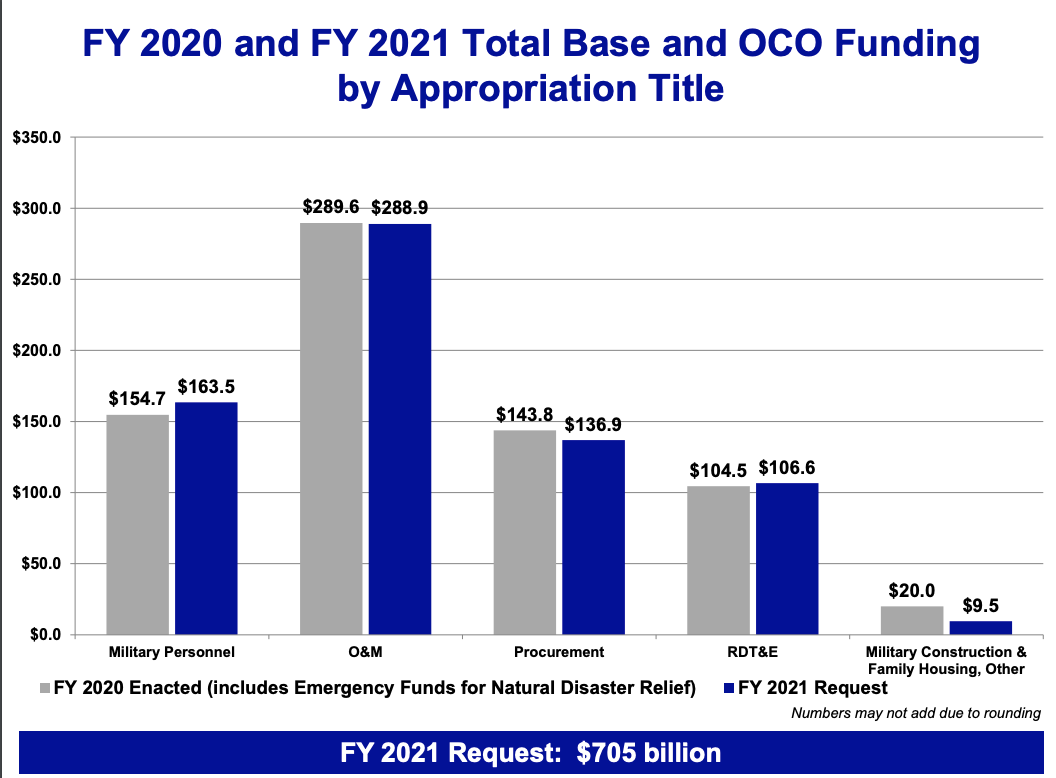

On Monday the White House submitted a request for $740.5B in FY 2021 Defense spending, $705.4 for the Pentagon and $35.1B for the Department of Energy and other agencies which support nuclear activities. The Pentagon request includes $636.4B in baseline spending and $69B in Overseas Contingency Operations (OCO) spending, $16B of which is going to fund baseline requirements.

There are no surprises in the size of the topline request. The proposed $705.4B Pentagon spending is less than 0.1 percent higher than the $704.6B appropriation enacted by Congress for FY 2020 and matches the ceiling agreed with Congress last fall in the two year budget deal for FY 2020 and 2021. (This is not the case for non-defense discretionary spending which is $25B (-4.4%) less than the agreed non-defense ceiling. "Its a ceiling not a floor," said OMB.)

There are some significant changes within the budget driven by the Pentagon's continued drive to meet the requirements identified in the 2017 National Defense Strategy needed to compete with China and Russia in the high technology battlespace. Creation of the US Space Force has resulted in the realignment of ~$15B to the new service. The R&D budget has been increased by $2.1B (+2%) over the 2020 enacted level to $106.6B, the largest RDT&E request ever. Also a factor in the changes is the need to cover inflation and higher costs in Military Personnel and Operations and Maintenance within the flat topline. The net bill payer for all of this is Procurement which is proposed to be down $6.9B (-4.7%) from 2020 levels to a still robust $136.9B.

Surprise Factor. In the following section we identify major programs by prime contractor which have significant differences in the FY 2021 request from what was forecasted for FY 2021 in the PresBud request for FY 2020. These "surprises" are likely to create the most unplanned perturbations in prime contractors' calculations of backlog and future revenue and will be their main lobbying objectives in the coming legislative year.

Lockheed (LMT)

F35. 79 aircraft requested for 2021, 2 more than requested in 2020 but 19 less than appropriated by Congress in 2020. This is net two less aircraft than forecasted for 2021 (5 less F35Bs, 3 more F35Cs) or -$368M. Expect Congress to find a way to add aircraft as they have for the past several years.

CH53K. The Marine heavy lift helo program has been significantly slowed in the FY 2021 request. Only 7 aircraft vice the planned 12 have been requested in FY 2021 at a loss of $652M in budget authority. There is a total reduction of 20 aircraft and over $2.2B over the next four years.

Hypersonics Prototyping. The Air Force has cancelled the contract to develop the Hypersonic Conventional Strike Weapon (HCSW), one of the two hypersonic missile prototype contracts it had with LMT. The remaining contract for the Air Launched Rapid Response Weapon (ARRW) remains robustly funded but total USAF funding requested for hypersonics prototyping in FY 2021 is only $382M vs. $586M enacted in FY 2020.

Boeing (BA)

F/A-18E/F. 24 aircraft for $1.8B are requested in FY 2021 as forecasted. The big change is that there are no further procurements of the Navy stalwart planned after 2021. This is a change from the forecasted 12 per year through the end of the FYDP and is a reduction of $3.6B in budget authority over the next four years.

F-15EX. Cost realism has taken hold as planned gross unit cost has increased from the PB 2020 forecast of $91M to $106M per copy. 12 aircraft for $1.4B are requested in FY 2021, 6 less aircraft and $250M less budget authority in that year. Over the next four years (2021-24) the Air Force will procure 15 less aircraft resulting in $340M less budget authority.

Shipbuilding (GD/HII). Despite Navy promises to publish a shipbuilding plan in the next few weeks that will increase the fleet size by 20% in the next 10 years, the FY 2021 shipbuilding budget only starts construction of 8 ships vs. the 10 forecasted in 2020 to be built in 2021. Increased costs of Colombia and the next nuclear carrier and the unplanned but Congressionally-mandated overhaul and refueling of Nimitz have eaten into new ship construction.

DDG-51. Significant reduction in quantities across the FYDP compared to the FY 2020 forecast. As forecasted two ships are requested in both FY21 and FY22. However, the six ships forecasted to be procured in FY 23 and FY24 has been cut to three. Budget authority for the period FY21 to FY24 has been reduced to $13.1B, $6B less than forecasted in 2020. Impacts GD and HII equally.

TAO Fleet Oiler. Built by GD NASSCO. The Navy forecasted procurement of an oiler in both FY 2021 and FY 2020 @ $515M has been zeroed out with procurement to resume in 2023. There is a $900M reduction in budget authority over those two years compared to the 2020 forecast.

Textron (TXT)

Ship to Shore Connector. The program remains troubled and is being further truncated. The 2020 forecast was to buy 4 of the air cushion vehicles for $274M in FY21. The 2021 request zeroes the program in 2021 and reduces the planned buy over the next four years (2021-24) from 21 to 9 with a loss of $800M in budget authority and potential revenue for TXT.