|

Below is a complimentary research note from our Gaming, Lodging, and Leisure (GLL) analysts Todd Jordan and Sean Jenkins. If you are an institutional investor interested in accessing our research email sales@hedgeye.com |

Welcome to another installment of our very own Hedgeye Consumer Travel Demand Survey.

Welcome to another installment of our very own Hedgeye Consumer Travel Demand Survey. With Q1 earnings season now in the books and more data hitting our screens, we continue to see the likelihood that if there’s any recovery in travel this year, it will be led by leisure travel.

We hope this survey should provide an advanced read on how leisure consumers are thinking about their future travel plans. Whether it’s hotel/resort, vacation rental, or ocean cruise, the survey should provide some color on where consumers might gravitate towards once the social distancing and CDC guidelines are slowly lifted.

Consumers remain more partial towards hotels & resorts, but judging by overall travel intent, it’s not a done deal that hotels will recover any quicker than vacation rentals, at least on the leisure side.

Overall, this past week did show a slight uptick week / week for the “likely” buckets for hotels & resorts and cruise while interest in vacation rentals slightly dipped. After ten weeks of running the survey, we would have expected a clearer direction from the data, either decidedly more positive or negative, but interestingly, we continue to see much of the same which includes plenty of indecision, not really a positive, but the rate of change is not overly negative, either.

If you are an institutional investor interested in accessing our research email sales@hedgeye.com.

CONSUMER SURVEY RESULTS

Methodology of Survey

Each week, Hedgeye GLL will receive updated results from their consumer survey questions. Since the majority of GLL is centered around the theme of “travel,” we geared our survey to directly plug into the wants and desires of potential travelers on a 6-month forward basis. Our survey is strictly focused on the US consumer and aims to gauge changes in interest levels across time.

Latest Results Commentary

HOTELS & RESORTS

- A slight pick-up week / week reading for the “likely” buckets, but generally consistent with the data over the past month (reading was 15% vs 15% last week, and 15% the prior week). % for likely to book at Hotels / Resorts still remains well below its highs last month.

- The % of neutral responses ticked down a bit vs last week suggesting the indecision spilled over into both the “likely” and “unlikely” buckets.

- Net/net, the survey spread between “likely” and “unlikely” for Hotels / Resorts was flattish week over week, though remained fairly negative. i.e. the spread between those unwilling and those willing to book remains near the highs.

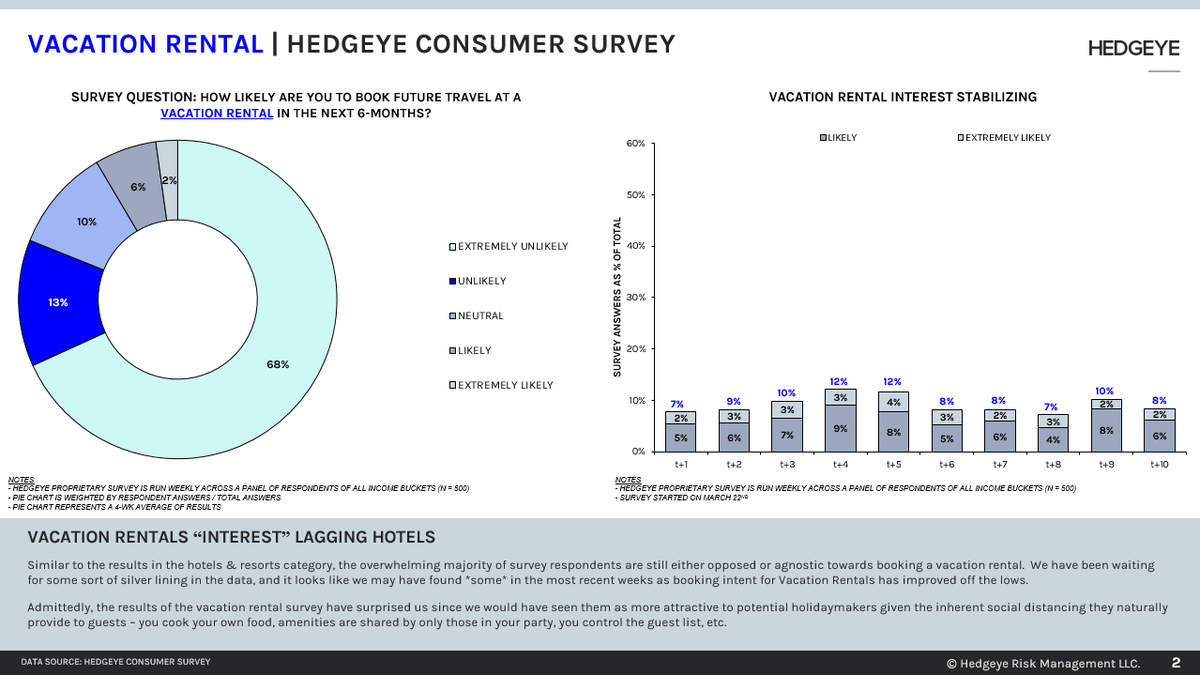

VACATION RENTAL

- After making its biggest weekly jump last week, the Vacation Rental option in our survey saw interest tick a bit lower this past week, but still remains off the lows. (reading was 8% vs 10% last week, and 7% the prior week)

- Neutral responses remained flattish week / week, so the majority of the change leaned more negative and went into the “unlikely” buckets.

- Net/net, this past week’s reading for Vacation Rentals skews less positive than it did last week, but the delta between “unlikely” responses and “likely” are still in better shape than they were just a few weeks ago.

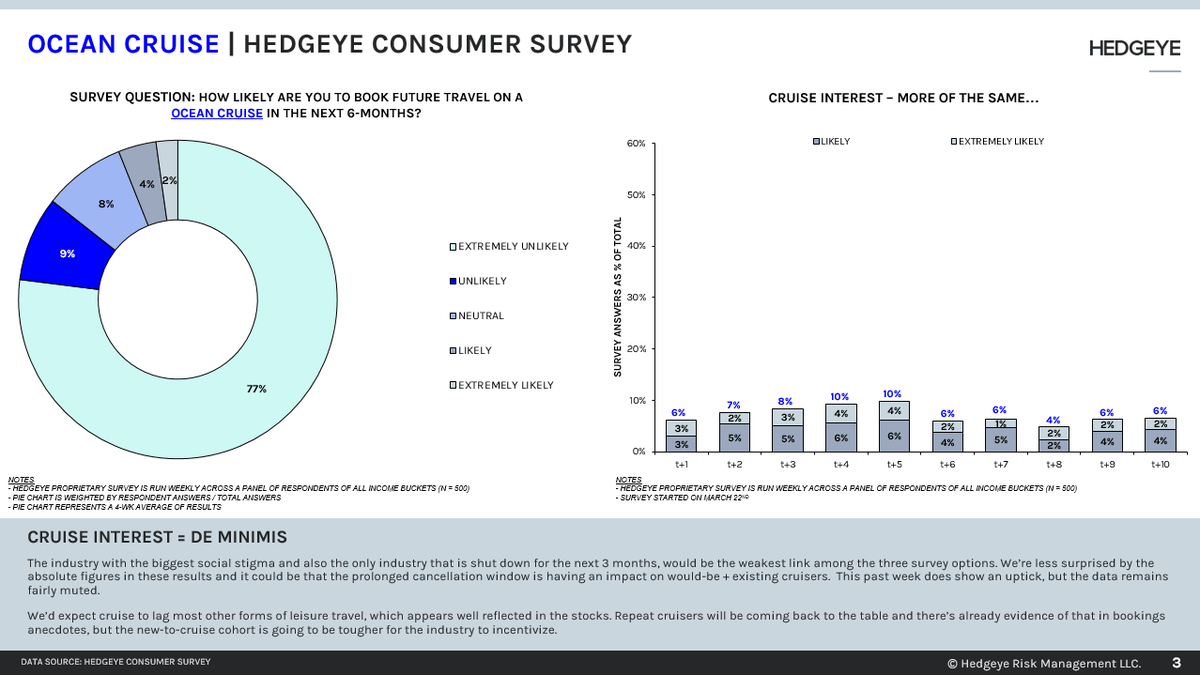

OCEAN CRUISE

- Reading for likely/extremely likely saw some slight improvement week / week but the data was still near the lows (reading was 7% vs 6% last week, and 5% the prior week)

- The % of neutral responses were lower this past week, as some indecision fell into both the “likely” and “unlikely” buckets

- Net/net, the survey for Ocean Cruise skews marginally more negative than it had last week, but the survey does indicate some modest improvement off the lows we saw just a few weeks ago.

- Overall, pessimism towards cruise continues to remain elevated, likely a bad sign for future new-to-cruise demand. However, demand shortfalls for new-to-cruise continues to be offset by growth in repeat customer segments.

If you are an institutional investor interested in accessing our research email sales@hedgeye.com