This new conversation between renowned investor Kyle Bass and Hedgeye CEO Keith McCullough is one of our most-watched interviews ever.

Keith and Kyle discuss China’s rising importance on the global economic stage, its massive leverage problems and deeply troubling Chinese social issues that we should all care about as freedom-loving Americans.

This conversation is a must-watch about one of the most important issues in finance right now. We’ve transcribed some key takeaways from this important interview below.

Click here to watch this entire interview free.

* * * *

Keith McCullough: Hi I’m Keith McCullough. Welcome back to the Hedgeye Investing Summit. We’re ending our summit with anchorman, Kyle Bass. We’re going to talk about one of the most important topics to anybody who's invested in global macro markets, and that’s China. So thank you for making the time to join us today Kyle.

I always enjoy having a conversation with you. We just spent some time together in Texas.

Before we begin I want to contextualize where we’re coming from and then hand it over to you.

When you think about China you’d start with the 2015-2016 stimulus in China. It wasn't a fake stimulus. It was the biggest stimulus in the history of China fiscally and monetarily. That massive push bled into Chinese GDP. Our call had been that the Chinese economy would slow in Q1 2018. That’s indeed what happened. The real question on China, at this stage, is whether the cycle slowing continues from here or whether this is a long-term secular slowdown.

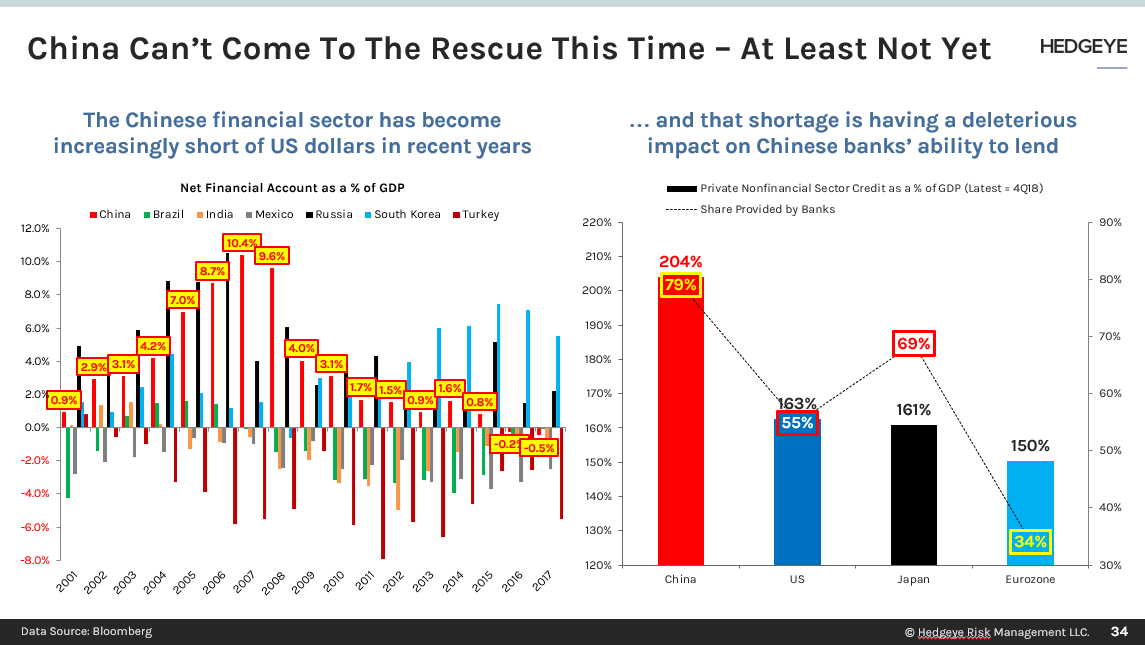

Obviously Chinese reserves have collapsed. The dollar being up has been a big problem for China because they're funding a lot of their issues in U.S. dollar denominated debt.

Kyle is obviously the first person to call this out, way early and right on the screws, which is that China is moving from a current account surplus to a developing current account deficit. And they have to fund their deficit in dollars.

So that’s the question I have for you Kyle. Do we have a secular problem that's just readily apparent on the screen?

Kyle Bass: You make a bunch of great points there, Keith. I think it's important to focus on the fact that when in China's ascendancy, call it post 2001, they were growing much faster than anyone else in the world. Right. And what they were doing is taking growth from their other Asian neighbors. What you're seeing now is the law of large numbers catching up to China where they're going from eight percent growth to seven to six to five all the way down to two or three percent growth.

If you look at the actual numbers, we think they're growing at about 2.5% last year and maybe somewhere between zero and two this year. And I think it's important to note that China won't be able to grow faster than the rest of the world from here now that things on the labor side of equalized. That has a lot to do with their current account. And you showed that other chart of China's dollar shortage, which we focused on.

We think about China in two different ways. One is domestically they control the printing press, they control the price level, the police, the narrative. How many times Keith, have you been sitting with someone and they say, ‘But it's China. They can kind of do whatever they want to do.’ And I say that's true domestically to a certain extent.

The real issue in China is they still have to interact with the rest of the world. And as they interact with the rest of the world, they have to buy crude oil. They are short of crude, short energy, they're short food, and basic materials, right? They have to buy these things to keep their GDP growing internally. They still have to continue to purchase things with their dollar balances or their FX balances. We think that current account deficit is secularly going to be negative from now on.

This is where the rubber meets the road, about whether this secular trend is meeting a cyclical down trend. The secular problem is they're running out of dollars. As soon as the world figures that out and the U.S. intelligence and presidential cabinet figures out that they're running out of dollars, they realize that in these trade negotiations, the U.S. holds all the cards.

McCullough: On trade negotiations, do you think that that 12/15 date for trade tariffs is critical? If we're not to implement those tariffs would that change the secular path of Chinese growth slowing?

Bass: I just think that it will prevent the trajectory from not getting worse. I don't think pushing back that potential tariff date is going to make anything incrementally better.

Tariffs are a very blunt force instrument that Trump likes to use. But I think you're going to see DOJ start using the FCPA, the Foreign Corrupt Practices Act, and they'll use that like a scalpel. They'll start cutting companies out of the U.S. that are endemically corrupt.

McCullough: I know you have a lot of respect for Brigadier General Robert Spalding's recent book, Stealth War. It kind of blows your mind that these things have been happening and they are documented. And everybody knows it.

Bass: Well, I wouldn't say everybody already knows that. I spent a week in DC meeting with people that focus on China. When I brought up the fact that Chinese companies that list in the U.S. don't actually have to adhere to the same standards as U.S. listed companies they looked at me like I had three eyeballs on my forehead. Many of them were Congressmen and Senators. So there are many things out there that people just aren't aware of.

I know this sounds crazy, but maybe we should require foreign companies to adhere to the same standards as U.S. companies when they raised money in the U.S.

McCullough: I think this is a major problem with Wall Street. I certainly aspire to create a level of awareness. So I want to do that on Hong Kong because I think you've done some great work on that.

Bass: Let me make one comment on that and then we'll go into Hong Kong. I think we all look at incentive structures. You saw this with the NBA. Their incentive structure was money over morals, right? Or money over freedom of speech.

You mentioned Wall Street. The incentive structure of Wall Street is to embrace China and hope that more M&A happens that more IPOs happened because they just see fees. China dangles that golden carrot out in front of any Wall Street firm that to chase it.

But let's talk about Hong Kong.

Hong Kong used to be a quarter of China's GDP in the early nineties, and now it's back down to about 2.5%. Strategically, it's really important from the perspective of geopolitics. Financially it's important from another angle. This is where China raises all of its dollars. The majority of its dollars go through Hong Kong.

When you look at private sector credit to GDP, Hong Kong's the most levered nation in the world. Taking five or 10 steps back to understand what just happened, Hong Kong has been pegged to the U.S. dollar and therefore is imported U.S. monetary policy for 36 years.

And that import requires them to basically, let Jesus take the wheel and import the monetary policy of the U.S. So what happened going into the financial crisis is we dropped our rates from 5% to zero. Hong Kong came along with us. At the same time, China hit the gas pedal. So we've seen Hong Kong's real estate market explode.

So from 2008 to 2018, it was the best 10 year period Hong Kong will ever see in its entire existence. It will never happen again. In 2008, when money became free, private sector credit to GDP of 300%. So Hong Kong's the most levered developed nation in the world.

You look at page six, Hong Kong's banking sector is now 850% of GDP. You remember back when Europe had their issues in 2011? Iceland, Ireland, Cyprus all fell like dominoes because their banking sectors got to be eight, nine, 10 times GDP. In that scenario, if you lose three to 5% of your assets, it literally bankrupts your entire sovereign.

Bass: And so what's happening in Hong Kong now is you've got enormous amounts of leverage and you've got enormous amounts of banking assets.

Once Hong Kong runs out of excess reserves, they're going to have a liquidity issue and they're going to have to raise rates to maintain their currency. The problem is 95% of the loans in Hong Kong are indexed in one month HIBOR (Hong Kong Interbank Offered Rate) and they reset monthly.

So you can't raise rates like they raised rates in 97-98 to keep the peg because you'll detonate an overlevered banking system.

I suggest you pay a lot of attention to this and decide whether or not you want to be around when things really hit the fan.

McCullough: How will China respond if at all, to a break in Hong Kong-U.S. dollar peg? How do you see this playing out?

Bass: I think the peg will go from a dollar-based peg to an RMB or an Asian basket a peg of currencies. And I think it will happen in one day, right? China will use its RMB exchange rate to buy the dollar reserves of Hong Kong.