Shares of luxury winter-coat manufacturer Canada Goose (GOOS) are getting unequivocally crushed this morning. They are down over 25% as of this post.

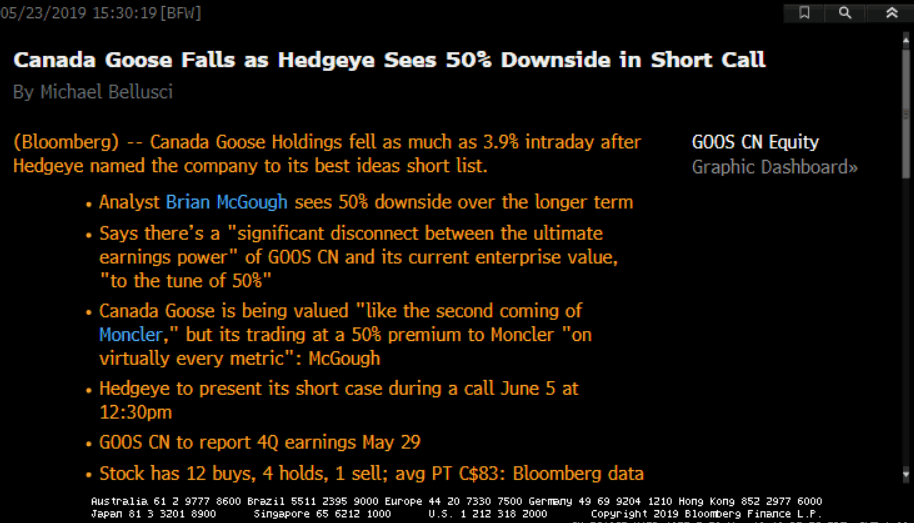

For the record, our veteran Retail analyst Brian McGough added Canada Goose to his "Best Idea" short list last week. He is presenting a deep-dive "Black Book" on GOOS on June 5th outlining the short thesis and why he believes substantial downside remains.

If you are an institutional investor interested in joining the call email sales@hedgye.com for access.

Below is a snippet from a research report from our Retail analyst team written this morning.

|

GOOS (Best Idea Short) didn’t quite put up what a $49 stock trading at 24x EBITDA needed. Beat by $0.04 but missed revenue slightly. Upcoming year EPS guidance of ‘at least 25%’ vs the Street at 28%, with revenue growth of ‘at least 20%’ which is simply not enough – especially with the Street at 27%. To be clear, I think the problems that this brand faces go far beyond a weak guide and a 15% pre-market sell off. There’s 1,000bp downside in risk to margins embedded in this model as it transitions away from its core jacket into innerwear/knitwear – something that wholesalers don’t want (I had a call with a private outwear buyer in Canada yesterday noting that wholesalers -- and presumably consumers -- have little appetite for anything other than it’s core coat offering, and that might even be getting thin. We’re presenting our Black Book on GOOS on Wed June 5th at 12:30 to outline the bear case from here, which I think is powerful. |