Below is a complimentary research note from Communications analyst Andrew Freedman. If you are an institutional investor interested in accessing our research email sales@hedgeye.com.

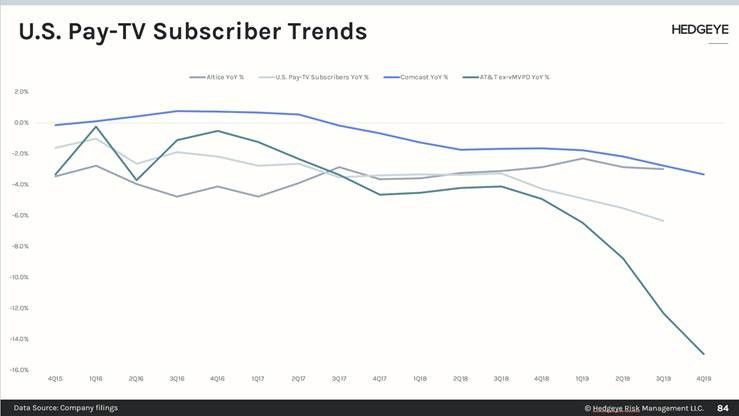

Altice (Short) was down ~4% today on sympathy to AT&T/T (Short Bench) 4Q earnings results that showed deteriorating trends in Pay-TV and broadband customers. Following CMCSA earnings and guidance last week, our expectation for 2020 Pay-TV losses to be greater than 2019 is pretty much confirmed.

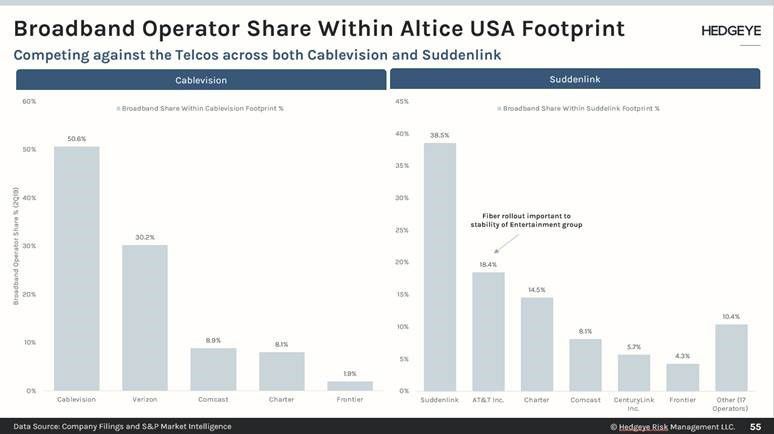

For Altice (ATUS), we expect Pay-TV declines to accelerate through the 1H20 and also weigh on broadband subs (see charts below). With 60-65% of the Optimum footprint bundled with video/broadband/phone, a cord-cutting decision increases the probability of an outright customer loss. The risk is higher in markets where they compete with Verizon (VZ), who recently began offering Fios internet and video unbundled w/no contracts.

Meanwhile, Altice is trying to pass through the largest Optimum price increase in years effective 2/1. With Verizon seemingly getting more competitive, it is a bold move in our view, and will be interesting to see how it works out for them.

VZ reports tomorrow morning, and we will be looking for an additional read for ATUS.