The guest commentary below was written by Christopher Whalen. It was originally posted on The Institutional Risk Analyst.

This week in The Institutional Risk Analyst, we return to the activities of funds operating in the world of distressed real estate and corporate debt. We noted a few months back that some of the biggest players in the distressed debt industry were preparing for a comeuppance in the market for collateralized loan obligations or “CLOs.” New funds were be created to absorb and profit by busted CLOs and distressed financial institutions such as Deutsche Bank AG (DB).

But the anticipated selloff has not happened as yet, in large part due to the rally in the bond market. Indeed, the decline in bond yields since year-end 2018 has caused a surge in new CLO issuance, including the remaining backlog from the Q4 2018 fiasco. It's almost like the Fed wanted to refi CLOs just one more time. Just as the entropy of global finance seemed to be heading from temporary stability to chaos, the Fed goosed asset prices once again and bought the equity markets a little more time.

“Issuance in the US Collateralized Loan Obligation (CLO) market is just behind the record- setting pace of 2018 despite criticism of the asset class and higher spreads eating into returns,” writes Kristen Haunss. “There has been US$63.84bn of US CLOs arranged this year through June 26, just behind the US$65.62bn arranged during the same period in 2018, according to LPC Collateral data. A record US$128.1bn was issued last year.”

The chart below from SIFMA shows the most recent data for new securities issuance in the US markets.

Notice that issuance of mortgage bonds and corporate debt have accelerated with the decline in bond yields. Indeed, we still seem to be in a seller’s market for securities, real estate and any other assets that investors can identify. The driver for this secular tidal wave of demand for assets is the action of global central banks, which are encouraging deflation in many economies around the world because of the fact of now $13 trillion in government debt with negative yields.

Despite their education and intellect, many economists do not seem to grasp that reducing global income and economic activity, and increasing debt, via negative interest rates accelerates deflation. At some point we believe that economists as a group will need to admit that negative interest rates have only delayed the day of reckoning for the global economy as the stock of public and private debt has exploded. Entropy. Economies may not be closed systems as posited in the three laws of thermodynamics, but the comparison remains apt.

David Kotok of Cumberland Advisors notes rightly that the gift of lower debt service via negative rates can only be given once to indebted governments. But in the meantime, we see little indication that the vast demand for yield or more accurately duration will abate, meaning that we see continued support for asset prices at current crazy levels -- for now. Yet growing numbers of economists are criticizing the use of negative interest rates to paper over a mounting global debt crisis.

Agustín Guillermo Carstens, general manager of the Bank for International Settlements and former head of the Banco de Mexico, last week rebuked global central banks for pursuing negative interest rates. He said little would be achieved by another round of loosening by central banks in countries with interest rates already at rock-bottom levels.

“I mean how much more stimulus will you get if interest rates are reduced in the margin another 25 basis points? It is difficult to see how that will generate a lot of bang for the buck,” Carstens warned. “This has to be balanced out with the potential risks in terms of asset misallocation and mispricing, and financial stability,” he said.

The BIS chief also noted the ratings cliff that has developed in the EU, with roughly half of all corporate credits just barely at investment grade or “BBB” rated.

“Credit standards have been declining as investors have searched for yield. Should the leveraged loans sector deteriorate, the economic impact could be amplified through the banking system and other parts of the financial system. There could be sharp price adjustments and funding tensions,” said the BIS.

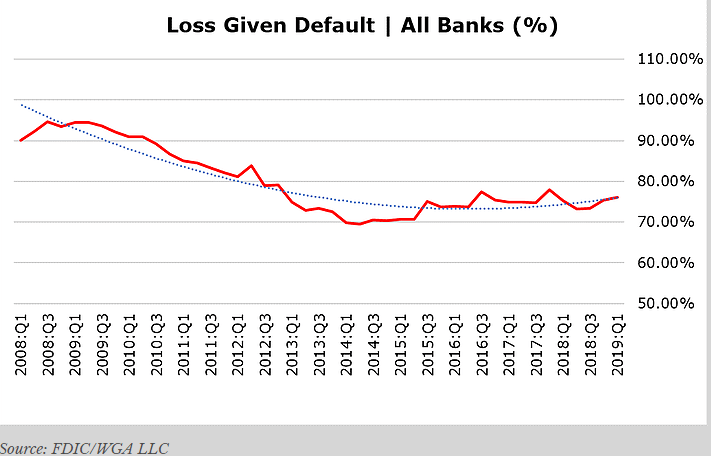

As we observe in The IRA Bank Book for Q2 2019, net loss rates for all manner of real estate loans owned by banks are just barely positive after quarters spent in negative territory. News reports of private equity funds raising cash for distressed real estate strategies are certainly of interest, but the timing of the opportunity still seems obscure. We continue to believe that policies such a quantitative easing or “QE” have embedded significant future credit losses in financial assets, but just when this risk will be recognized by the markets is an open question. Thus our use of the entropy metaphor.

As we wrote this quarter in The IRA Bank Book:

“The credit quality of the US banking industry remains pristine – at least by appearances. The bank regulatory data still suggests that credit has no cost in most real estate related asset classes, including residential and multifamily first lien mortgages, HELOCs and construction loans. But the key question asked by more astute analysts is whether the asset price inflation engineered by the FOMC is masking a lurking problem in terms of future credit losses. Default activity for all loan categories was unchanged at 0.5% in Q1 2019, while loss given default (LGD) for all loans and leases rose slightly to 76% in Q1 2019.”

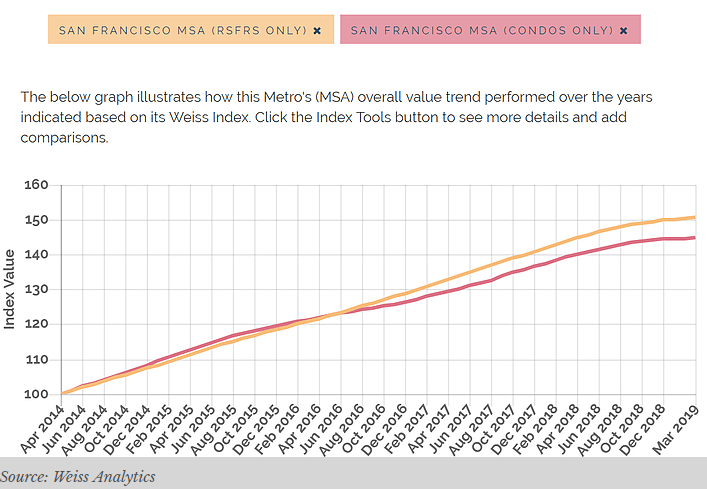

Even as we wait for the day or reckoning in the world of CLOs, there are growing reports of a slump in US housing prices after six years of rising valuations. The charts below from Weiss Analytics (WGA LLC is an advisor to and shareholder in WA), show that while home price appreciation has certainly slowed or even stopped entirely in some markets, there is as yet no broad-based decline in asset prices for single family homes in either the New York or San Francisco MSAs. Just as in the case of the global bond market, too few housing assets chased by oceans of global fiat capital means asset price inflation well about the Fed's two percent inflation goal.

While excesses are clearly building up in the global system, we think the bad news is that central bankers have gotten it wrong when it comes to deflation. In sworn testimony before Congress, both former Fed Chairs Ben Bernanke and Janet Yellen stated that fighting deflation today is more important than the asset price volatility that comes tomorrow. But do either Bernanke or Yellen truly understand what they have done to financial markets?

The Fed's fight against deflation has been a dismal failure. Now the global financial system sits perched atop a cliff, with asset prices and credit loss rates entirely correlated and the only place to go, it seems, is lower in terms of prices and higher in terms of realized loss rates. The only question that remains is when and how quickly will the much anticipated repricing occur? Again, entropy. Judging by the volatility observed in the financial markets over the past year, the answer seems clearly that change will occur faster and on a larger scale than in the past.

Economists and central bankers in their arrogance suppose that they can control the forces of markets and economies, and even direct these systems toward stable states of "equilibrium." Anyone who works in the physical sciences, however, will tell you that in fact just the opposite is true; that absolute zero where entropy occurs is the limit of the natural world's ability to measure a lack of heat. When central banks armed with the idea of negative interest rates tinker overmuch with the workings of global finance, the massive forces that accumulate can wreck terrible destruction.

Thus we suggest that our readers ponder the third law of thermodynamics and how the concept of entropy relates to the global phenomenon of deflation. As we move from the apparent but transient appearance of stability to chaos and disorder in a global economy with grotesque levels of debt, the mistaken judgments made by Bernanke and Yellen when it comes to fighting deflation with hyperinflation of the US economy during the past decade may govern the fate of the global economy for many years to come.

EDITOR'S NOTE

This Hedgeye Guest Contributor piece was written by Christopher Whalen, author of the book Ford Men and chairman of Whalen Global Advisors. Over the past three decades, he has worked for financial firms including Bear, Stearns & Co., Prudential Securities, Tangent Capital Partners and Carrington. This piece does not necessarily reflect the opinion of Hedgeye.