The Powell Fed panicked yesterday.

As 1) global asset markets were nosediving 2) rates futures fully pricing in a 50 basis point cut for March and 3) investors facing a deepening Quad 4 outlook, the Fed attempted to placate anxious investors with an emergency 50 basis point cut.

It didn’t work.

Shortly after the news broke, Hedgeye CEO Keith McCullough held a flash webcast updating investors on the key investing implications.

Here’s a taste:

|

"The economic conditions and the market volatility being what they are it could certainly perpetuate a potential stock market crash. It wouldn’t be hard to have a -20% decline from its most recent all-time high. We’re already more than halfway there… The last time the Fed cut interest rates by 50 basis points was in 2008. Not a good reference point. The last time we had a market up day like yesterday (up +4.6%) was back in October of 2008." |

Below we’ve transcribed critical callouts from this webcast. Click to watch the entire 30-minute discussion.

TRANSCRIPT

Daryl Jones: Welcome everyone. Let’s get right into it. Alright Keith, we got the cowbell. Now what?

Keith McCullough: Indeed we did. But we did not get the market reaction that many of those people want. A lot of people think it’s all about Fed liquidity. This could change but this was a panic rate cut by Powell and I think markets could panic.

I’m not trying to scare anyone but trying to give you a proactive plan for what could happen here. The economic conditions and the market volatility being what it is certainly could perpetuate a potential stock market crash. It wouldn’t be hard to have a -20% decline from its most recent all-time high. We’re already more than halfway there.

I’m just trying to prepare you for the Quad 4 economic reality. That’s when you have both growth and inflation slowing at the same time. In this case, the Fed is cutting rates but they can’t reflate the assets that are falling.

What did the Fed just do? The last time the Fed cut rates by 50 basis points was in 2008. Not a good reference point. The last time we had a stock market up day like we had yesterday – of +4.6% on the day – was back in October of 2008.

Everyone probably felt “good” about that move. The S&P 500 got back above its 200-day moving average and that sucked a lot of people in thinking it was the “all clear signal.” So then the Fed cuts by 50 basis points and you’d think that the stock market should be up a ton if everyone actually thought the economic scenario was solved by the Fed.

Of course the market doesn’t believe that. So now we have the same volatile set-up, the same economic conditions and we have a Federal Reserve who shot their bullets. What do you expect them to do next? Do they have to cut rates every day?

Now let’s focus on part B of this. Once the Fed goes to the fourth, fifth, sixth rate cut that’s not a good thing. That means that the Federal Reserve understands that the U.S. economy is slowing.

Don’t forget that the entire bond market has been front-running the Fed on the U.S. economy peaking and slowing since the end of Q3 2018. Bond yields have only gone down since that point. That’s why we’ve been long bonds, bond proxies (which include REITs, Utilities, Consumer Staples) and Gold. These are the things that like it when real yields go down.

This is the game that’s been front-running the Fed for some time. That doesn’t mean it can change its course. As the Fed goes to the fourth cut, it’s a lot different than going to the first cut or not raising rates in Q4 of 2018 to dovish very quickly.

Don’t forget 2001. The Fed cut by 100 basis points and the stock market went down in a straight line. There’s a lot of history to be aware of instead of just flailing listening to political opinions or what should happen in markets.

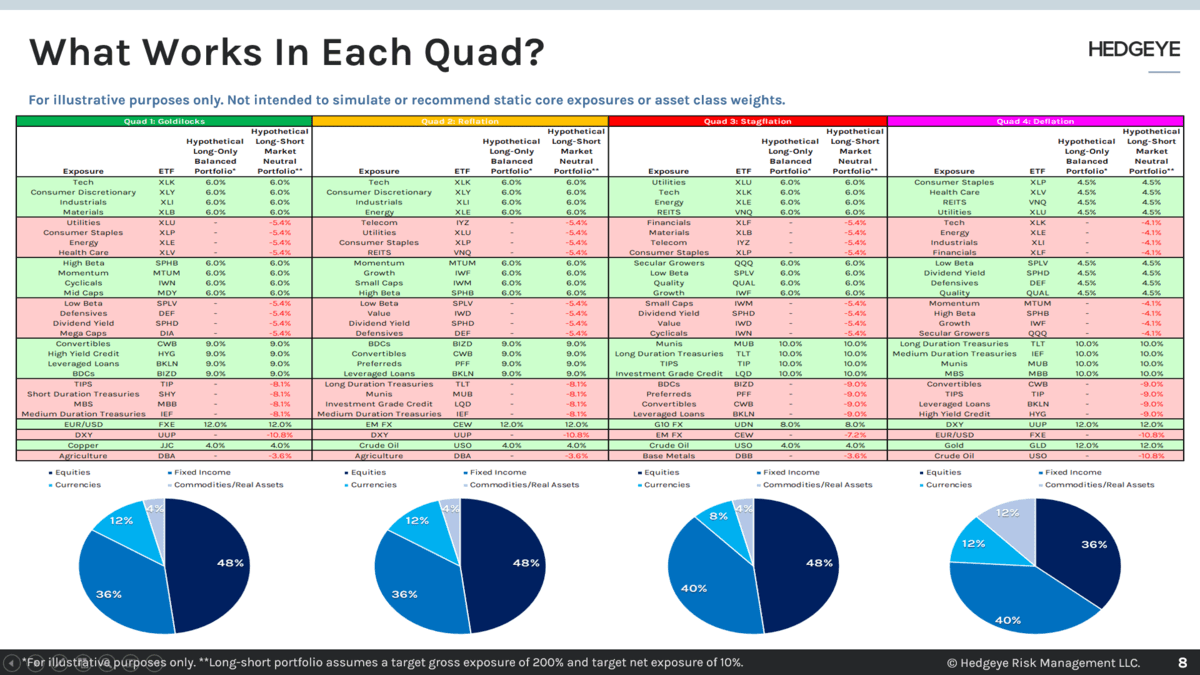

Now what is the market doing today. You have Treasuries up, Gold up, Utilities up, Consumer Staples, REITs and Housing up. What portfolio is that? That’s Quad 4. This is playbook 101 to Hedgeye subscribers.

On the short side, what’s not working today? The things that go down in Quad 4… Tech, Energy, Industrials, Financials. The point is clear. The market is trading on Quad 4 no matter what a central planner of economic gravity thinks he can, should or would do. So you would be set-up that way anyway.

There are two economic factors that matter most. There’s the rate of change of growth and inflation. Those in due course affect the rate of change in corporate profits and the jobs market. In other words, if you get the rate of change in growth and inflation right you’re going to get everything else right. You’re going to get your asset allocations right and the sectors within the market.

When you’re sitting there having some kind of visceral reaction it is what it is. It’s not about our emotions. It’s about the prevailing conditions of growth and inflation.

McCullough: Understand that even if what we think doesn’t happen between now and the end of today’s market close, that there will be time and space between now and the end of the second quarter. We’re not even into the second quarter yet and preannouncements have already started happening – like Visa, Mastercard and Hyatt. The good companies are coming out and telling you the truth first.

The profit decline in conjunction with Jobless Claims is something you need to be watching. That’s the big one. That’s where the Federal Reserve is going to have to panic more. Think about it. The Fed is panicking at full employment. So tomorrow’s ISM Services report should continue to slow. Friday’s Jobs Report will continue to deteriorate.

But the last thing is that people get fired. Jobless Claims are at the low. When they go up, as you can see in the last two times that the Fed cut rates in 2001 and 2008, claims go straight up. People get fired. Profits decline at a faster rate. People get fired. Consumption goes down.

So the whole narrative that ‘The Consumer is great shape,’ is nonsense. First of all, the consumer is in slowing shape. Second of all the consumer is going to continue to slow at a faster rate. That is classic Quad 4.

Now that’s going to take some time. But if you think the Fed rate cut just cured the Coronavirus, you need your head read.

Jones: We’re getting a lot of questions about High Yield. Is that the next big short?

McCullough: It’s been a great short in the past few weeks. Here’s the important thing on that front. Show the chart on earnings. 483 companies have reported year-over-year earnings growth that’s at 0%. So exactly 0.62%. This is pre-virus. I can’t say that enough time.

Energy, Materials, Industrials and even the beloved Consumer (i.e. Consumer Discretionary) have negative year-over-year earnings. So when you think back to what I was saying about the jobs market, whether you’re Wayfair (W) or a profitless company like Lyft (LYFT), you’re now being forced to fire people because you’re no longer forced to be an equity that’s profitless.

People say there are no imbalances. Part of the bubbliness of private equity and venture capital is in the equity market. We said the equity market was at its most complacent and capitulatory risk right on the screws, between February 14th and 18th.

That and the credit market together is the epicenter of complacency. For people to have bought speculative credit right at the rate of change in negative profit growth you’d have to believe Wall Street’s BS that profits have bottomed. This is one of the most ridiculous expectations that would only pass on the Old Wall.

Wall Street says Q3 was the bottom. Everything is going to go up from here. Not only is the rate of change on that assumption wrong but the direction is dead wrong. Earnings could be down -5% to -8% in the next quarter.

Oh, you don’t believe that? You’d only have to go back to 2016 to find that. We made that call too. Back then the weakness was largely in the Industrials, Energy, cyclical space. Now we have weakness in Consumer Staples, parts of Tech that are negative.

This is a very important time relative to expectations in the corporate credit market. The number one way you lose money in corporate credit is when these companies start to lose money.