Editor's Note: Hedgeye launched coverage on the Cannabis sector led by analysts Shayne Laidlaw and Howard Penney on November 8th. To access our Cannabis team's institutional research email sales@hedgeye.com.

As part of their new Cannabis sector launch, Laidlaw and Penney took a deep dive look at their top Short in the space, Canopy Growth (CGC) and top Long Cronos (CRON).

Since then, shares of CRON have surged 76%, while shares of CGC shares have fallen 4.3%.

As Laidlaw and Penney wrote in November:

|

"While the cannabis industry certainly has great growth prospects, we believe there is far too much optimism built into top-line projections and thus the market value of some important equities in the space." |

Why the divergence between CRON and CGC?

Back in November, Penney and Laidlaw wrote...

|

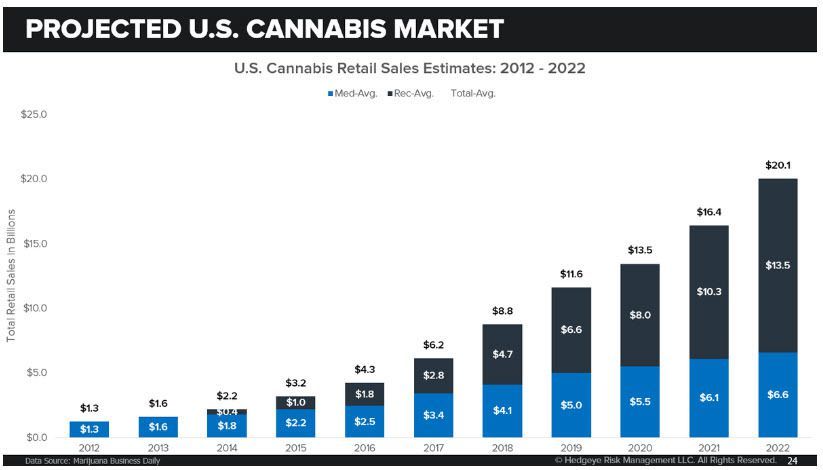

"The current state of the cannabis industry can be described as a double bubble. The current valuation of the publicly traded companies participating in the cannabis industry (CGC and TLRY have a $14B and $10B market cap., respectively) dwarfs the size of the current legal marijuana industry (2018 global legal cannabis sales are expected to be roughly $13B – illicit market is estimated to be $150B globally). On top of that, there are projections coming from CEO’s of large U.S. publicly traded companies touting the possible TAM in the next 15 years to be $200 billion, and we have heard more bullish estimates of $500 billion from publicly traded cannabis companies. With all the capital flowing into the industry, you now have companies planting enough assets to nearly supply the majority of global demand, all grown in Canada! |

Specifically on our short CGC call, Penney and Laidlaw argued that the company is "the epicenter of the bubble," a "four-year roll-up story" with a "high cost of production." That's why Penney and Laidlaw conclude it is "unlikely [CGC can] generate any meaningful EPS over the next 5 years."

Meanwhile, looking at long CRON, Penney and Laidlaw like its "asset light model" and "limited exposure to growing plants." "As flower drifts away and alternative consumption methods grow share, this will put CRON at the leading edge," our Cannabis team writes. And furthermore, "Given the operating structure, we estimate that CRON GAAP Gross Margins should hold up as some of the best in the industry."

For more insight on our CRON call watch the video below.