I’m stopping short of calling BBY a Best Idea short ahead of next Thursday’s print – but am getting increasingly bearish on the name. Cyclical and Secular headwinds are intensifying, BBY short interest is at cycle lows at 2.9%, lowest since 2004, Sell side most bullish in ~4 years, total equity value is back to levels we saw before the recession ($23.6bn), EV(plus leases)/EBITDAR at cycle highs just above 7x. The tariff situation has not been fully resolved. China (where factories are barely staffed) is about 60% of COGS with next year expected closer to 40% as suppliers move sourcing, and margins are 30bp away from management’s 5-year target. Not playing for much on the margin front – so this needs to be a good ‘ol fashioned comp story – something I’m unwilling to bet on. By no means is our thesis baked. We’re not done vetting it and are open to any and all pushback. Here’s our initial thoughts on some of the more critical parts of the BBY business model.

There are a number of product cycles that drive Best Buy and outside smartphones the majority are declining or are in the process of peaking. The company has been making a diversifying push into health care, but it’s too early to know if it will be a success or yet another poor acquisition. Through its own historical expansion Best Buy has over 1,200 big box stores with spare floor space to sell products that are increasingly purchased online. How to better utilize the excess space has driven the company to questionable new forays over the years. With sales increasingly moving online this dynamic shows no signs of abating.

Cell phones have innovation at higher prices

Best Buy’s largest segment is Computing & Mobile Phones which represents about 45% of sales. The industry has benefited from higher ASPs and continued innovation. The replacement cycle has lengthened as new must have technologies in smartphones have given way to an evolution of improvement along with higher price points. Many in the industry have pointed to 5G technology as the next step change in smartphones. A 5G phone from Apple is seen as a key driver for adoption, but that may be released in September or 2021. There are debates over download speeds, carrier price points, carrier coverage areas, and penetration levels outside dense cities, but 5G carries the hope and excitement for the consumer electronics industry. Early 5G adoption will be critical for Best Buy and the industry as consumers may put off purchasing a replacement depending on early reviews. As Best Buy’s other product segments decline or peak it will be increasingly reliant on 5G spurring a new replacement cycle for growth.

Gaming cycle

The gaming cycle is currently cyclically weak for brick and mortar retailers, but it is structurally weak as well. For Best Buy the entertainment category, of which gaming is a major component, represents 8% of sales. GameStop reported comparable sales declined 25% in the Nov.-Dec. period. GameStop said results during the holiday period were indicative of the overall industry trends. With the next generation consoles expected to be launched in the holiday season of 2020 it should turn into a positive for holiday 2020. The initial year of a console launch is a big basket benefit. Sony and Microsoft have both announced that their next generation consoles will be backwards compatible so games purchased on the current generation will still be playable. Video games over a longer time frame are likely to be a headwind as consumers purchase fewer titles and instead increase the playing time of a single game through in-game purchases and extra maps that are transacted around the retailers and through the platforms directly. Fewer customers are even purchasing physical copies of their new games and digitally downloading the games instead. Video game publishers capture more of the sales dollars by selling directly. Without physical copies to sell back to GameStop the used game market has seen a significant drop in supply. In the very long term it is likely that the console itself is avoided and all games are streamed. The most popular game since it’s launch in 2017 is Fortnite. Fornite is free to download on a number of platforms. Yet it is the industry’s highest earning game through the sale of in-game transactions. This has caused the video game publishers to change their strategies for new game launches and revenue sources in ways that are all negative for brick and mortar retailers.

DVD and music sales are in secular decline

DVD and CD sales are the next biggest components of Best Buy’s entertainment category. DVD sales have declined 86% since 2008. With the launch of Disney+ DVD sales are likely to continue to decline, but are much less important for Best Buy due to the small percentage of sales it currently represents. CD sales have fallen to a fraction of the total music industry revenues as seen in the industry chart from The Economist below. Best Buy does not appear to have a traffic driver to the stores like new DVD and CD releases once were.

TV cycle needs a technology catalyst

The second most important cycle for Best Buy is the TV cycle due to the high ticket and central role it plays in the household’s electronics. The Consumer Electronics segment represents a third of total sales. In early December Conn’s reported that its consumer electronics category comped down 25.6% in Q3 as the ASP for TVs declined 8%. The ASP for large TVs over 65 inches declined 22%. The decline in TV prices can be a sales driver for Best Buy in the short term, but too much deflation brings heightened competitive activity. Televisions have experienced price deflation every year since 1981. The average deflation rate since 1981 has been -10.5% according to US Bureau of Labor Statistics. In just the past ten years prices have fallen an average of 16% each year so that a $3,000 TV in 2010 would cost $527 now. The average replacement cycle of a TV is seven to eight years according to Best Buy. With the size of the screens being so large for a number of years a new technology making older TVs obsolete is needed to spur a shorter replacement cycle. The TV industry hoped 4K or 8K would be the future, but the technology has mostly exceeded the industry’s ability to utilize the capabilities due to additional streaming, programming and device upgrades necessary to see the difference.

Appliances have been a success courtesy of Sears

Appliances have been a growing category for Best Buy since 2000 and now represent 10% of domestic sales. Best Buy has been a beneficiary of the hemorrhaging of market share by Sears. In 2017 alone Sears and the exit of hhgregg shed $1.9bn of appliance sales which went primarily to Home Depot, Lowe’s and Best Buy. According to the Wall Street Journal Sears has lost about half its market share in appliances in the past three years as seen in the chart below.

In Oct. 2018 Sears declared bankruptcy. In Feb. 2019 Sears emerged from bankruptcy with 400+ Sears and Kmart stores down from 1,000. Since then the company has closed some 35 Kmarts and some 20 Sears stores in 2019. In November the company said it would close an additional 51 Sears stores and 45 Kmart locations in February 2020 leaving it with a combined 182 stores. The steady market share lost by Sears accelerated dramatically in 2019 which likely represents the peak for its competitors.

Coronavirus will impact supply chains

China is critical in the global electronics industry. Apple said this week that inventory levels of existing products may last until April or longer. Other similar announcements should be expected to be forthcoming in the near future.

Competitive environment likely won’t have tailwinds

Best Buy has done an admirable job adjusting to e-commerce competitors, namely Amazon. The idea that the “showrooming” term was at first seen as synonymous with Best Buy shows how far the chain has come. Best Buy hasn’t had any national consumer electronics competitors in several years. Smaller regional or local brick and mortar competitors have relied more on services to stay relevant or close. Amazon will always be a price competitor limiting Best Buy’s pricing flexibility. Best Buy has lost the shoppers who actively compare prices at least where it isn’t competitive on price a long time ago. Best Buy has succeeded by servicing customers who need to see the merchandise and prefer the interaction with a salesperson. These customers tend to be less comfortable with new technologies and skew older. Best Buy survived the first competitive push from Amazon, but it is difficult to see the competitive environment actually improve.

It’s still a pressured sales culture

Circuit City ended commissions for salespeople in 2003 to match Best Buy. Customers preferred employees in the store to be less “pushy.” Circuit City went bankrupt in 2008 and its inability to retain knowledgeable salespeople without commissions was a contributing factor. Even though Best Buy does not pay sales commissions, it is as close as you can get when you factor in hourly revenue goals, attachment goals and revenue per transaction targets. Revenue generated can also impact the number of hours the employee gets as well. E-commerce is much less “pushy” and Circuit City’s warning remains.

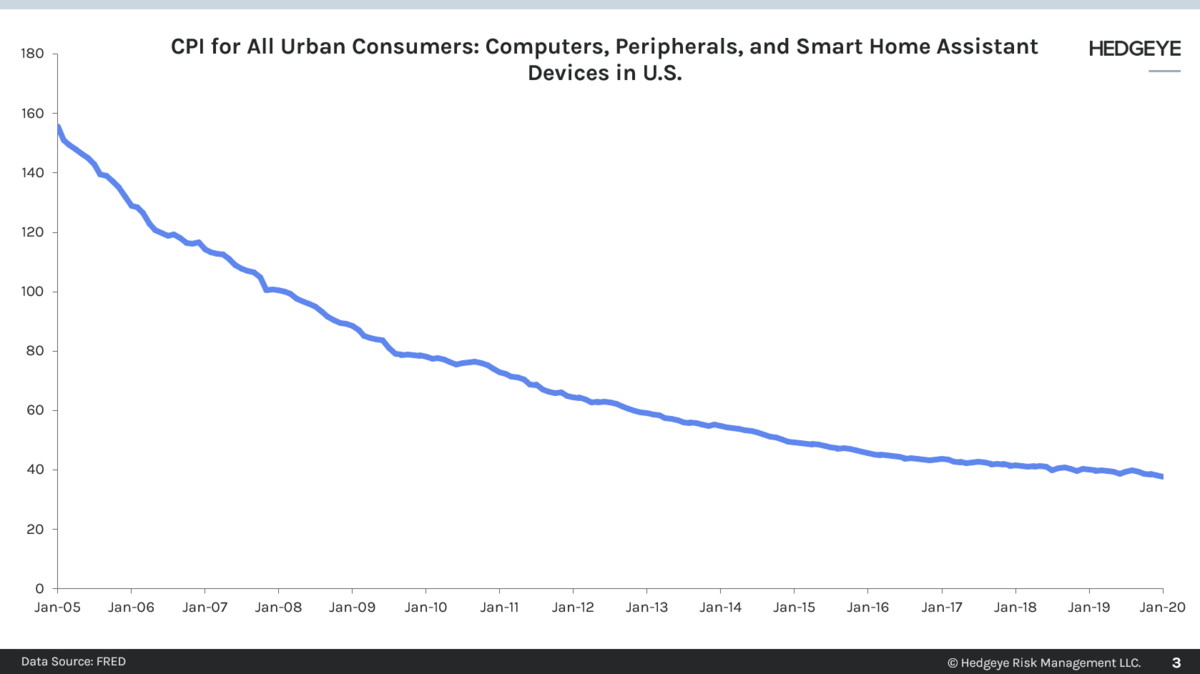

Warranty sales drop when the transaction is online

The sale of extended warranties is a significant profit driver for Best Buy. Due to the high ticket and perceived difficulty fixing the product among other factors consumer electronics has a high attachment rate for warranty sales. Warranty sales are very profitable. The attachment rate for consumer electronics warranty sales is about one-quarter of all purchases based on data from INFORMS Society of Marketing Science Durables which used 140,000 product purchases at a major US electronics retailer’s 1,176 stores between 1998 and 2004. Dated, but still likely in the ballpark. Unlike the purchasing decision to come into the store, the decision to purchase an extended warranty very often involves little price comparison shopping. The price of an extended warranty is roughly one-quarter of the retail price. Due to the low failure rate of electronics the profitability before sales commissions is estimated to be roughly 70% of the price of the warranty. Best Buy records the sale of the warranty net of a third-party underwriter as revenue with no associated costs. Best Buy also receives a profit-sharing payment depending on the performance. In F2019 Best Buy received $7mm in profit sharing down from $59mm in F2018 and $110mm in F2017. Because the profit-sharing premium has declined so significantly in the previous two years we are under the presumption that the rates have been negotiated over time such that Best Buy receives more revenue with the original sale than in the profit sharing. There are two structural headwinds to Best Buy’s warranty sales. Warranty attachment rates are correlated to the price of the item. Clearly human psychology plays a role in the consumer’s decision making and risk aversion. The ongoing price deflation in consumer electronics as seen in the CPI chart below makes warranty sales more challenging.

The larger headwind is Best Buy’s growing sales mix in online purchases (16.6% in F2019 vs. 15.5% in F2018). The much lower attachment rate of warranties online is an under-reported negative of e-commerce sales. According to “The Effect of Product Misperception on Economic Outcomes: Evidence from the Extended Warranty Market” written by Jose Abito and Yuval Salant the online attachment rate is 1/7th of the in-store rate (4% compared to 24% in-store). Best Buy has not been able to find a selling proposition online to match the in-store sales associate.

Few acquisitions have created value

Best Buy has a very checkered history in acquisitions and new initiatives. We don’t blame a company for trying, but it’s important to keep in mind the history when ascribing value to future acquisitions/initiatives like the current healthcare push. Appliances and services are the exception in expanding new major categories for Best Buy. Carphone Warehouse’s $2.1bn, European store expansion, Five Star’s $180mm, Musicland’s $425mm, Napster’s $121mm, and CinemaNow are some of the notable busts in Best Buy’s history of failed investments. The Geek Squad and Pacific Sales acquisitions in 2002 and 2006 stand out in Best Buy’s M&A track record. Best Buy does continue to operate Magnolia for which it only paid $87mm, but it also closed all of the stores and moved them into some Best Buy stores. Also Pacific Sales stores have only grown by seven since it was acquired 14 years ago and Services of which the Geek Squad is part of only represents 5% of sales. Best Buy anniversaried the GreatCall acquisition in Q4 which was accretive to gross margins all year. The $800mm acquisition matches the portion of Best Buy’s customer base that needs the most in-person assistance and their aging needs for emergency help. GreatCall’s flip phone appears to be vulnerable to disruption, but the leading consumer electronics retailer should be well positioned to see technology disruptors ahead.

Recent trends are mixed

Target said the electronics category was down more than 6% over the November and December holiday period. Walmart cited strength in electronics in Q4 and weakness in media and gaming. Consumer electronics store sales as reported by the Census department have been downtrending. November was down 3.2%, December was down 1.1% and January was down 3.2%.

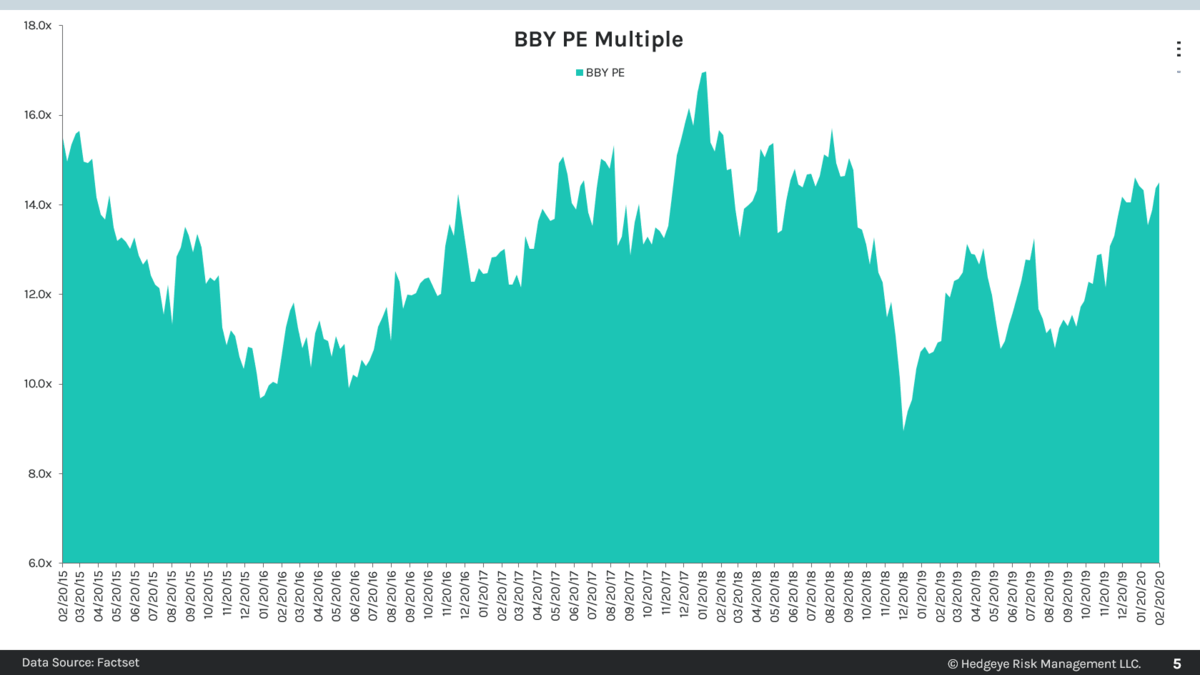

Valuation is at the higher end of its range

Best Buy shares are trading at 14.5x NTM consensus EPS estimates, which is at the high end of the range over the past five years.

Best Buy has not missed consensus EPS estimates in several years, because management is adept and revising guidance. However, the share price has fallen on the day of earnings six out of the last ten quarters by at least 3%. We are not modeling an EPS miss in Q4 – which is holding us back from making the call ahead of the quarter. But keep in mind that management raised EPS guidance for the year to $5.81-5.91 on the Q3 report and consensus is above guidance at $5.93.