|

Editor's Note: Below is a complimentary research note from our Housing team of Josh Steiner and Christian Drake. They will be hosting their quarterly housing themes on July 13th @ 10AM. If you are an institutional investor interested in accessing their research please email sales@hedgeye.com. We are pleased to announce that we recently launched Financials Sector Pro, Josh's new research product. Click HERE to learn more |

Today's Focus: June Builder Confidence

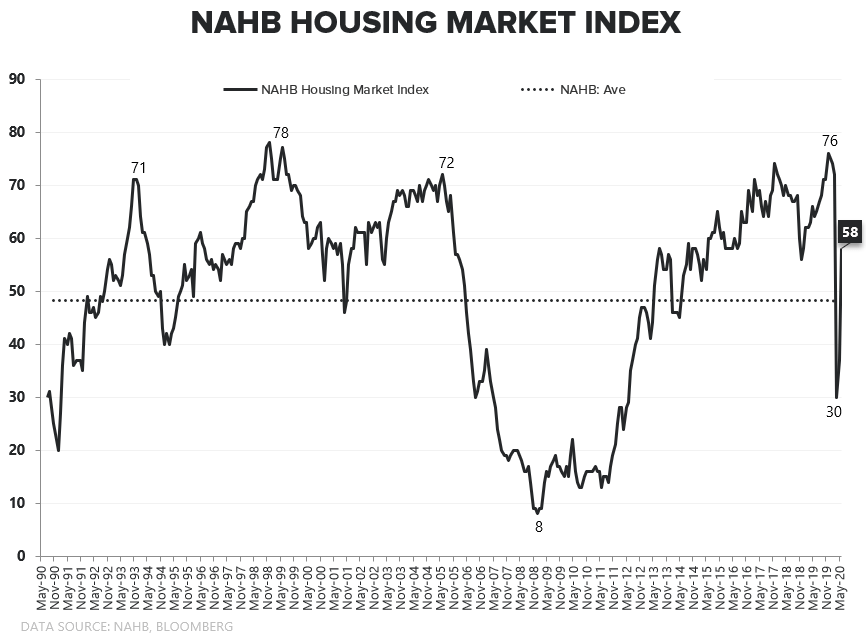

Released just two weeks into the reported month, the NAHB HMI remains one of the most real-time housing and macro indicators.

At times, however, it’s hard to pin down the direction of influence. Is it lagged optimism on the heels of last month's resilience in NHS? Is it a lead indicator of strength in tomorrow’s Starts data? Is it (partially) a finicky reflection of a shifting mosaic of other dynamics – be it Purchase Apps, interest rates, or the headlines and broader contours of the evolving macro or equity market narrative? Is it some amorphous mix of all of it?

Going strictly by movement across the constituent subseries, the mix interpretation appears most apt, at least for June. Indeed, while Current Sales and Traffic both showed a meaningful improvement, 6M Expectations rose even more, pushing the “Optimism Spread” (Expectations less Current Activity) to a 4-year high.

In any case, this month’s gain requires little in the way of rationalization. The latest data have been positive and the transition from mandated cessation in economic activity to large-scale re-opening and the realization of deferred consumption always promised to produce an initial and mechanical step-function jump in activity.

It is worth re-highlighting, however, persistence in present conditions may help re-cultivate the if-you-build-it-they-will-come dynamic for new construction:

- Lower for longer has effectively morphed into lower forever and with yield curve control seeming like an inevitability, rates should remain a protracted support to purchase appetite.

- All-time tight supply conditions in the existing market remain a marginal positive for New Home demand ….

- … and NHS demand skews towards a higher income demographic – the demographic that has, thus far, been more insulated from the COVID related labor market fallout, would disproportionately benefit from asset price reflation while also (probably) carrying a higher proclivity/capacity to take advantage of any fledgling push towards de-urbanization.

- New Sales and Construction activity remained suppressed relative to historical housing cycles and had recovered far less than existing market transaction volume.

In short, to the extent the above conditions hold, New Construction stands to benefit on both an absolute and relative basis even if larger supply conditions, mortgage credit tightening, and Unemployment cap the upside in total housing market transaction volume.

About the NAHB HMI:

The Housing Market Index (HMI) is based on a monthly survey of NAHB members designed to take the pulse of the single-family housing market. The monthly survey has been conducted for 30 years.

The survey asks respondents to rate market conditions for the sale of new homes at the present time and in the next 6 months as well as the traffic of prospective buyers of new homes.

The HMI is a weighted average of separate diffusion indices for these three key single-family series. The HMI can range from 0 to 100, where a value over 50 implies conditions are, on average, improving, a value below 50 implies conditions are worsening, and an index value of 50 indicates that the housing market is neither improving nor worsening.