CLICK HERE to access the associated slides.

Our mission at Hedgeye is simple: Get “The Cycle” right, so that our investing subscribers can proactively position their portfolios for high probability outcomes which will drive financial market returns over the next six months.

The unique risk management process our research team has developed measures and maps everything that ticks in global Macro. We humbly submit that our granular and rigorous investing process will help you be more often right than wrong.

Remember, the current stagflationary economic environment we’re forecasting has helped investors navigate the big investable breakouts (and breakdowns) in financial markets, even as financial pundits and so-called experts purvey fear of World War III.

That’s why Hedgeye CEO Keith McCullough and Senior Macro analyst Darius Dale hosted a complimentary edition of The Macro Show this week. We want investors to tune out the incessant noise and nonsense and get properly positioned for the market environment to come.

Here’s a key quote from Keith:

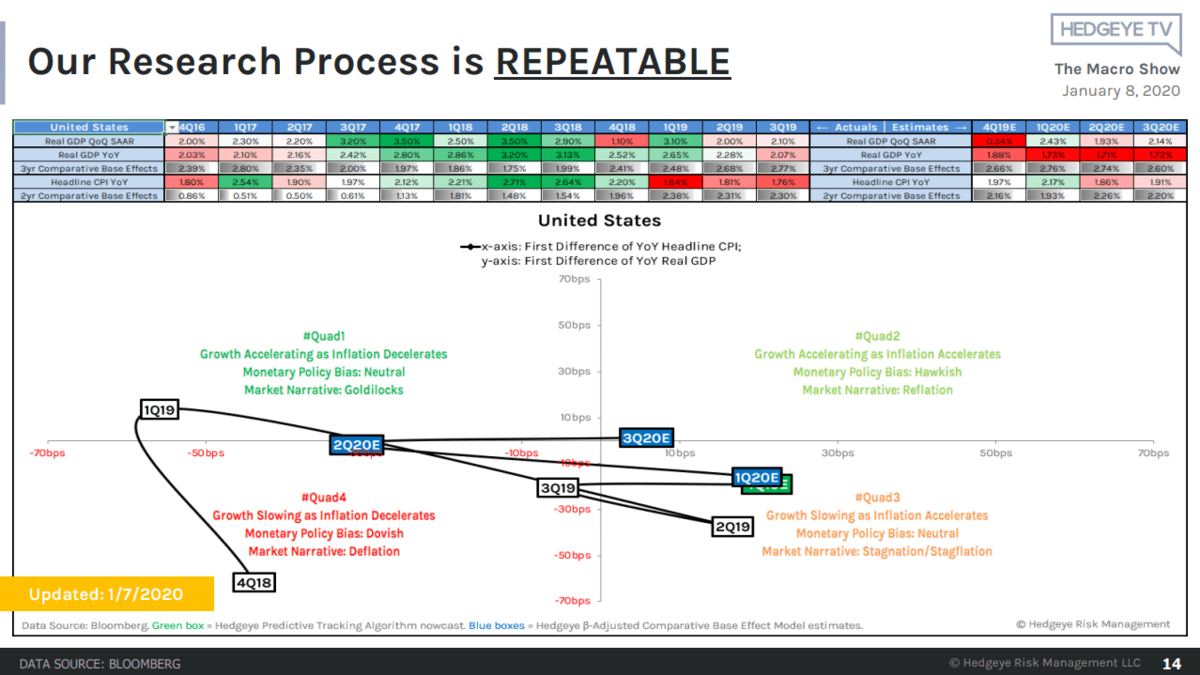

“That’s what our Quad model is capturing too when we say we’re in a Quad 3 environment. Quad 3 is stagflation. The U.S. Dollar breaks down in Quad 3 as the market sniffs out deteriorating economic data and front-runs the probable outcome of the Fed going dovish.”

Once you dig into the Macro mosaic implied by Quad 3, the fog of market uncertainty clears and the investing implications are manifest.

Below are key excerpts transcribed from this complimentary edition of The Macro Show. Watch this entire episode of The Macro Show above.

* * * *

Darius Dale: Good morning everyone. I’m Senior Macro analyst Darius Dale and welcome to this complimentary edition of The Macro Show. Enter your questions and we’ll get to as many as we can before the end of the webcast. I’m going to turn it over to Hedgeye CEO Keith McCullough.

Keith McCullough: Thank you Darius. First things first, I’m going to do what I do every morning and that’s the top things in my Macro notebook.

The Russell 2000 is down for the year-to-date. How about all those people talking about the year-to-date? For the year-to-date the Russell down. How about The Cycle to-date? For The Cycle to-date it’s down.

The Russell is down -4.7% from where we got you out of Small Caps at the end of the third quarter 2018. Don’t forget you sell Small Caps when you’re in Quad 3 or Quad 4. When we hit Quad 4 in Q4 of 2018, Small Caps crashed. Some people may forget that and then they talk about the 2019 year-to-date off that crashed out low. Of course, all of those people sold it at the 3Q18 peak then bought it back at the bottom.

Dale: Nope.

McCullough: That’s just people bloviating on TV. You can get that insight for free. I digress.

Small Caps only work when you’re in Quad 1 and Quad 2. We were long Small Caps coming out of 2016 until Q3 of 2018. Now we’re in Quad 3. So short the Russell on rallies to the top end of the Risk Range.

McCullough: I want to talk about the VIX. The Macro Tourists are freaking out about World War III on CNBC. I have no idea why you watch that. It’s a waste of your time. Your time in life is precious. Spend it according.

The volatility of Volatility – if you don’t know what that is you’re going to learn something here – that is the leading indicator of the surface area of price. The vol of Vol says, ‘I’m not concerned about World War III.’ And that’s why we have more longs than we have shorts in Real-Time Alerts.

Unless Volatility can break out on a trending basis – or the vol of vol rises – why would you short the S&P 500? Instead you buy the four sectors that are longs in Quad 3. That’s Tech (XLK), Utilities (XLU), REITs (VNQ) and Energy (XLE) stocks. Those are the top four sector overweights, particularly on pullbacks.

Buy what works in the economic regime you’re in (i.e. Quad 3). In addition to that you want to be long Commodities or Russian stocks.

There are plenty of things to be long in Quad 3.

And, against your longs, you can short what doesn’t work in Quad 3. So your longs can be balanced by your short U.S. Dollar position. Short Transports (IYT). Short Industrials (XLI).

But getting back to vol, and this is an important risk management reminder, the low-end of the risk range for the VIX implies a higher low so be careful with your longs as the VIX approaches 12.01.

Just to simplify the complex. You sell the top end of the range and buy or cover at the low end of the range.

And here’s another really important point. Look at the implied volatility of the S&P 500. Now, a lot of you if you’re new to what we do have no idea what I’m talking about. This is an eye-opening thing. The implied volatility premium yesterday in the S&P 500 was 49%. What that means, at its most basic level, is that everyone has already bought protection.

Basically, implied volatility is the market’s future expectations of volatility that’s implied by the futures and options market. Realized volatility is actual historical volatility of that asset. So when implied volatility is at a premium to realized volatility, particularly a high and rising premium, that means investors are getting more fearful and buying protection. Conversely, an implied volatility discount implied complacency and capitulation.

So, at a 49% premium on the S&P 500, you don’t want to be buying protection when everyone else has already bought it. What you want to do is buy protection when everybody has absolutely capitulated on their shorts and is super complacent about their longs. If that were the case you’d see an implied volatility discount versus 30-day realized volatility.

McCullough: Here’s a chart for you. Look at Russia (RSX). Did you buy Russia when you should’ve bought Russia in October at every higher low? That’s what you should be doing. Understand that Russia, unlike China and the U.S. was in the right Quadrant.

Again, if you look at slide 20, we can show you our GIP model for G20 countries. This is about awareness. We can show you every single country in the G20. What Quadrant they’ve been in, which is an economic fact, and what we have them mapping towards.

So roll down that list to Russia and you can see Russia has been in the right Quad. It’s in Quad 2.

So you buy the equity markets that are in Quad 1 and 2 versus the markets that are in Quad 3 and 4.

We update this every single day. And that’s what you need to be looking at. If you get up and don’t have a process you’re just flailing around like a Macro Tourist.

McCullough: Now why else do we like Russia, Energy stocks and Commodities? The answer is the inverse correlation between anything in the Commodities space and the U.S. Dollar. The Machine really likes that one. What the Machine is doing is front-running the Fed going dovish as U.S. economic data continues to deteriorate.

And that’s what our Quad model is capturing too when we say we’re in a Quad 3 environment. Quad 3 is stagflation. The U.S. Dollar breaks down in Quad 3 as the market sniffs out deteriorating economic data and front-runs the probable outcome of the Fed going dovish.

Are you feeling smarter now? There’s a 77% inverse correlation between Commodities and the Dollar on a 30-day basis. The U.S. Dollar is down -2.2% from its Q3 2019 peak. The Dollar nailed the Quad 3 transition and broke down right on schedule. When you look at this through the Quad 3 lens its no surprise the Dollar is falling and Commodities are breaking out.

So that’s another thing that’s driving my Risk Range signal to a stay long. It’s also why I’m going to be buying every damn dip in Energy until I damn well please because my Risk Range signal is bullish and the Risk Ranges front-run the Quads.

Remember, it’s an A/B test. The “A” part of our Risk Management A/B test is our four Quadrant Growth, Inflation, Policy (GIP) model. The “B” part is my Risk Ranges, which measure the price, volume and volatility of anything that ticks in global macro. When both of these signals align, my Risk Ranges and our GIP model, we’re all in.

Dale: And on the Quads, what we’re doing there is looking at all of the historical iterations of Quad 3 in market history and telling you what’s likely to work and what’s not likely to work. What our Quads show you is that you want to be long Energy (XLE) in Quad 3.