Dear Investor,

In 2008, I responded to an unlikely Craigslist ad. A start-up financial research company then called Research Edge was looking for a junior analyst to join their team.

At that point in my career, I’d worked to get my Master’s degree and had been studying to get my PhD in molecular biophysics for the better part of a decade. By late 2007, investing in financial markets was a secondary interest that had begun eating up more and more of my time.

Still, my disparate qualifications seemed an unlikely fit for a financial research company run by a bunch of former buysiders. But since I’d be joining the Healthcare team, there was enough overlap for this start-up to take a chance on me. Offering to grind for free – everyone @Hedgeye worked for free (not free, but pretty much) the first couple years – just to get a shot probably didn’t hurt either.

Of course, Research Edge would later be renamed Hedgeye Risk Management.

Back then, we worked out of the old Taft mansion in New Haven on the edge of the Yale Campus. The heat didn’t always work, so in the winter you’d be bundled up and shivering. Sometimes the squirrels that lived on third floor would come down and run through the office.

Eventually, I moved over to the Hedgeye Macro team where I’d work alongside our iconoclastic CEO Keith McCullough. Around that time, Keith was making the rounds on various financial TV networks. I say “making the rounds” because Keith would occasionally get kicked off for being just a little too truthful.

The network people hated him – Keith had a habit of not holding his tongue when he disagreed with an “Old Wall” guest. But the viewers loved it and inevitably Keith would get put in the penalty box from time-to-time before the networks came calling again.

Those early days were a grind.

While our Macro risk management process has evolved significantly over the past ten years, Keith’s vision and approach has always been clear – It’s all about rates, spreads and deltas and 2nd derivative inflections in Growth, Inflation and #TheCycle are the factors to watch. Don’t get distracted by the shiny Macro Tourist objects.

Asymmetry, Risk And Critical Thresholds

As U.S. Macro analyst, Keith tasked me with measuring and mapping the U.S. economic cycle. What I’ve learned over the past decade is that as the cycle or mini-cycle matures, there is generally a slow layering of geopolitical, fundamental and market structure risks that finally build to a palpable crescendo.

Many times what occurs is that small risks are looked through and not discounted in the moment. Instead, what you get is the accumulation of latent risk or a dynamic where prolonged stability (via central bank intervention or when growth is accelerating) ultimately cultivates instability which then shows up, all at once, in dramatic fashion when the cycle turns.

On those days, you can feel it in the air and watch it on the tape. Critical thresholds get breached, acute volatility clusters and a begrudging consensus finally acquiesces to a market phase transition.

This phase transition births a fevered frenzy to characterize the new investing equilibrium and Trending macro regime. Eventually, everything settles down and the new trend perpetuates classic business cycle dynamics.

Credit Growth → #TheCycle

In an increasingly financialized and credit-driven economy like the U.S. credit trends and growth are inextricably linked.

Generally, credit growth is pro-cyclical as stronger-growth and rising spending drives income and employment higher which, in turn, drives consumption and confidence higher in a virtuous, self-reinforcing cycle. Credit serves to amplify the cycle with credit expansion following pro-cyclically as loan demand and creditworthiness both increase alongside rising incomes and higher household net wealth. Rising consumption accelerates economic and credit growth which feeds positive earnings revisions and stock buybacks. Stock market multiples rise.

The converse is also true.

As banks tighten standards and make it more difficult for Main Street and businesses to get credit, economic activity slows, which self-propagates lower loan activity as demand for credit suffers while credit worthiness deteriorates incrementally. Falling consumption, slowing economic growth and tightening credit markets cause negative earnings revisions and lower multiples.

It’s not particularly complicated – although pervasive factor crowding and modern market structure provide for more harrowing price reflexivity. (Think of Amazon: Tech = Consumer Discretionary = Growth = Momentum = a constituent of pretty much every factor basket of consequence.)

And, of course, ‘more’ is generally relativistic too, in the sense that an explicit consequence of having more of one thing means having less of another:

- More credit/debt today ≈ less household consumption tomorrow

- More growth now ≈ less base effect support next year

And so on.

Growth/Inflation/Policy → Asset Allocation

That’s why we track the rate of change in Growth and Inflation so closely. Macro remains an exercise in successfully front-running better or worse conditions from a slope-of-the-growth-line perspective. The Policy component of our framework both shapes and responds to the extant Growth/Inflation environment and the market’s pricing of both in a two-way communication loop… active participant, passive observer, both and neither.

Core to our conceptual framework is the contention that asset price movements – inclusive of all their dynamism and vagaries – remain a function of the prevailing growth and inflation regime, particularly over the Trend duration.

The implications of this are profound.

It means the problem of picking among all the different asset classes, globally, can be reduced and represented in a single unified framework - meaning that the ‘problem’ of how to choose from among a dizzying multitude of investment options is all really the same problem and a generalized model can be effectively developed and applied.

The art remains in conceptualizing a novel framework – then figuring out how to dynamically measure, map, and operate inside of it.

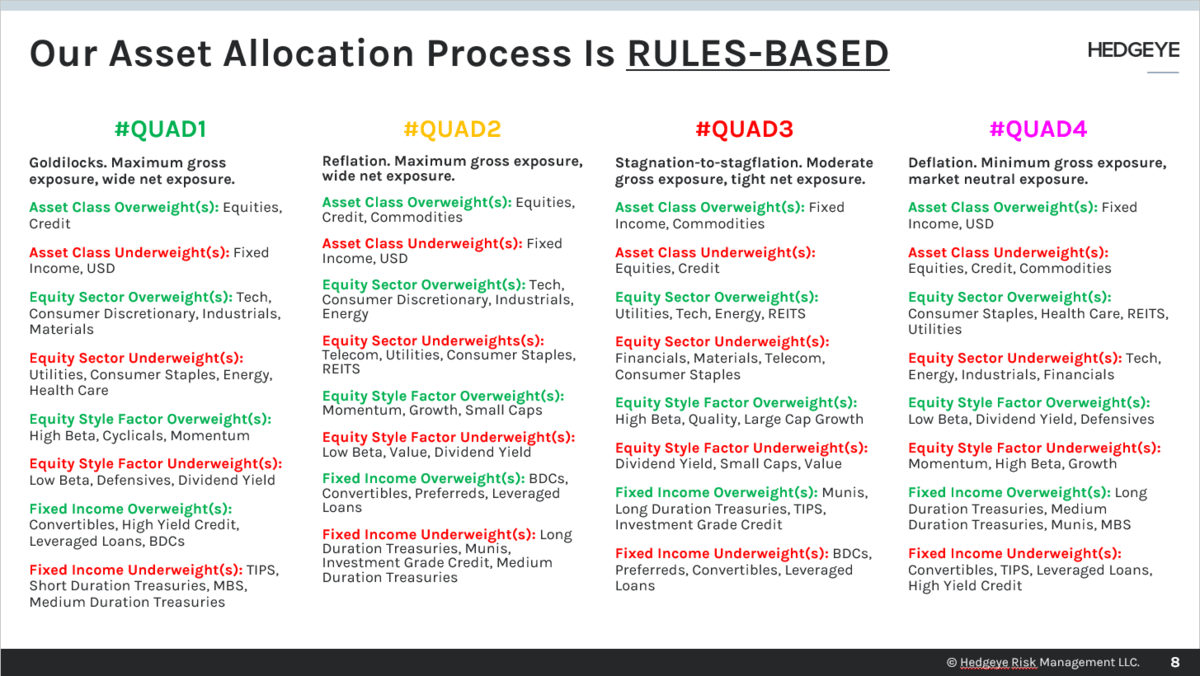

That’s where our Growth, Inflation, Policy model comes in (see the GIP and asset allocation summary charts below). From there, the data comes in and we probability weight evolving economic and policy conditions in the perpetual service of stalking asymmetric risk.

Where We Are Today

As you can see in the chart above, our Growth, Inflation, Policy model suggests that the U.S. economy was in Quad 4 for 3Q 2019 then will narrowly transition to Quad 2 in 4Q19E (we're closely measuring and mapping that transition into Quad 2 for any signs of Quad 3). The global growth picture (for the top-20 global economies) looks very similar: Quad 4 in 3Q followed by Quad 2 in 4Q19E (see the summary chart for the G20 economies below).

Here’s a common question we’ve received in the wake of our 4Q19 Macro themes call and some quick clarifying context:

Q: If you are expecting Quad 2/3 why are you still largely allocated to Quad 4 assets?

A: Quad 2 represents the base-effect defined projection. It’s still only a projection and requires (redundant) confirmation for us to take a convicted view in the setup. Recall, our risk management process effectively anchors on our A|B test which includes:

A. Mapping the evolution of the economic data and

B. Evaluating the market signal which defines what environment the market is currently pricing in.

At present, neither the macro data nor the market signals have confirmed an inflection out of Quad 4 so, simply, we’ve continued to stick with the same sector/factor exposures that have worked for the past year. We still have another month of Quad 4 in Q3 data to be reported and we’ll have to traverse peak profit cycle comps in 3Q.

When the A|B test begins to confirm the rotation, you’ll see that reflected in our commentary and positioning, in real-time.

Take a look at the data below, for instance. In no particular order, here’s a quick recap of the latest global macro data of consequence:

- Eurozone: Sentix Investor Confidence = -16.8 = lowest since December 2012. Sentix leads the German ZEW Outlook reading which leads the broader outlook for the German economy.

- German Factory Orders decelerated another -110bps, tanking to -6.7% Y/Y

- German Industrial Production remained mired in contraction at -4.0% Y/Y

- Irish Industrial Production decelerated -560bps, falling to -6.3% Y/Y

- U.K. same store Retail Sales decelerated another -120bps to -1.74% Y/Y

- Italian Retail Sales = decelerated -190bps to 0.7% Y/Y

- Japan Leading Indicators fell -2pts to 91.7

- Japan Eco Watcher Survey Outlook = -2.8 pts to 36.9 = lowest since 2H14

- Taiwan exports = decelerated -600bps to -4.6% Y/Y

- China Services PMI = fell to 51.3

- Mexico Business Investment = -7.6% Y/Y

- U.S. Small Business Confidence = -1.3pts to 101.8 = back to the January lows while fully retracing all of the post-election ebullience.

The above all represent multi-year or cycle lows and should serve as a kind of rhetorical contextualization of the prevailing state of global cyclical conditions, obviating any need for further fabricated over-analysis.

I’ve said it before, but it’s worth repeating when traversing the chop associated with prospective cycle inflections: The early bird catches the worm, but the 2nd mouse gets the cheese.

In the event we get a (A|B test) confirmable inflection out of Quad 4, there will be plenty of 2nd mouse opportunity.

To process and patience,

Christian B. Drake

Macro Analyst