This Hedgeye Guest Contributor piece was written yesterday by Tim Boyd of Delphi Capital.

What a long, strange trip it's been to this place where equities no longer carry risk! Sardonicism aside, we've been fortunate enough to have the good sense to not stand in the way of this creeping glacier the major central banks have created. We use the term "glacier" because the S&P 500's latest rally to new all-time highs has felt as plodding as it has unstoppable. We know better than to argue with the market, but we would be remiss if we didn't express our extreme concern at the moral hazard that has manifested.

Investors are no longer cowed by anything: not by deteriorating global macroeconomic conditions, ongoing trade skirmishes, unprecedented domestic political drama, or extreme valuations (on a total market cap to GDP basis in particular).

Why? Because the majority of them believe the one-two punch of Trump and the Fed will absolutely forbid a meaningful correction in risk assets. In light of the fact that the Fed didn't even hesitate to initiate quantitative easing measures in the overnight repo market (we don't care what Mr. Powell says - it's 100% quantitative easing), such a belief bears credence.

It appears that liquidity is and will continue to be forced down the throat of the global financial system, and in the post-2008 world liquidity trumps fundamentals. Woe to those who refuse to accept this sordid but undeniable new world order.

We'd like to share three charts that have our attention this morning:

1) EEM (iShares Emerging Markets ETF) has broken out of a multi-year pennant formation and is a good bet to retest its all-time highs before the end of the year. While this technical event is indicative of rising risk appetites, we think there is also another force at work here, namely investors' working assumption that as long as the Fed/ECB/BoJ are prepared to dump cash out of helicopters, emerging market equities carry significantly less risk than normal. Add to this the fact that EM valuations remain at very low levels relative to those stateside and it seems reasonable to expect a steady rotation out of the U.S. and into Brazil, Russia, India, China, the Asian Tigers, Mexico, South Africa and other markets that are generally viewed as not quite meriting the moniker "developed" (although we must admit we think it's rather silly that China is still included in that group).

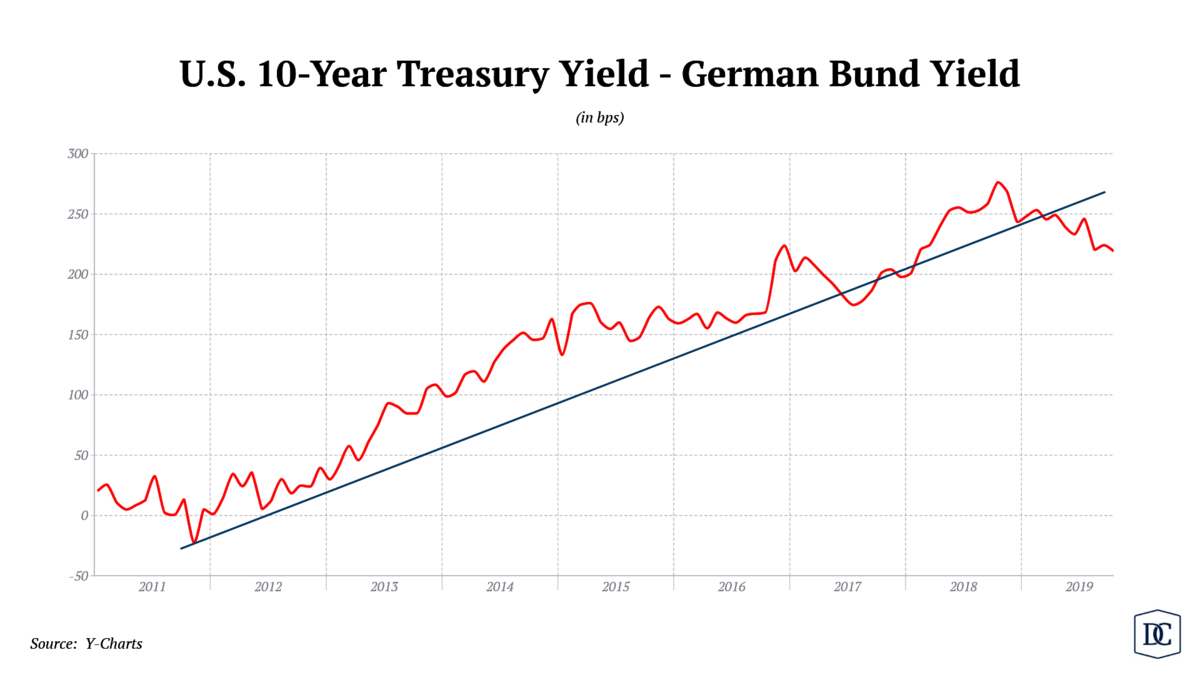

2) The second derivative of the U.S.'s yield advantage over Europe is rolling over. We've traded interbank currency markets for nearly 20 years and can state without hesitation that the single most important driver of developed-market exchange rates is the rate of change in yield differentials. In that vein, we note that hatred of the Euro has been deep and widespread since the German Bund dipped into negative rate territory. The fact that the ECB would love to see EUR/USD trade below parity adds to the single currency's miasma. Problem is, the market has not gone all-in on the Dollar: looking at a chart of EUR/USD it's plain to see that the downtrend which took hold in early 2018 has had a very "reluctant" look to it. In our view this is due to two things:

a) The long-term structural fundamentals of the USD remain horrid, particularly our massive twin deficits (budget and current account).

b) The growing suspicion that the Fed will have no choice but to follow the ECB down the NIRP rabbit hole. Eventually.

We have been EUR bears since the day the single currency went live. We believe the concept was deeply flawed and all but doomed from the start. That has served us well at times against commodity currencies (e.g. Australian Dollar, Canadian Dollar) and the Japanese Yen, but it has been painful bet most of the time against the USD. For the first time ever, we are now bullish on EUR/USD for the simple reason that we are more bearish on the USD than any other developed-market currency. The USD's yield advantage over the EUR exploded higher in 2012 as it became abundantly evident that Europe was in much deeper socioeconomic "excrement" than the U.S.; over that time period the ECB acted aggressively while the Fed seemed to always be looking for the QE exits. The governors' dream of rate normalization was crushed last December when it became clear that the U.S. economy couldn't even handle a 10-year yield over 3% (which is scary in its own right, but that's a story for another day) and it is now quite clear (to us at least) that the Fed is well-behind the curve.

The below chart of the yield differential between Germany and the U.S. provides a visual confirmation of our suspicion regarding the Fed: Powell & Co. will likely be compelled to accelerate their stimulating activities over the next 12 months, and this strongly suggests that the USD's uptrend vs. the EUR is at an end. One tie-on to our observations on EEM: given that emerging markets thrive when the USD is weak, a breakdown in the greenback could end up being a catalyst for overall risk sentiment as well.

3) Silver prices have broken topside after a multi-month consolidation phase. We have been precious metals bulls since last August but we are souring on gold in the near term for two reasons:

a) We are concerned there will be a sharp decline if any more progress is made on the Sino-American trade detente. Much of gold's run since last fall has been attributed to a flight-to-quality in the face of a tempestuous trade spat, and when Mr. Trump drops his tariffs for very little in exchange (which we are convinced he will do to boost his reelection chances) it's probably a safe bet that the resulting selloff in the Dollar won't help gold very much.

b) The gold/silver ratio has turned sharply in the latter's favor of late and in light of silver's widespread industrial use

and tightening supply it should hold up rather well after the "Yugest Bean Deal Ever" is officially codified. Technically, the ratio can fall all the way to 71 (it's 84 as we write this) before its 8-year uptrend is even modestly threatened.

Combining these two factors with the bullish technical outlook for SLV (iShares Silver ETF) yields what we view as an outstanding risk/reward opportunity. We believe spot silver prices can reach $21 before resistance stiffens, which implies 17% upside from current levels. With central banks around the globe playing "Who Can Debase Their Currency More?" - and with that unlikely to change for the foreseeable future - we think there's a good chance silver tests its 2011 highs near

$50 within the next 3 years. If anyone knows where we can find 17% short-term upside and 180% medium-term upside in the equity markets, please let us know - but color us skeptical given the frothy heights stocks have reached in 2019.

There is indeed a catch, however. Well, two catches to be exact: silver is not only extremely volatile (an issue that can be addressed by reducing one's leverage) but highly susceptible to manipulation (as the recent charges against J.P. Morgan reminded us). Bullion banks are frequent practitioners of what we refer to as the "Paper Crush", in which the banks dump billions in paper gold and silver (i.e. futures contracts) on the market with zero regard for execution costs. In other words, they don't "work" their orders.

They simply slam every bid on the board - even if it results in 100+ basis points of slippage. We suspect that they do this with the blessing of central banks, in whose interest it is to prevent a parabolic rise in gold and silver prices (which could theoretically destabilize one or more fiat currencies). The gold bugs at GATA are much better versed on that topic and we encourage all would-be precious metals investors to read the material on their website (www.gata.org) regarding central bank meddling.

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Tim Boyd of Delphi Capital. This piece does not necessarily reflect the opinion of Hedgeye.