revenue flat from 2Q into 2H FY but in order to achieve that lowly guidance the company would have to lose over $200MM of quarterly revenue in churn with $0 offset from incremental customer additions, expansions, or upsells. We can theoretically argue peak as much as we want but as long as ZM is making higher highs in billings we aren't there.

Stellar results and momentum + ongoing increases in pace of billings + heavy conservatism in guidance + a future product with revenue potential as great as the first = buy.

ZM remains a Hedgeye Technology Best Idea Long.

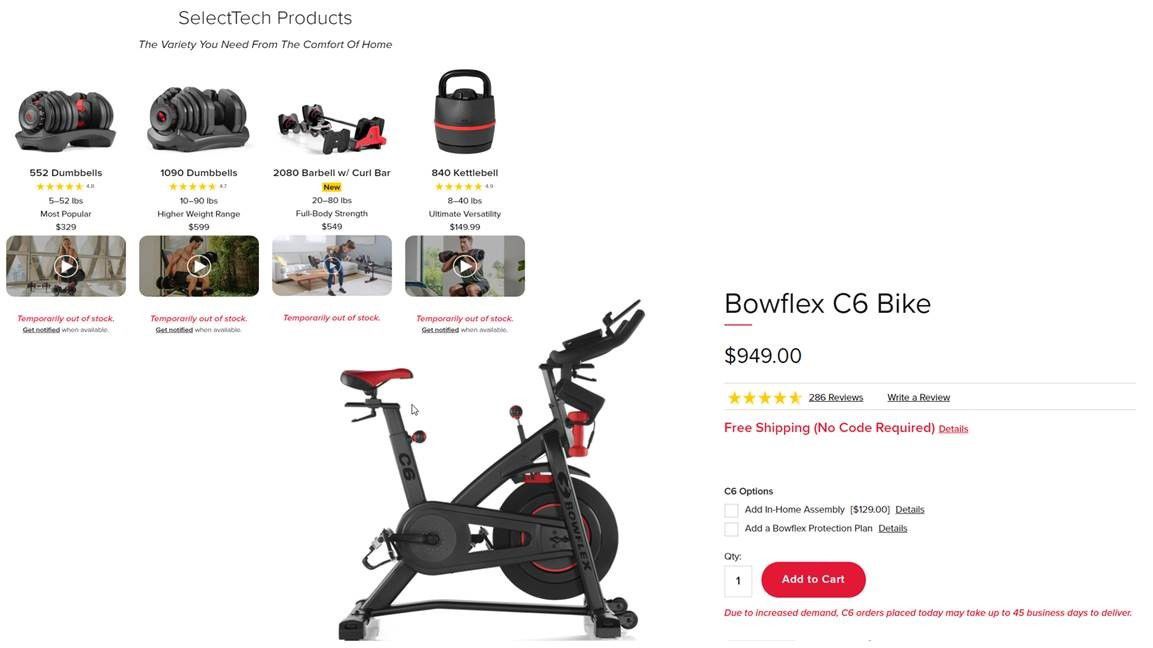

NLS

Covid-19 new cases in the US hit new highs this week, and demand for home fitness solutions does not seem to be losing any steam. For Nautilus (NLS) the high demand is a positive, but it also presents a challenge in keeping up with demand with supply chain still not working at normal levels.

Check out the site snapshots below, Bowflex is out of stock of many key products, and the leading bike model has a 45day back log. What we think this means is that the demand is being spread over many months, not just a couple.

That makes for an extended duration of elevated revenue growth, on top of what we see as likely at least 6 more months of elevated demand. So as long the supply chain can keep product moving there is likely upside to NTM sales and earnings.

Source: Bowflex.com

ONEM

After finally “flattening the curve,” many businesses began looking for the best methods to “re-open” their daily operations in a way that made their employees and customers feel safe when returning. For many of us, the “new normal” of living in a world that couldn’t afford to be shut down any longer, but still did not have a COVID vaccine or therapeutic was anything but “normal.” The effects of COVID-19 have and will continue to structurally alter the way in which health care is consumed (evidenced by our work in telemedicine) and physicians choose to practice.

Our 1life Healthcare (ONEM) thesis combines both aspects well and has been successful throughout the initial surge in cases, as well as, the recent re-acceleration of caseloads in the US. We continue to track physician counts weekly, and HR hasn’t missed a step in hiring new providers. For this reason, we believe that ONEM is more than a “doc in a box” platform, but an attractive primary care partner to businesses throughout the country looking to provide their employees with a benefit program that caters to them.

We remain Long ONEM in the Hedgeye Health Care Position Monitor.

MAR & HLT

Click here to read our analyst's original report for Marriott.

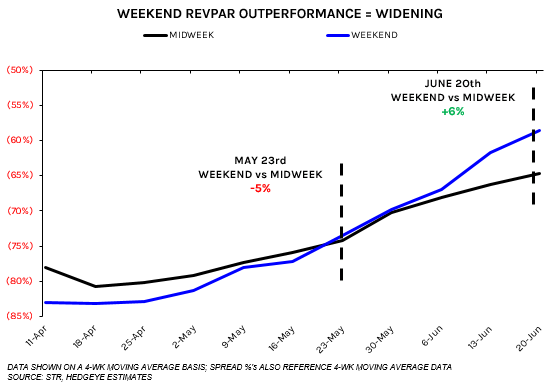

Given that much of April and parts of May were experiencing gradual slowdowns in growth and true trends had not yet solidified for the industry, we think the last few weeks should provide more perspective on how the early stages of the recovery should shake out. Note the outperformance spread weekend vs midweek RevPAR growth starting to widen over the last few weeks as leisure travelers prove to be more interested in getting back on the road and taking a trip. It is true that the midweek is also seeing some gradual improvement, but not nearly to the same degree, and we expect that trend to continue for some time.

We remain firm on the short thesis for both Marriott (MAR) and Hilton (HLT).

MDLA

Medallia (MDLA) reported $3.5MM of Non-GAAP Operating Profit, showing Y-Y incremental operating margins of 7% despite the incremental headcount from acquisitions. MDLA is committing to show positive NG operating profits this year. As such, we expect some gamification there, such as closing Voci in F2Q ($59MM acq) and we will be on the lookout for excess capitalization of costs.

MDLA remains a Hedgeye Technology Best Idea Short.

ATUS

Click here to read our analyst's original report.

We held our Long TMUS institutional presentation last week. As part of that work, we updated the data we track across the broader cable/telco space for employee satisfaction and user reviews. The latest update shows that ATUS continues to rank the worst among peers across all key metrics. While everyone hates their cable company, we would note that Altice (ATUS) ranks worse than Frontier (Which is bankrupt!).

This data is further evidence that ATUS management continues to manage the business with a focus on short-term, financial engineering over long-term value creation. Additionally, ATUS high leverage of ~5.0x Net Debt/EBITDA is a style factor that underperforms in Quad3, which is the Hedgeye Macro teams expectation for Q3.

DFS

As noted in the company's 10-Q, the CARES Act provides financial institutions, like Discover (DFS), with the option to temporarily suspend certain accounting requirements related to troubled debt restructurings.

As of June 7, 2020, $3.3 billion or 4.7% of credit card receivables have been enrolled in the Skip-a-Pay program, up from $2.4 billion or 3.25% reported at the end of 1Q20. Of the $3.0 billion, 30% has been enrolled in a second month of the Skip-a-Pay program.

We remain firm on the short.

SYF

We continue to hold the view that private label card operators are in a curious position relative to their general purpose counterparts due to the risk-sharing and economics-splitting nature of these relationships. On the one hand, these arrangements serve to insulate the issuer, but on the other hand, this risk-sharing may catalyze a liquidity event on the part of certain retail partners.

In accordance with its credit and collection policies, the Servicer has granted forbearances to certain accounts in connection with the COVID-19 pandemic. Those accounts receiving forbearance relief may not advance to the next delinquency cycle, including eventually to charge-off, in the same timeframe that would have occurred had the forbearance relief not been granted.

Accordingly, with both private label and considerable subprime consumer credit exposure, Synchrony Financial (SYF) is on the front lines of this COVID-19 downturn.

MCD

Click here to read our analyst's original report.

McDonald's (MCD) sales have lagged its QSR peers during the pandemic due to its international exposure where stay at home restrictions kept more people at home and its much larger breakfast business.

Consumers are eating more breakfasts at home as they "attend" school and work "virtually" from home. McDonald's sales have benefited from its drive through windows and less competition from other restaurants that have remained closed with their dining room capacities limited.

The company also reported $10.7 billion in EBITDA in 2019, implying that all the pandemic has cost MCD was one year of growth. Will the street ever care about declining profitability and a business model that may be challenged for more than 12 months?

ITW

ITW looks to be at risk of a sizeable 2020 reset on consensus estimates, with very optimistic justifications focusing on bailout (‘cash for clunkers again’) and other stimulus measures. We see 30% relative downside in shares of ITW, a name that every few years gets re-rated as a mediocre, discounted conglomerate.

Auto sales dropped by about 1/3 sequentially and YoY, a pace that was almost certainly worse toward the end of the month as social distancing efforts increased. According to our Macro team’s Christian Drake, a “primary read-through is to Retail Sales where autos represent ~20% of the Total.” In many ways, the dynamics of this downturn are likely to hit demand for ‘consumer’ exposed companies like Illinois Tool Works (ITW) more than some traditional manufacturing names with transportation, construction, government spending, or defense exposure.

As we flagged in our ITW deck, used car prices are likely to fall, potentially impacting financing. We remain with the short thesis.

SYY

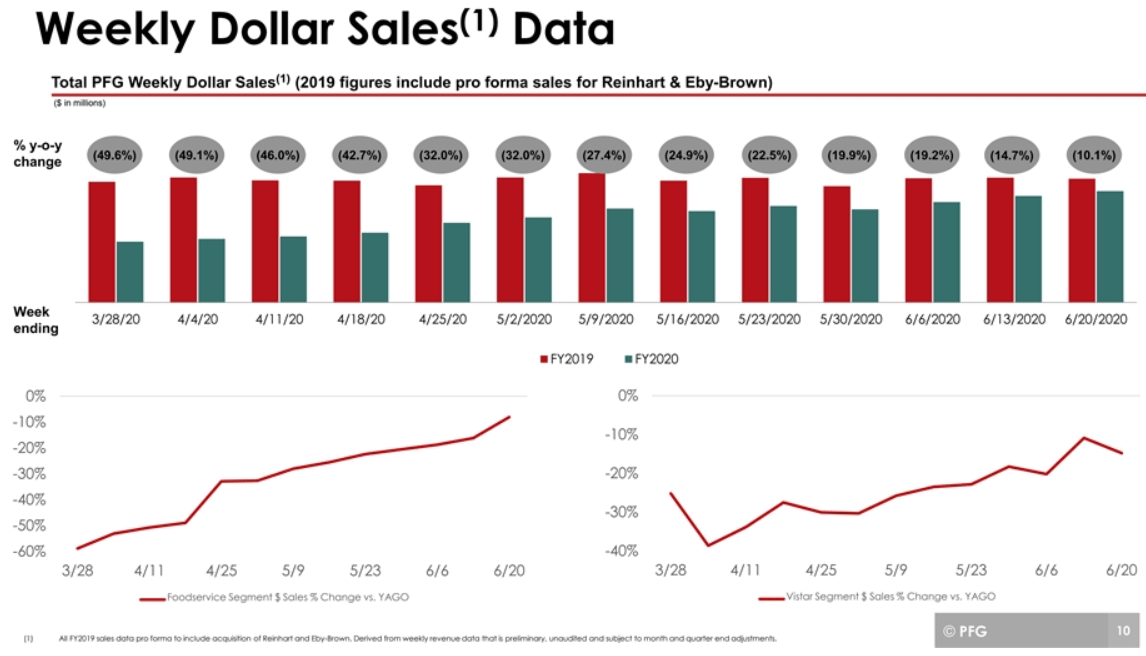

At an investor conference this week Performance Food Group disclosed that in the week ended June 20, sales only declined by 10.1%. We believe that Performance Food Group has the best management team in the food distribution sector as well as a better business mix than Sysco (SYY).

The steady improvement, especially over the two most recent weeks, is encouraging, and we would like to understand the drivers better. The company’s slide included below presents weekly sales, not a like for like customer comparison or case volumes. Inflation, especially in beef, would benefit sales without benefiting the bottom line.

Sysco said its sales continue to improve sequentially as well and has accelerated recently as more states open. The differences in customer mix account for a lot of the gap in performance between the two companies.

Performance Food Group has more exposure to the pizza category (which has been the category winner with its delivery service) and more exposure to Europe which has taken a more measured approach to reopening restaurants. The reopening phase has not been smooth as seen in Texas on Friday shutting down bars again and reducing the dining capacity of restaurants. Sysco’s share price is discounting a quick recovery in restaurants, which looks to be too optimistic given the situation at the restaurant level.

GOLF

Click here to read our retail analyst's original report.

Temporary Coverage Restriction Notice – Acushnet Company (GOLF)

From time to time, during the ordinary course of conducting our investing research, circumstances or events outside our control can cause us to temporarily restrict or halt our research coverage of a specific security. It’s inconvenient for Hedgeye analysts and our subscribers.

But we believe it is the appropriate and ethical way to conduct business.

Please be advised that Coverage of Acushnet Company (Ticker: GOLF) has been temporary halted at this time. We hope to resume coverage soon. Unfortunately, we cannot comment further and are unaware of exactly when we will be able to resume coverage.

BYD

Did CZR act because it was tipped off that executive action was coming and wanted to look good to its employees? Twitter is debating this as we speak but for us it doesn’t really matter. Wednesday afternoon, CZR trumped the Nevada Governor by announcing that the company would require visitors to wear masks in all public places throughout their Las Vegas properties.

Later, the Governor issued his own Executive Order mandating masks in all public places throughout the state that went into effect this past Friday (6/26). We’ve been worried about a mask mandate over the past 2 weeks as Covid cases have escalated in Nevada and surrounding states and reiterate our concern with the impact this might have on casino visitation. In our view, this is a pretty big negative for the Strip, downtown, and Las Vegas casinos like Boyd Gaming (BYD) will all be affected. Already, Kayak had reported declining interest in Las Vegas as a destination this week and that’s before the mask mandate was announced.

AXP

During the first quarter 2020, American Express (AXP) created a Customer Pandemic Relief Program for customers impacted by COVID-19. Delinquency status is generally frozen at enrollment, and loans that are current at enrollment do not age, regardless of whether payment is made. Upon exiting the program, delinquency aging resumes where it had left off at enrollment.

With roughly two-thirds of total revenue driven by card spending, with net interest income accounting for another quarter, American Express is suffering from the dual impact of depressed consumption and mounting credit worries as the world economy nosedives off the Covid Cliff.

IFF

In more normal trading markets, we’d expect International Flavors & Fragrances (IFF) to pop on the garbage Old Wall takes about accelerating growth and whatnot in the quarter, and then trade off. The earnings call will likely encounter some tough questions. Jilla Rustom wasn’t such a bad CFO at MSM, but the spread between the press release and 10-Q here is egregious. A portion of customers aren’t paying, negative mix impact in 2Q is omitted in the press release, restructuring is being drawn out, and a chunk of the operating margin improvement is a Brazilian litigation benefit.

HUYA

HUYA's (HUYA) recommendation banner stopped working this week as it underwent serious rectification. Some of its cultural content was not updated and some went offline. In addition, there was a new minors mode which mentions that some functions have been disabled.

HUYA has been in hot waters lately. First, in early June, the game advertisements during their education courses for kids was scorned by CCTV News. Second, in mid-June, pornographic content appeared in some of its live broadcast rooms and user comments again attacked HUYA.

Furthermore, the State Cyberspace Administration and relevant departments stated that live broadcast platforms such as "HUYA Live", "DOYU Live", "BILI", "Tentacle Live", and "NTES CC Live” have problems of vulgar content.

We remain negative on HUYA.

WORK

On billings adjustments: we are not buying into the $10MM add-back unless everyone agrees to de-book that out of billings when the deal gets recognized sometime in the next three quarters. The $7MM? Fine - for now they keep that as adjusted Billings but really it is typically thought of as a long-term account receivable (i.e. a problem rather than a growth kicker). And if those companies go bankrupt or cannot pay, Slack won’t collect any of that $7MM.

Bottom line, the April-Q billings range – the best Q Slack (WORK) will see for now and a huge acceleration point – is either 38% (reported), 42% (Hedgeye adjusted, with shrug), or 49% (CFO wish list).

ZI

Hedgeye CEO Keith McCullough added ZoomInfo (ZI) to the short side of Investing Ideas this week. Below is a brief note.

I guess some of the Hoodies are thinking ZoomInfo (ZI) is like our Long Idea, Zoom (ZM)? Who knows, but the stock is up into the close and we sell on green...

Here's a brief summary excerpt from Technology analyst Ami's Joseph newest SELL idea:

|

"The net is we believe the company has tail risks on the business model, that its current growth rate incorporates a re-pricing period that is not reflective of adoption demand, that S-1 data points themselves point to a period of steep churn in 2019, and other elements wherein we remain convicted on our ZI Short." |