“I believe we have to scare the bejeezus out of China on Japan.”

-Richard Nixon

One can only imagine what Nixon would have done on Twitter.

As Richard McGregor reminds us in Asia’s Reckoning, “in private, Nixon was as crude and unsentimental about rival foreign players as he was in targeting his domestic enemies in his notorious Oval Office rants.” (pg41)

Trump believes he has to scare both the Fed (into cutting rates aggressively) and stock market bears alike that he controls The Game on Chinese trade negotiations. Despite his prior tweets, once again, there is no “trade deal” this morning…

Back to the Global Macro Grind…

I always get asked about “client feedback”… you know, what are the big players in The Game most concerned and/or excited about… on that score, the concerns and excitement are usually about the same two things:

- The Fed Cutting Rates

- Trump Trade Deal

Once you get through today, fully loaded with the month-end markups that you saw with SPY hitting all-time highs at the end of April (then whammo, May happened), you will have:

A) Your rate cut … and

B) No Trade Deal

Then what?

Since I don’t see anyone in the daily fishbowl who called The Turn (i.e. going from Bullish on US Growth #Accelerating for the 2 years prior to Bearish at the end of Q3 2018 as The Cycle was about to peak and rollover)…

Why are so many so sure what to do at this stage of the Fed rate cutting cycle?

Especially if the Fed isn’t as dovish as the Quad 4 In Q3 US economic data is going to be from now until the SEP Fed meeting, there’s an expectations mismatch already “priced into” the market.

That’s why I think there’s a high and rising probability of a black-hole in components of the US Equity market that you’ll have to risk manage between now and October when the worst of the US Earnings Cycle hits (i.e. Q3 Earnings).

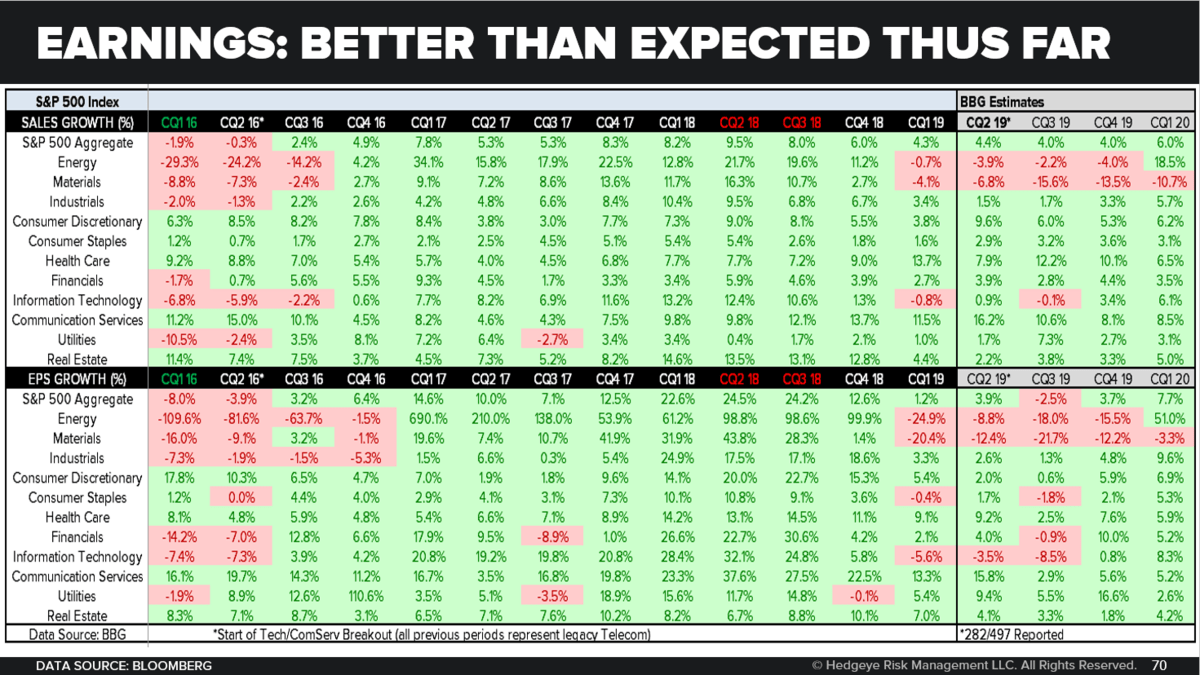

To be fair (and I’m always hugely fair when it comes to being very very fair), Q2 Earnings Season has not only been “better than expected”, but non-recessionary (i.e. NEGATIVE y/y EPS). Here’s the real-time data dump on that:

- 282 of the SP500’s companies have reported aggregate year-over-year (y/y) EPS growth of +3.86%

- Financials (53 of 68 have reported aggregate year-over-year (y/y) EPS growth of +4.0%)

- Technology (32 of 67 have reported an aggregate year-over-year (y/y) EPS DECLINE of -3.5%)

Oh, you weren’t told about Part 3 of the ongoing US Earnings #Slowing story, eh? Of course not. The Old Wall and its media only talks about the upside. “So” let’s only talk about AAPL’s beat today!

As Tech enters its #EarningsRecession, the 2 Sectors of the SP500 who are already in a clean cut #EPSRecession remain:

A) Energy (12 of 29 companies have reported an aggregate year-over-year (y/y) DECLINE of -8.8%)

B) Materials (16 of 26 companies have reported an aggregate year-over-year (y/y) DECLINE of -12.4%)

If you’ve been long and/or “overweight” either Energy or Materials since we made the Full Cycle Investing turn call back in SEP of 2018, I’ll pray for your family and their offices.

If you’ve been long something we’re long and/or overweight like Utilities (XLU) where 7 of 28 companies have reported aggregate y/y EPS GROWTH of +9.4%, well done. That made “expensive” exposures more expensive all the while.

If you’re long US Housing (ITB) like we’ve been since making the Full Cycle Investing turn call back in SEP of 2018, very very well done! Unlike the #slowing data you have to play a game of stock-picking chicken within Industrials (XLI), the ROC (rate of change) data for this domestic cyclical continues to #accelerate:

A) Pending US Home Sales for the month of JUN #accelerated to +1.6% year-over-year growth

B) That’s the 1st month in the last 18 where the GROWTH rate was POSITIVE on a year-over-year basis

If you bought Housing (ITB) when it was “cheap” on the wrong numbers 18 months ago, you got your clock cleaned by Quad 2 (US Growth & Inflation #Accelerating) … and rates breaking out to the upside in kind.

Yeah, so many pivots and so many places to get in and out of if you get The Cycle and The Quads right, eh? Unlike consensus, that’s why I don’t wake up panicked about trade deals and rate cuts. My p.a. hasn’t been scared for 3 years.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.00-2.12% (bearish)

UST 2yr Yield 1.77-1.91% (bearish)

SPX 2 (bullish)

RUT 1 (bearish)

Utilities (XLU) 59.09-61.14 (bullish)

VIX 11.99-15.74 (neutral)

USD 96.40-98.35 (bullish)

Oil (WTI) 54.48-58.83 (bearish)

Nat Gas 2.08-2.30 (bearish)

Gold 1 (bullish)

AAPL 203.51-216.42 (bullish)

NFLX 294-341 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer