|

Below is a complimentary research note from our Retail analysts Brian McGough and Jeremy McLean. If you are an institutional investor interested in accessing our research email sales@hedgeye.com |

To anyone who’s paying attention to the state of global retail, Under Armour’s (UAA) 1Q results should not come as a surprise.

The business was doing what it should have done through the first two months of the quarter, then it got its clock cleaned in March and is currently sitting on nearly a billion in aging inventory that will need to be marked down throughout the year.

No surprise.

The reality is that 80% of the company’s global distribution was shut down for the majority of 2QTD, and though its own DTC/ecomm is a nice offset (it has 2x the ecomm penetration vs Nike), the reality is that we’re looking at 2Q sales down 50-60% -- the only quantification the company gave as it relates to modeling in a post-Covid world.

Again, no surprises unless you’re living under a rock.

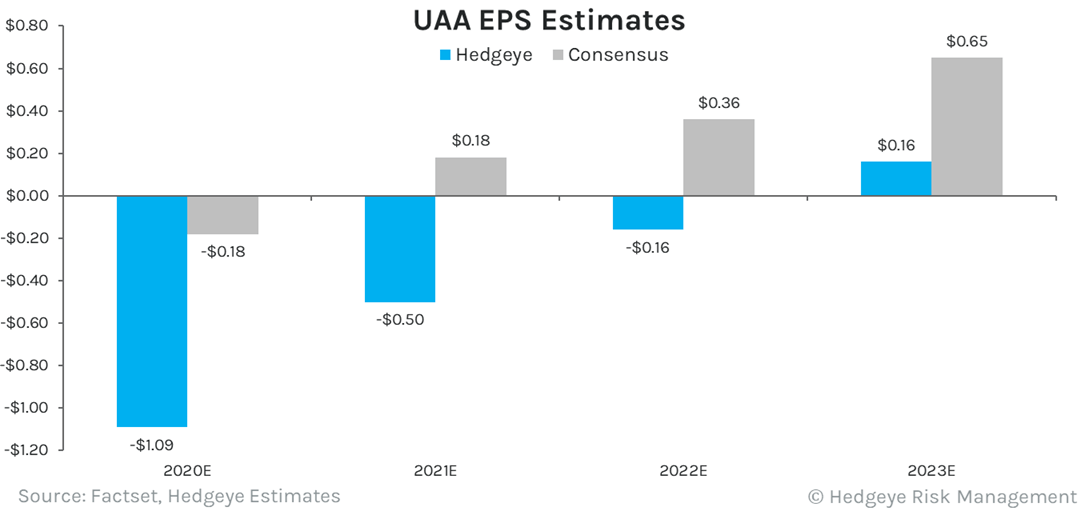

Whether the market knows it or not, I think the reason why the stock is down is that people are finally going through the modeling exercise over a multi-year time period, and the reality is that given fixed cost deleverage, the company is unlikely to earn a profit until 2023. That’s a problem when the Street is modeling a profit in every year after the small loss it’s modeling for 2020.

Perhaps my estimate on the timing of a recovery is too conservative, but all in I’ve got a 26% revenue decline for this year (-17.5% in 2H), and then +15% in 2021, and 10% in 2022 and 2023. In effect, the narrative around $0.75-$1.00 in underlying earnings power is being pushed out by two years, and the consensus estimate needs a massive downwards revision. But again, this seemed clear to me with the stock trading under $10.

One point that is worth hitting on is that as beared-up as our model is (I’d call it realistic rather than bearish) UA won’t need to tap into capital markets for cash needs. The irony is that UA is in the basket of companies that will come out of this recession much stronger than when it went in, particularly as it relates to previous reliance on the off price channel for sales. This allows the company to rip the band-aid off that one pretty transparently.

If we’re looking at $1.00 in EPS in year 5, we’d give this a 25x p/e without beating an eyelash – low by UA historical standards. Discount that back by 10% annually to today’s dollars and you get to a stock in the mid-teens.

I know stocks don’t trade explicitly on discounted earnings, but the stock trading at $8 borders on obscene as it relates to what implies about the long-term defendability of this business model.

UA is on our Long Bias list – added after the stock’s implosion post the 4Q results after being a long time short -- and once consensus estimates get in the ballpark of economic reality – it’s a strong candidate for a Best Idea long side.