Watch the replay below. Also below is a brief transcript (of key excerpts) from the webcast.

Keith McCullough: All right, there's a nice big audience joining us this morning. It's free for the newbies, so welcome. We appreciate your time and certainly your attention to the process for those of you that are paying for The Macro Show. Thank you.

So here’s what happened yesterday. The market was immediate-term trade oversold. That's Point A.

Point B is that Private Equity Powell came out intraday day saying, “We agree with the Hedgeye view that at some point we could consider a rate cut.”

So at the low end of the range, the stock market was going to go up anyway. At the top end of the range in the Nasdaq, which is now a 7,722, you're a short seller. Why? Quad 4 economic conditions.

So again, you're seeing that this morning in the ADP number. That's why the 10-year yield collapsed down to 2.08% from 2.12% when I got up this morning.

Economic data is setting up to deteriorate at a faster rate. That's what we call Quad 4. Quad 4 is when both growth and inflation are slowing. Profits are slowing. And the Fed is going dovish as the market's getting more concerned about those fundamental facts. So again, we'd be a short seller of Semiconductors at the top end of the range. That's one of the juiciest spots to be. SMH on the short side.

The problem remains that you can't eliminate the economic cycle. While it's nice to imagine PE Powell and the Vice Chair of the Fed coming out every single day, ringing the cowbell and saving you from the cycle. That damn cycle won't go away.

I'm definitely not a buyer. I'm looking to make short sales on the things that we do not like in Quad 4.

Alright, sectors yesterday. Everybody was a winner! At the low end of the range I'm a buyer of Real Estate. We like REITs in Quad 4. We also like Utilities. Those would be the top two favorite ideas in sector space, Utilities and REITs. And now you can buy them on sale.

You will not get to buy Treasury bonds on sale today. Unfortunately for those who have not understood the call, because again the ADP number knocked the 10-year Treasury yield down by another four basis points and we’re off to the races.

If Treasuries get to the low end of the range, yes we would buy the 10-year. Man, this is amazing. Amazing, but not surprising. The low end of the 10-year Treasury yield risk range is 2.03% to 2.35%. So again, a couple of points I'd make. The top end of the range is the lowest lower high that we've had. And the low end is the lowest low that we've had. Okay? So that's good. If you are bullish on Treasury bonds, it remains our #1 asset allocation, across the curve, going all the way back to Quad 4 in Q4. That’s probably a good spot to take some questions.

Darius Dale: Alright. Turning to viewer Q&A, Max is asking, “With the U.S. in Quad 4, and wind of Fed rate cuts, will that push the U.S. economy into Quad 3 almost immediately (i.e. should we be prepared to pivot back in a Quad 3 assets the moment the Fed blinks)?

McCullough: If I thought that was the answer, I wouldn't have titled today’s Early Look, “Fading Fed Cowbell.” We make a call every day, it's a call based on our process. We're the ones who told you that the Fed was probably going to hurry up on a rate cut. Don't forget.

So again, I think that preemptively now people are hoping the rate cut comes in June. But the Fed doesn't have the economic data to support it until July and August. After the June FOMC meeting, we're going to have Quad 4 economic conditions. On slide 14, you can see where our current Nowcast is for the U.S. economy, which is below consensus. We're at 1.58%. So it's not about what the GDP number feels like, it's what the GDP numbers are doing.

So you're going to have that number in July. You're going to have the lowest CPI or headline inflation number in August. At this point, if the Nasdaq's down -15% to -20%, then you're going to have the conditions where the Fed might consider a rate cut. So that's when I think it's going to happen. If I changed my mind on that, I'll let you know.

Dale: Yeah. You heard Bobby Kaplan this morning (the Dallas Fed President) who’s a non-voter. He represents the general belief of the institution that they're close to neutral. They’ll probably need to see the River cards in the form of the GDP data you just highlighted. That'll be out on the 26th of July. The CPI data you referenced will be out on August 13th and then ultimately Jackson Hole in late August.

McCullough: That's our setup. The real risk is that investors buy the damn dip at some point in August and what if it's not a dip? What if the Fed needs to cut by 50 to 100 basis points just to satisfy the market?

Dale: It looks like we're going in that direction.

McCullough: So again, the real question is are they dovish enough? Did they cut enough? And I think that that'll be the real risk management exercise.

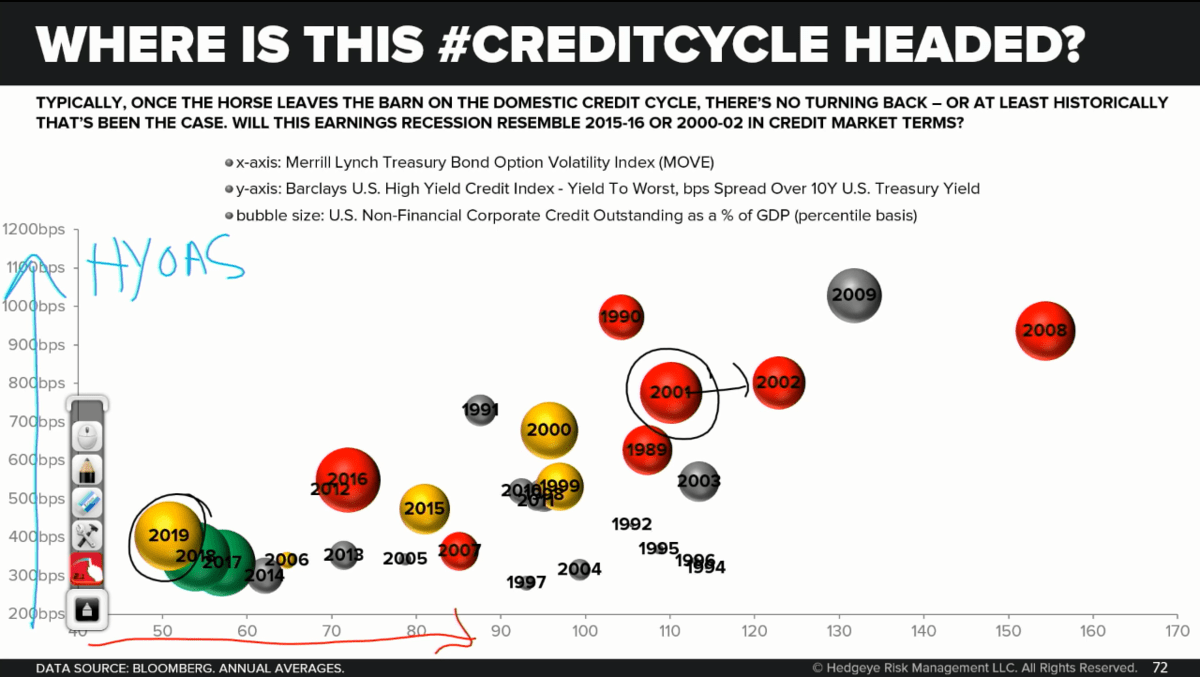

Here’s an important point. This is called the MOVE Index. It’s a Treasury volatility index. So the MOVE is moving. It was plus 20% last week. That’s on the week.

Dale: So on the MOVE Index, go to slide 72. This is one of my favorite charts. If you don't fundamentally understand credit cycles, this is a phenomenal chart for you to review it. There's so much information in this chart. What we're showing here on the X-axis is the MOVE index Keith was just referencing, the Treasury bond market volatility index. On the Y-axis we're showing high yield option-adjusted spreads. The size of the bubble is calibrated to the leverage of the corporate non-financial sector. And what I mean by that is it's a ratio to GDP that effectively shows how levered the corporate sector is.

So what you see is that we're very late cycle currently in 2019. Prior to what we've seen in the most recent two months, the MOVE index was about as low as it can possibly get.

Once the MOVE starts moving the market is effectively pricing in interest rate cuts by the Federal Reserve. And the faster the MOVE moves out, it communicates that the market doesn't believe the Fed’s communication. It's effectively forcing the Fed to act at the same time as high yield spreads are widening, as they currently are, up 74 basis points a month over month.

That's a real big signal to investors that the Fed is behind the curve. And that's a real big signal. So if the Fed waits until September to cut, these counter-trend bounces could really fade and dissipate. So that's the real big risk it’s that the 2019 dot is moving and there's only one way to go once the horse leaves the barn.