This guest commentary was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

The great sucking sound heard last week was the release of accumulated froth in the global equity markets.

The FOMC’s decision to act with a 50bp cut in the target for Fed funds had little effect on real markets for real counterparties. Meanwhile, the panic in the media is having outsized consequences for people, companies and society. Below we ponder the effects and consequences.

The unfolding impact of COVID19 changed the effective ratings for dozens of corporate issuers, resulting in an increase in the effective cost of equity finance for everyone from American Airlines (AAL) to Amazon (AMZN). And the fact that the Fed dropped the target for federal funds is nice, but does nothing really to help these and other companies. Assets move for ratings, a fact we learned long ago from Bob Salvaggio at AMBAC in the world of RMBS.

John Dizard writes in the Financial Times on the topic of Fed interest rate announcements:

“The actual rates at which even most institutions can borrow against Treasuries or government backed securities have not been cut by any 50bp. On Tuesday, the widely used DTCC GCF Repo index quickly rose from 1.6 per cent at the open to 1.85 per cent, and only came briefly down to 1.5 per cent before creeping up again. The index settled at a 1.72 percent average for the day. By that evening, “ease” or no ease, the Fed was turning down some of the record $111bn of bids for repo from within its own select circle of counterparties.”

Because so much of the world of monetary policy is predicated upon maintaining consumer confidence, and since the availability of credit impacts same very directly, times of market stress are costly to the economy. The Fed now faces a sudden, twin crisis of both liquidity constraint and sharply discounted credit profiles for some major corporate and public sector names.

The Fed’s 50bp was thought to be a way to reinforce confidence, but instead it signaled that the worst is yet to come. Treasury Secretary Hank Paulson’s suggestion that the government had to buy bad assets from Citigroup (C) over a decade ago had a similar effect.

Robert Eisenbeis at Cumberland Advisors asks whether the Fed wasted 50bps last week. Our thought is probably yes. Nobody in the mortgage industry is going to agree with you on that count, however, with secondary market spreads north of two and one half points and widening. He writes:

“The Fed’s move was clearly intended as insurance designed to convince participants that the Fed will do what it takes to support the economy in the face of the coronavirus threat. As the day proceeded, however, the realization set in that rate cuts aren’t medicine when it comes to the threat of a pandemic. It can’t get consumers out of their homes to spend and it can’t fix supply chain bottlenecks.”

The first question, of course, is whether the virus panic now being fanned in the global media and also in the political sphere is going to cause a global credit crisis and recession. Specifically, and to the questions about the efficacy of last week’s Fed rate cut, is merely adjusting the target for Fed funds sufficient to meet the growing demand for the volume of credit? Specifically, will the hit to the supply chain also cause crippled corporate credits to lean hard on bank lines and other sources of liquidity.

“Just cutting funds and IOER without backstopping liquidity is going to make USD funding offshore a nightmare in coming days as the global supply chain (which is a payments chain in reverse, thanks Zoltan) clogs and backs up like bad plumbing,” says Ralph Delguidice of Pavilion Global Markets. “Companies not shipping high value-added goods (chips, etc) will draw down USDs to make payments to fill the gap (resulting in a temporary surfeit of liquidity). This will become a global scramble for dollars among those banks seeing deposits flee and credit lines drawn the longer the chain stays disrupted.”

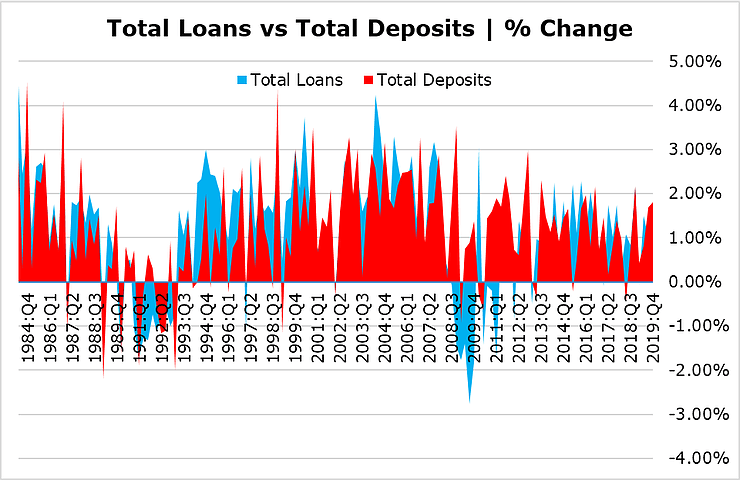

As the chart above suggests, the FOMC has managed to throttle bank deposit growth since December 2018. Strangely, this is when the central bank stopped raising rates and started to become aware of ST liquidity risk. With the shock to the global supply chain will also come a shock to commercial banks, first in terms of increased volatility in once stable corporate deposits from longtime customers. Later these same customers may come under financial stress or even be forced into default and restructuring due to the disruption of COVID19.

Liquidity, like confidence, is something that economists discuss endlessly but cannot define or measure. We constrain bank liquidity with rules and regulations, but then lament when funding is insufficient to meet market demand. And cash liquidity available to the broad market, not the target rate for Fed funds, is what gets stuff to happen in the economy such as loan growth.

In fact, the volume of liquidity flowing through GCF repo for Treasury collateral has been falling for the past year even as interest rates have fallen – or rather have been pushed down by the Fed. GCF RMBS repo volumes have been strong, of note, even as new loan origination volumes climbed 20% year-over-year.

As with this past September and December 2018, when we took large cap stocks off by a third in value, the forward concern seems to be liquidity risk resulting from numerous examples of falling corporate cash balances and deteriorating credit conditions. We cannot see whole industries such as airlines, lodging and hospitality grappling with sharp cuts in revenue and not expect a substantial reaction in terms of reducing costs and raising liquidity in those sectors.

Another worry when it comes to liquidity is the new issue market, which was going great guns in January but may have slowed significantly in February with the notable exception of mortgage securities. At $158 billion in January, RMBS volumes were up 25% YOY according to SIFMA. But more worrisome is the fact that corporate and ABS bond issuance has fallen dramatically since September of 2019. This may have been the early sell signal from the world of credit in this cycle.

We’re struck by the fact that corporate debt issuance started to dive five months ago, but the equity markets did not respond until the arrival of COVID19. In fact, after a small pop in high yield (HY) spreads in the September 2019 time frame, HY credit spreads actually rallied 50bp in yield down to the mid-300s over the curve by early 2020. With the arrival of COVID19, however, HY spreads have widened to plus 500bp over, dangerous territory that can be a predictor of an impending credit risk reset event.

Fred Feldkamp’s First Rule states simply that when HY spreads go much about 400bp over the swaps curve, financing activity on the fringes of the consumer economy slows as counterparties start to demand wider spreads on risk transactions. Get to plus 500bp as we are today and the economy is in danger of an outright stall. An economy is an airplane that never actually takes off but must always be at least at sufficient autorotation speed necessary for flight.

Falling volumes in the GCF repo market, stagnant bank deposit growth and a sharp drop in corporate bond and ABS issuance don’t sound like a particularly positive combination to us. Add a likely spike in cash demands by a range of public and private obligors whose effective credit ratings changed over the past week and we see a variety of immediate and long-term problems facing the Fed and the Trump Administration.

For starts, we think the Fed should worry less about targeting interest rate price and more about understanding, intimately, what is happening in terms of apparent and real liquidity in the credit markets. Like we said, assets move for ratings. There is a huge, sudden and somewhat hysterical asset allocation shift underway out of equities and into safe assets due to uncertainty arising from COVID19.

At some point, however, the lack of yield in bonds will drive investors back into equities.

ABOUT CHRISTOPHER WHALEN

Christopher Whalen is the author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington.

This piece does not necessarily reflect the opinion of Hedgeye.