“Rational, unemotional investors are very much in the minority.”

-Howard Marks

As Marks went on to write in Mastering The Market Cycle, “the fluctuation – or inconstancy – in attitudes towards risk is both the result of some cycles and the cause or exacerbator of others.” (pg 135)

Do you invest with how you “feel” about market risk? Or do you have a #process that’s built to proactively predict how your competition is going to feel during a change (or Phase Transition) in fundamental macro conditions?

Do you “feel” close to “management”? Or do you embrace the uncertainty associated with Quad 4 and what it did in Q418 to said management teams, their top-down guidance, etc.?

Back to the Global Macro Grind…

I finally sold Energy (XLE) and some of our favorite Pot Stocks yesterday. That decision had nothing to do with my analysts’ fundamental sector or bottom-up research views. Selling Tech (XLK) on last week’s bounce didn’t either.

It had everything to do with what mostly no PM did enough of in preparation for Quad 4 in Q4 of 2018. Even some of our battled-tested and top-performing power-users struggled in Q4 of last year because “Keith, I just didn’t sell enough.”

I’m not trying to antagonize you with my line of questioning about your risk management #process. Having made mostly every mistake you ever will (and publicly #timestamped ones at that!), I’m trying to help you.

If all I do is have you question, refine, and evolve your decision-making #process, that’s a win for both of us.

Since we’re looking for a Quad 4 Scare in Q3, the #process says get out of things that go down in Quad 4 and re-allocate that capital to things that have a higher probability of going up under those macroeconomic conditions. Put simply:

- ENERGY – goes from a LONG in Quad 3 to a SHORT in Quad 4 (and back to a LONG again in Quad 3)

- POT STOCKS – Organic GROWTH = Long in Quad 3 and Short in Quad 4 (and back to LONG again in Quad 3)

Through the lens of The Quads, Tech is no different than Energy and Pot (Cannabis, soh-rry, I’m Canadian, eh). Effectively, you’re selling both inflation and growth expectations, at the same time. Quad 4 is also called #Deflation.

If you haven’t heard of people risk managing their money this way, that’s a very good thing. Imagine your “risk manager” started every portfolio discussion with, “well, looking at the valuation here, I see this position as attractive.”

If you ask me about “valuation” (let’s use Utilities as an example):

A) Oh, you don’t like (read: don’t own) Utilities (XLU) because they are “expensive”?

B) I only like them because they’re getting more expensive, which confirms my Quad 3 and Quad 4 view

To be clear, I prefer lower prices (and Utilities were lower when we told you to buy them in late SEP 2018 alongside what an Old Wall Guy would have to admit were relatively “cheap” REIT and Housing (ITB) sectors too)…

But Mr. Market isn’t going to give you lower Treasury Bond and Bond Proxy prices during a Quad 4 Scare.

Moving along to what most Valuation Experts generally accept and understand about “stocks”...

A) If a company has a peak stock price based on peak earnings growth and earnings #slow… or

B) If a company with cyclically #slowing earnings continues to guide lower and lower…

They’ll probably (especially if their edge is “meeting with the companies”) either short the stock ahead of that news and/or wait to buy it until they see the Street’s reaction to that news.

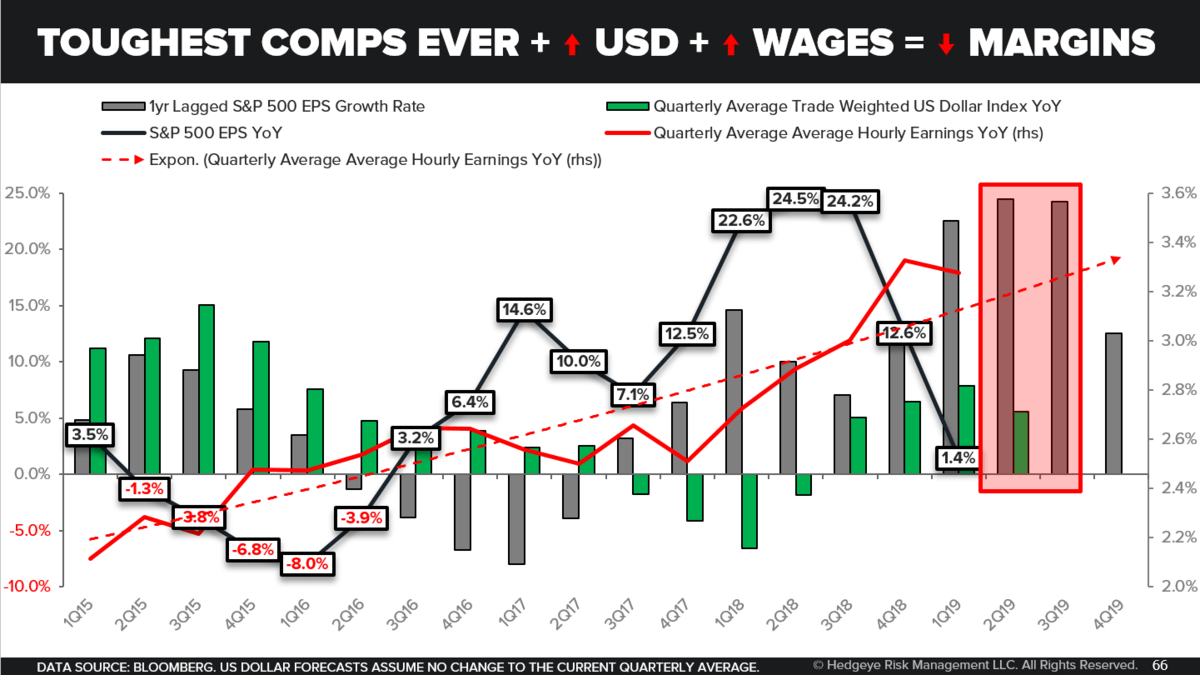

I look at countries the same way my analysts look at companies. Instead of the top-line (SALES Growth), I measure and map Real GDP … and instead of EARNINGS Growth, I use INFLATION as a proxy for COGS and margins.

I also constantly measure and map the ROC of bottom-up SALES and EARNINGS growth for SP500 companies:

A) So far 463 of 500 companies have reported aggregate (year-over-year) EPS growth of +1.41%

B) TECH (57 of 68 companies) has reported aggregate (year-over-year) EPS growth of -7.16%

Yes, it is true that Q1 Earnings Season was “better than expected” (i.e. not yet negative year-over-year), but it’s also true that Tech Earnings are not only NEGATIVE, but the most NEGATIVE they’ve been throughout Earnings Season.

Up next: Tech gets to compare against #PeakCycle EPS Growth of +32.1% year-over-year from Q2 of 2018!

I’m not just “Selling Tech” ahead of a top-down Quad 4 Scare in Q3. Since we haven’t had #PeakCycle Tech compares like this since Q2/Q3 of 2000, I’m simply doing what Howard Marks himself called The Most Important Thing.

And that’s “knowing where we stand in various cycles.” Ladies and gentlemen, we are standing against The Peak.

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND signals in brackets) are now:

UST 10yr Yield 2.34-2.47% (bearish)

SPX 2 (neutral)

RUT 1 (bearish)

Utilities (XLU) 57.04-59.58 (bullish)

REITS (VNQ) 85.46-88.59 (bullish)

VIX 13.40-21.50 (bullish)

USD/YEN 109.10-110.81 (bearish)

AAPL 178.99-191.03 (bearish)

GOOGL 1113-1184 (bearish)

NFLX 339-361 (bearish)

TSLA 196-226 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer