Below are analyst updates on our twelve current high-conviction long and short ideas. Please note we removed UnitedHealth Group (UNH) from the short side of Investing Ideas this week. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

EXP

Click here to read our analyst's original report.

Our macro team held their Themes recently, and it was unusually important for cyclicals. We’ve been seeing weakness in basically every sensitive series we track, with a big part of the problem stemming from mid-2018 being an impossibly hard compare. Critical takeaways for Industrials & Materials?

- “2016 served as an acute reminder that you don’t need an official recession to get an earnings recession.”

- “The Fed can print money, but it can’t print earnings.”

- “USD is setting up for a big move lower in 2H19E and beyond”

Our Macro team also expects a more supportive housing environment into 2020. Comps for the group get MUCH easier in 2H19, and mortgage rates have plummeted. If a spike in mortgage rates got these companies into a period of weak demand, lower rates might be expected to get them out of it. The activist angle at Eagle Materials (EXP) adds a bit of a tailwind, if a less near-term benefit than strengthening demand.

GIL

Click here to read our analyst's original report.

Part of our thesis on Gildan (GIL) is the fashion basics opportunity and how the company has invested in new supply growth to compete in the category. Growth requires more than just having the available capacity. Gildan acquired two brands well known to screenprinters (at very attractive prices) in order to target different demand drivers in fashion basics.

The Gildan brand is the lowest priced fashion basics t-shirt which is both a volume driver for the category as well as a share taker. Buying the American Apparel brand out of bankruptcy gave Gildan a premium brand to position at a much higher price point for the most fashion forward customers. The different brands even though they are made by Gildan (at nearly the same cost) facilitates screenprinters commanding a higher price for the t-shirt. This allows the retailer of the shirt, whether it is a concert or sporting event, etc., to sell the t-shirt for much higher prices.

In other words the different brands make it easier for a concert to sell a $35 t-shirt when the blank is from American Apparel rather than Gildan which made the concert goer’s $15 t-shirt. So Gildan now has brands positioned above and below the largest competitors in fashion basics and the capacity to grow by a third when it is fully utilized in the next couple of years.

ANTM

Anthem (ANTM) remains a long as the advantage they have in developing a PBM in a new era is probably more valuable than ever.

Recently, the White House told reporters they were withdrawing the rebate rule for Medicare Part D. The rule change was a major headwind for the MCOs land its withdrawal is good news, especially for those that have an in-house PBM, for now. For pharma, the shift in policy is very, very bad news.

We had highlighted a significant delay or withdrawal of the rule as a risk to the UNH short because it was so hotly debated at the White House. There was a 6 month delay in its initial release with the president finally backing Sec. Azar, the strongest advocate for the policy. That did not stop policy advisor Joe Grogan, a budget hawk, from lobbying against the effort and its $177 billion price tag. In the end, the president made the decision to withdraw the bill and focus on other, more direct efforts to bring down drug prices.

The news is welcome for the PBM industry but they are hardly out of the woods. In fact, congressional action may yield a much worse result than any regulatory change, from their perspective. Drug price policy legislation making its way through the committee process and a priority of both the chairman of Senate Finance, Sen. Chuck Grassley, and the chairman of Senate HELP, Sen. Lamar Alexander, includes:

- Requirement that 100% rebates generated on behalf of commercial plans are passed through to sponsor or employer

- Prohibition on spread pricing

- Required reporting by PBMs to plan sponsors or employer groups on amount of rebates, total spending and drug utilization

At the White House, the focus has turned to more direct efforts to reduce drug prices, which is where things could get very dicey for pharma. With the president's announcement on Friday of a "most favored nation status" for Medicare via executive order, he has reset the baseline with quasi-negotiation. It will be up to Congress to moderate this fairly radical approach and that may just be the point.

Sen. Grassley and others have expressed opposition to anything the smells of negotiation. House legislative efforts have made direct negotiation a priority. One of the sticking points over Senate Finance legislation is a provision offered by Senator Wyden that requires rebates in Medicare Part D if price increases exceed a threshold amount. This impasse has to be broken and the withdrawal of the rebate rule coupled with the White House's proclivity for executive action creates an urgency to act. That action is very likely to include significant restrictions on drug price inflation, in one form or another. Even if the rebate system remains in Medicare, the fuel that drives it - ever increasing drug prices - will be diminished.

Finally, the OIG in issuing the rebate rule reminded us that two practices are not covered by existing safe harbor; quid pro quo agreements for rebates in return for formulary placement and using rebates in Medicare to subsidize premiums in other lines of business. Given the public airing of PBM practices, enforcement risk is higher now than it was before the debate began.

As we wait and see if the White House strategy will work, we removed UNH from the short side. ANTM remains a long as the advantage they have in developing a PBM in a new era is probably more valuable than ever.

TSLA

Click here to read our analyst's original report.

With the tax credit step-down, no new model or variant introductions, and international order depletion, the market should be able to anticipate Tesla's (TSLA) 2H19 weakness clearly enough, especially if the macro backdrop softens. With no major introductions of Model 3 Variants at lower price points or untapped geographies, 2Q19 deliveries look likely to be the high water mark for 2019. Better deliveries in 2Q likely pushed the next major catalyst into October.

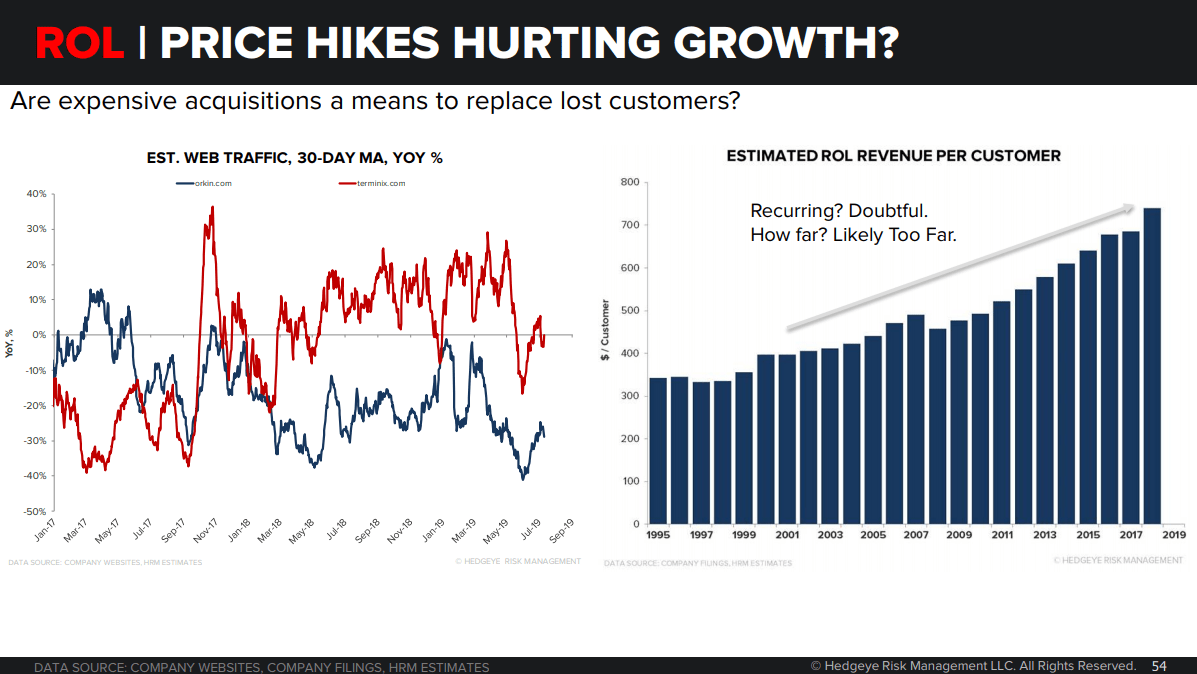

ROL

Click here to read our analyst's original report.

Rollins (ROL) web traffic suggests share loss to a resurgent (well, using normal business tools now at least, like salesforce) Terminix. A wet May, which disrupted farming, also shows up clearly in the traffic series for ROL and Terminix.

Furthermore, acquisitions have filled in during periods of weaker organic growth. This is fine, as long as the acquisitions are reasonably priced and successfully integrated. However, smaller pest companies often have better relationships as acquisitions by larger players destroys culture and employee retention. We estimate that, across the pest control industry, the acquisition price relative to revenues has nearly doubled in the last five years.

Are expensive acquisitions a means to replace lost customers?

DVA

Click here to read our analyst's original report.

An important event to watch for our DaVita (DVA) short thesis is the movement of AB 290 through the California Legislature and the Third Party Payment rule under consideration at the White House.

Having cleared the California Assembly and been referred to the Senate, AB290 is set for Senate Committee hearing on July 3rd, following more or less the same path to approval as last year’s identical but vetoed legislation. This bill, if enacted singles out Large Dialysis Organizations for Medicare level reimbursement when a third party, like the American Kidney Fund, pays commercial insurance premiums for ESRD patients.

Similarly, the White House is reviewing a rule that would regulate third party payments at the federal level. While we do not expect CMS to take as bold a step as the California legislature, they are likely to require more disclosure and reporting that discourages migration to commercial payers by dialysis patients that are otherwise eligible for Medicare. Depending in the federal response, the California solution may spread to other states.

There is also an ongoing lawsuit in Florida where Florida Blue has accused DVA of similar practices highlighted in California, among other things.

With the ~10% of patients who are commercially insured accounting for 110-115% of DVA’s profit, the increased regulation and prohibition of third party payments will be a much big deal to DVA.

HQY

A Health Savings Account must be tied to a High Deductible Health Plan (HDHP). HDHP dates back to “Consumer-Driven Health Care” (CDHP) movement of late 1990s. CDHP's intent was for insured to have “skin in the game” to motivate consumer behavior, although without price transparency, negotiation leverage or comparative quality measures.

HSA enrollees and employers make pretax contributions to balances. Non-medical expenses are taxed at income tax rate + 20% penalty before age 65. Non-medical expenses are taxed at income tax rate + 0% penalty after age 65. Balances can be invested in equity related instruments.

HealthEquity (HQY) and other providers earn per member per month service fees, yield on cash and investment balances, and interchange or transaction fees when a customer uses a debt card to purchase services.

On our HQY short thesis, we think member growth is at risk of incremental deceleration as employment slows given the macroeconomic set up, and possibly declines in a recession scenario. Republican-driven policy to expand HSAs to working Medicare populations are dead in the Potomac River as Capitol Hill remains divided for the for the foreseeable future.

While there will be a delay between falling rates and Custodial Yield, the path to lower rates appears all but assured. We believe investors will recognize the future impact despite the custodial asset investment structure with substantial earnings headwinds from falling yields.

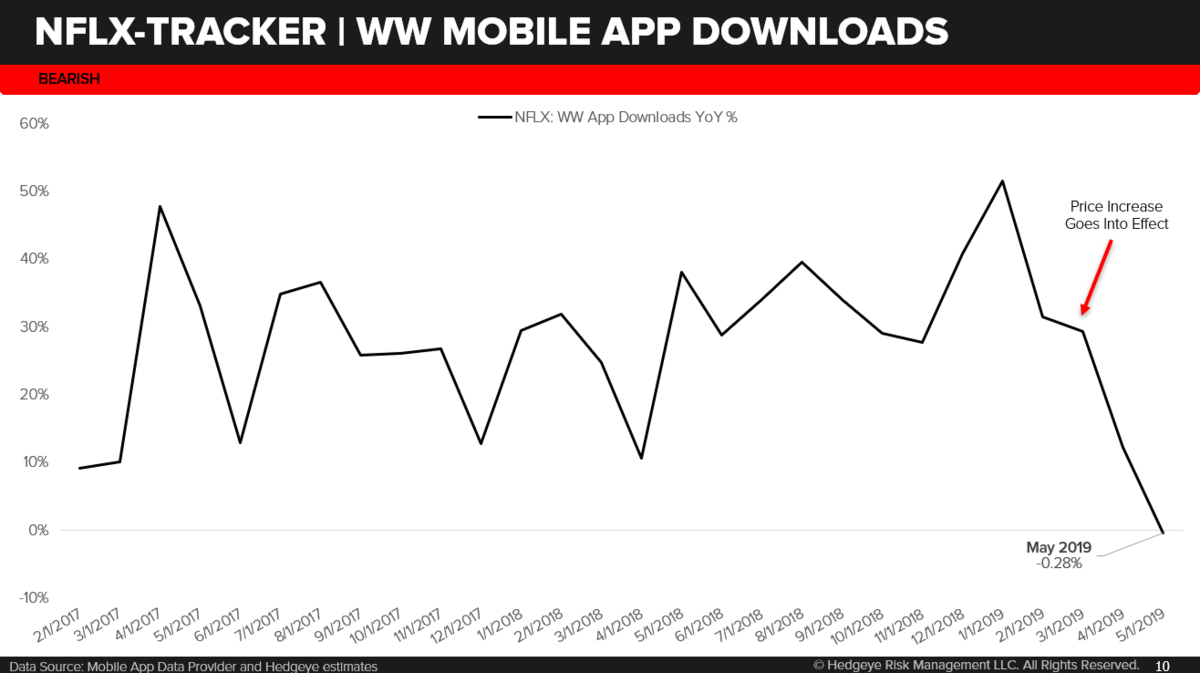

NFLX

Click here to read our analyst's original report.

We added Netflix (NFLX) as a short on the belief that investors were overestimating NFLX's pricing power and ability to drive further adoption in key developed markets, especially given the looming competition from legacy media. Our conviction in the short grew following Q1 earnings, and the data we track intra-quarter indicated a material slowdown in gross subscriber additions in Q2.

In 2Q19, NFLX reported the largest net paid subscriber miss since 2016. The weakness was broad-based, with gross subscriber additions missing management's forecast "across all regions" and the U.S. paid subscriber base declining QoQ for the first time in the company's streaming history. Meanwhile, management's 3Q19 global paid net subscriber guidance of 7.0 million looks aggressive and likely sets the stage for another disappointment later in the year. Overall, we believe this is the beginning of the end for the NFLX growth story.

In the chart below we show the meaningful drop off in NFLX app downloads. Communications analyst Andrew Freedman hosted an institutional update presentation on his thesis and review of the quarter this week. You can watch for free. Click here for special, one-time complimentary access.

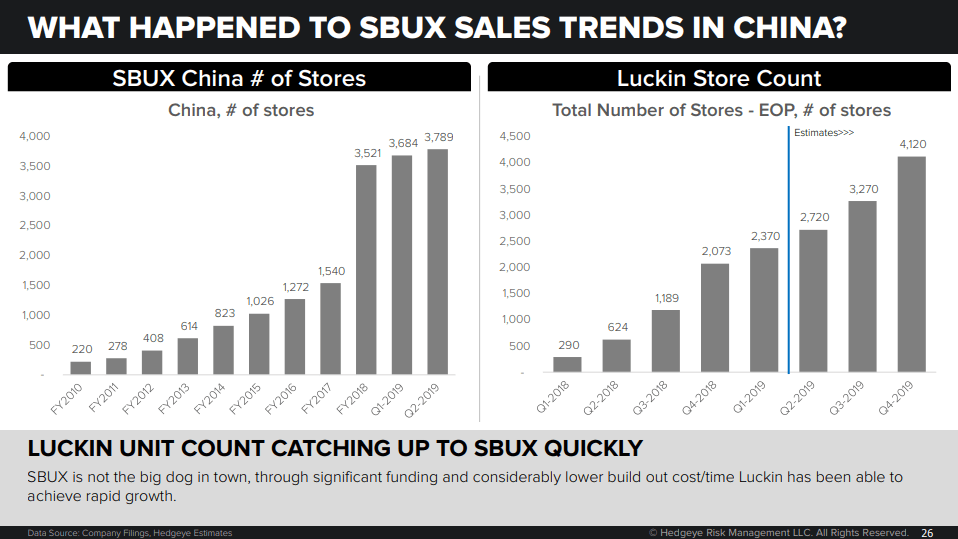

SBUX

Around the world, Starbucks (SBUX) is considered a super-premium brand, and this is especially true in China. Therefore, that pricing strategy is reflected in the locations, the decor, and the prices of the drinks themselves. For example, for the same cup of cappuccino, Luckin coffee 24 RMB, Starbucks sold for 31 RMB. If you order a cup of coffee online, Luckin needs to add a 6 RMB shipping fee, a total of 30 RMB, still 1 RMB cheaper than Starbucks. It’s significantly cheaper because if you buy 2, you get one free, and if you prepay for 5, you get 5 for free, which is why so many people have tried Luckin. This would help partially explain why Starbucks sales have slowed so significantly. Add to that free delivery if your order is above $5!

SBUX is not the big dog in town, through significant funding and considerably lower build out cost/time Luckin has been able to achieve rapid growth and is catching up on SBUX unit growth.

NSP

Click here to read our analyst's original report.

Below are a few key thesis points on our Insperity (NSP) short call:

- It need not be negative/recessionary for PEOs to re-rate downward, in part because costs catchup with pricing or regulatory catalysts.

- Even if relative performance doesn’t, exactly, the key metrics tracked in the industry often track employment trends. These metrics, some of which had stagnated for years, may revert to prior levels in a slower growth, tax reform comp environment.

- NFIB may be the most relevant, and has lost some of its post tax reform luster in recent readings.

If wage pressures increase and NSP tries to raise prices in a slowing economy to cover benefit cost increases, will churn increase? Seems likely. Other PEOs have seen retention increase, and churn is typically procyclical. Higher churn in recessions tends to add to unit costs at an already difficult point in the cycle. NSPs contract with its clients can typically be canceled within 30 days.

MAR

Click here to read our analyst's original report.

For Marriott (MAR), we still see a disconnect between sentiment and valuation vs industry and company specific catalysts. RevPAR matters folks, even as the bulls point to the much lower impact to EBITDA from RevPAR changes. Historically, valuation multiples compress dramatically following negative RevPAR pivots and we expect lower RevPAR forecasts and multiple contraction for MAR.

Looking past just 2019 unit growth, MAR’s pipeline is showing some cracks in its foundation – a potentially big blow to the bull thesis. The bear case could already be accelerating as MAR will be under a microscope to deliver EBITDA beats and incrementally more positive forward looking commentary with regards to the pipeline and RevPAR outlook. We see longer term top line and EBITDA growth as likely to disappoint with more negative evidence to emerge over the next several quarters. Our call is less about near term EPS, but more about multiple contraction as growth decelerates.

GOOS

Click here to read our analyst's original report.

Canada Goose (GOOS) has one safe product: an iconic parka that’s become America’s go-to for ultra-cold weather. Buyers own and use these $1000 coats for about a decade, making GOOS a decidedly consumer durables company. But now, the luxury retailer – with a steady but small TAM in parkas– is trying to become a non-durables company.

We’ve never seen this before anywhere in retail, and it’s fair to say that no management team will be able to navigate the volatility of this growth model. Sales are already slowing, and tail risks are being overlooked. We see ~1000 basis points of margin loss built into their model; around 300BP/year for the next three years. Since consumers are slow to adopt product lines outside of the core flagship parkas, these layered growth initiatives in non-durables are unlikely to scale at any meaningful rate. This will inevitably put further strain on growth in parkas to continue driving the business.