Below is a complimentary excerpt from a Demography Unplugged research note written by Hedgeye Demography analyst Neil Howe. Click here to learn more and subscribe.

|

Millions of Boomers are reaching the end of their working lives with little or no savings, a trend that’s set to worsen in the coming years. This piece, which interviews six Americans ages 57 to 74, offers a glimpse at the hard choices they’re facing and what they’re doing to get by. (The Washington Post) |

NH: This is a great article, brimming with poignant anecdotes and fortified by citations to research. It is also a profoundly depressing commentary on the deteriorating standard of living Boomers can look forward to in their retirement. I've written often on the reasons why this is happening. See "The Old and the Bankrupt," "Why Are Seniors Flipping Burgers," and "Boomers Stuck in 'Low-Quality' Jobs."

Overall, Boomers will not do as well as the last generation (the Silent) in retirement. See the first chart below, which shows that, in 2014, Americans born in the late 1930s (at age 73 to 83) actually had a higher average and median net worth than Americans born in the late-1950s (at age 55 to 59). In fact, the financially best-off Americans in retirement were born in the early to mid-1940s--which means they are either late-wave Silent or early wave Boomers depending on where you want to draw your generational boundary.

Later-born Boomers have generally been worse off at every age, which is why--now that these late-wavers are approaching age 65--hardship in retirement is attracting more media attention. (See also "The Graying of Wealth.")

One of the biggest challenges for today's new Boomer retirees is the rapid decline in the prevalence of defined-benefit pensions. As for defined-contribution pensions like 401(k)s, barely 40% are eligible to participate. And even those who do participate borrow against them, fail to roll them over, or are forced to take early withdrawals (in the face of events like the pandemic lockdown).

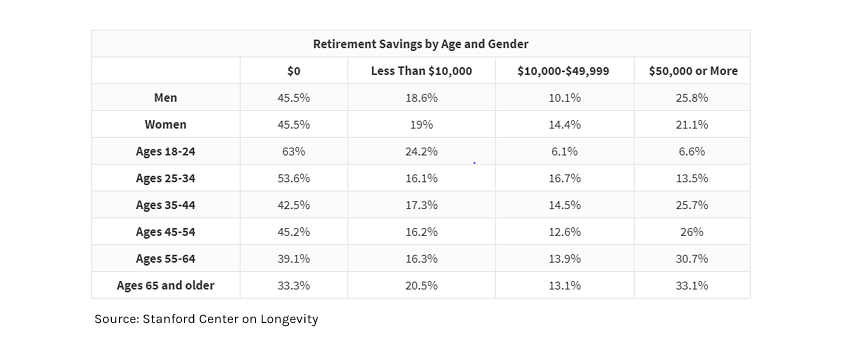

For some truly alarming statistics, look at the table (below) tabulated from a 2019 survey by GOBankingRates. Even at age 55 to 64, 55% of Americans had accumulated less than $10K in retirement savings. Less than a third has more than $50K.

"We’ve probably peaked in terms of retirement security--and it’s not great," said Monique Morrissey, of the Economic Policy Institute. "And now it’s all downhill. Unless something changes, we’re going to start seeing much more hardship." Yes, with senior employment bound to fall in a Covid-19 world, I think that describes the situation pretty well.