Below are analyst updates on our seventeen current high-conviction long and short ideas. Please note that we added Pinterest (PINS) to the long side of Investing Ideas this week. We also removed McDonald's (MCD) from the short side. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

GTBIF

Click here to read our analyst's original report.

Brands, brands, brands. You hear it all the time in this industry, “we are going to build a national brand!” But who is actually doing it? Green Thumb (GTBIF) is focused on both a wholesale and retail model. They want to provide the best possible experience to the consumer, so supplying both their own, and third-party brands is critical. Along those same lines, selling their top-notch brands such as rythm and Dogwalkers through the wholesale market to spread their distribution across more doors is core to their strategy. These are brands that have a consumer appeal and a use case that is very apparent, that’s how large CPG companies build brands, so we are confident this strategy will persevere in this industry.

Another critical component to our diligence process is corporate governance and focus on shareholder value. GTI executives are focused on long-term value of their equity, not on taking huge salaries, they are for the most part seasoned executives with secure financial positions. GTI also displayed a solid understanding and respect for four-wall economics, as traditional restaurant analysts this is music to our ears.

There are roughly 330M people, with an estimated black market cannabis spend of $50B, that is ripe to be harvested through the new legal market. Through their brick and mortar locations, the U.S. MSO’s represent the entry point to legal cannabis, giving them a leg up from a sales and long-term branding perspective. GTI is our first best idea long in the US space as we feel they are one of the best positioned MSO's.

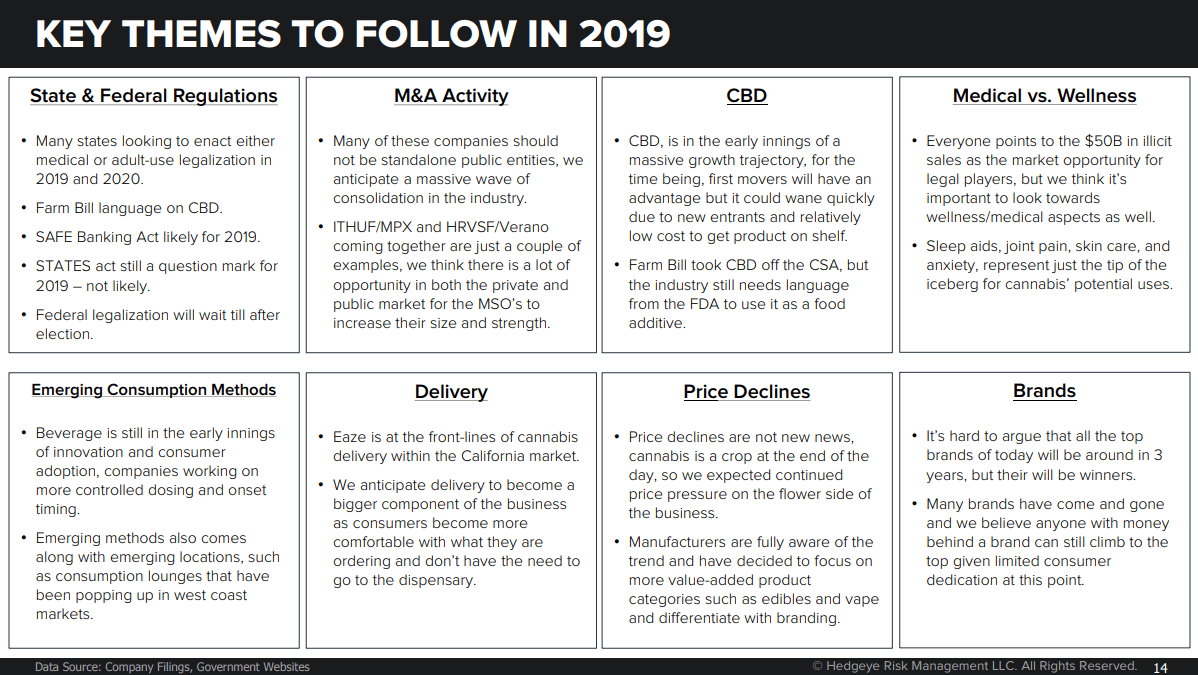

Below are a number of themes we're following in 2019 regarding U.S. legality...

AMN

Click here to read our analyst's original report.

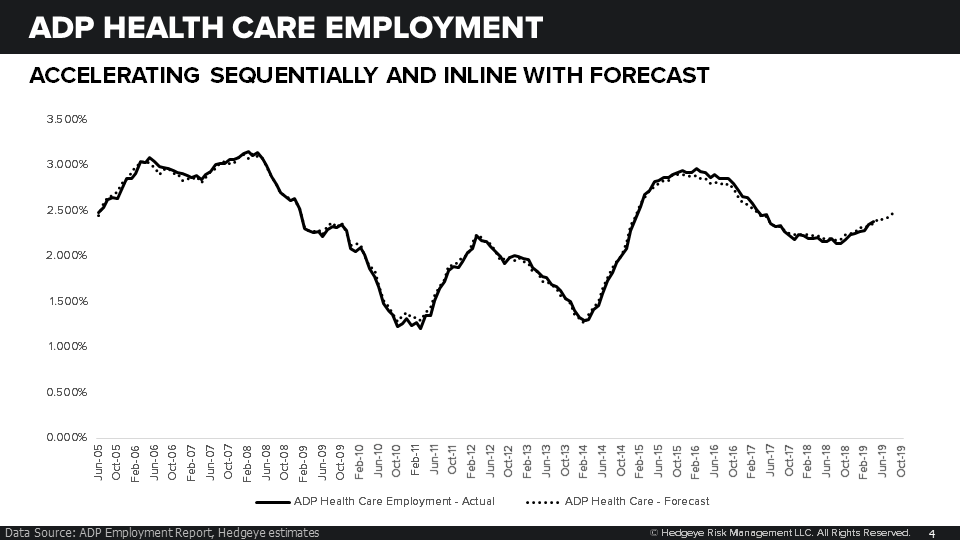

We use BLS employment and consumption series as an indicator of demand and pricing for Health Care services, among other things. For April 2019, Health Care employment accelerated in line with our forecast to +2.4% and continues to point to continued improvement through the remainder of 2019. We are optimistic that AMN Healthcare (AMN) should continue to benefit from increasing demand for Health Care labor.

One of the key themes we’ve identified in Health Care is accelerating wage inflation for medical workers. This creates an interesting set up in 2019 where incrementally positive patient volume could be offset by an extremely tight health care labor market, especially for RNs. For a temporary health care staffing company like AMN, the result should be decidedly positive.

CNQ

Click here to read our analyst's original report.

Canadian Natural Resources (CNQ) | 1Q19 | Consistent Execution

- CNQ generated ~C$1.4B in FCF before changes in WC; repurchased 10.7MM shares (C$400MM) through May ‘19. Fair Value ~C$45 – C$50 per share.

- Though CNQ is light on fundamental catalysts, we continue see it as one of the most compelling opportunities on the long side in energy today. The business is on the back-end of a 10 year CapEx cycle, retains high FCF margins due to low operational costs and bitumen upgrading operations, has a repeatable, low decline asset base, and is shareholder focused.

- All in all, a rarity in North American E&P. Additionally, we see it as an interesting way to play our Macro Team’s call that Quad 3 and Long Energy will be a persistent theme over the coming quarters.

- Efficient Oil Sands Mining Operations…… As fixed costs are a significant portion of the oil sands mining cost structure, high utilization rates are critical in maintaining low production costs per unit. Capacity utilization has remained strong at CNQ’s mines, averaging 100%+ since CNQ acquired AOSP in 2Q17.

We value CNQ on a DCF methodology and arrive at a fair value of C$45 – C$50 per share based on a commodity price range of $50 - $60 WTI and normalized WCS differentials of 25 – 30%. At current strip prices, we estimate CNQ will generate ~C$5B – C$6B of FCF, a ~10 – 12% yield at current equity prices.

ITHUF

Click here to read our analyst's original report.

iAnthus Capital (ITHUF) unveiled their new national dispensary brand “Be.” recently at the Canaccord cannabis conference (press release HERE). At this stage of the cannabis industry there are very few real strong brands especially with a national presence, so despite iAnthus being late to the game from a dispensary branding perspective we are not worried about what they can achieve with this new brand.

ITHUF has access to 11 states and licenses to build 63 dispensaries and 593,000 sq. ft. of cultivation space. As we stated when we first went bullish on ITHUF, they have a proven ability to roll-up licenses and put them on their platform, look for 2019 to be the year they get the locations under one brand, and start to expand on branded product platform.

WTRH

Click here to read our analyst's original report.

While Waitr Holdings (WTRH) got hammered during the UBER roadshow (Uber Eats being positioned by The Bears as a competitive threat), WTRH signaled immediate-term TRADE #oversold (again) this week. Restaurants analyst Howard Penney thought their quarter and revenue guidance was solid. He really likes the management team too.

We like WTRH for three key reasons:

- The growth in the delivery industry

- A strong business model driving strong relationships with restaurants and consumers

- M&A – WTRH is looking to build out a strong restaurant/delivery ecosystem

When we look at the future of chain and independent restaurant operators, it will be important for delivery providers to be a single vertically integrated service that can fulfill all the needs of its restaurant partners. WTRH has a strong start with a tablet in every restaurant and local teams on the ground to focus on the convergence of services.

THC

Click here to read our analyst's original report.

We reiterate our long thesis on Tenet Healthcare (THC).

- The #MedicareforAll theme, economic growth concerns (Quad 3/4), rotation out of Health Care stocks, UHS's mixed results and commentary on 1Q19, have all been banging THC and the Health Care group around the last month.

- Heading into the earnings print expectations for THC appeared low given an EV/EBITDA multiple of ~7.0X and a price that had fallen -26% from $31 and its YTD high on April 10th. THC's 1Q19 results should provide some relief.

- We continue to like the turnaround story of divestitures and cost controls in a secular backdrop of rising Outpatient/ASC mix which we detailed on our Black Book presentation 11/5/2018.

- We've been making progress testing methods to forecast key metrics for THC and other companies using a machine learning methodology against proprietary and public data. These methods suggested upside to 1Q19 Hospital same facility adjusted admissions versus consensus expectations.

- While the differences are small, direction matters given a half a turn in the EV/EBITDA multiple is worth ~$13 per share. The +0.6% reported same facility adjusted admissions were 120 bps better than -0.6% consensus and impacted by a weak flu season by -0.6%.

- In addition, the results were likely negatively impacted by service line closures and what we believe has been a weak maternity trend in 1Q19, although details were not given.

- Cost controls were solid although given the impact of divested assets makes a true comparability difficult. Given the prevailing wage environment, a tight nurse labor supply, and accelerating Health Care wage growth, the operating cost results appear solid.

DLTR

Click here to read our long Dollar Tree (DLTR) stock report sent by Retail analyst Brian McGough to Investing Ideas subscribers earlier this week.

SNE

Click here to read the long Sony (SNE) stock report sent by Technology analyst Ami Joseph to Investing Ideas subscribers earlier this week.

EXP

Click here to read the long Eagle Materials (EXP) stock report sent by Industrials analyst Jay Van Sciver to Investing Ideas subscribers earlier this week.

PINS

We are sticking with Pinterest (PINS) as a long, but keeping it on a short leash following 1Q19 earnings. While 1Q19 results were modestly better than expected on revenue and adjusted EBITDA, management's in-line revenue guidance for 2019 is forcing us to revisit some key assumptions in our model that supported the more bullish scenario.

After stress testing our assumptions, however, we still have a hard time getting numbers down below the high-end of the revenue guidance range. Other than us being completely wrong, we debate whether management is just being conservative and setting themselves up to beat-and-raise. Given the upside we see to guidance and our long-term thesis in-tact, we are willing to stick around on the long side.

TSLA

Click here to read our analyst's original report.

Industrials Sector Head Jay Van Sciver's original Tesla (TSLA) short thesis posited that the unlimited demand the growth bulls were relying on was likely to evaporate in early 2019 when the Federal tax credits began phasing out. And 2019 would coincide with rivals rolling out new electric vehicles to compete with Tesla. Since then, Jay has validated and expanded the diminishing demand thesis with proprietary alternative data tracking fewer test drives, and fewer app downloads, and the company has confirmed demand drying up with successive price cuts and capex cuts.

The recent Q1 earnings report shows that sales are nowhere near where management guided even three months ago, and the stock continues to tumble. Jay thinks there’s still plenty of downside in the stock, especially since the company has more than $15bn in debt, and no earnings.

ROL

Click here to read our analyst's original report.

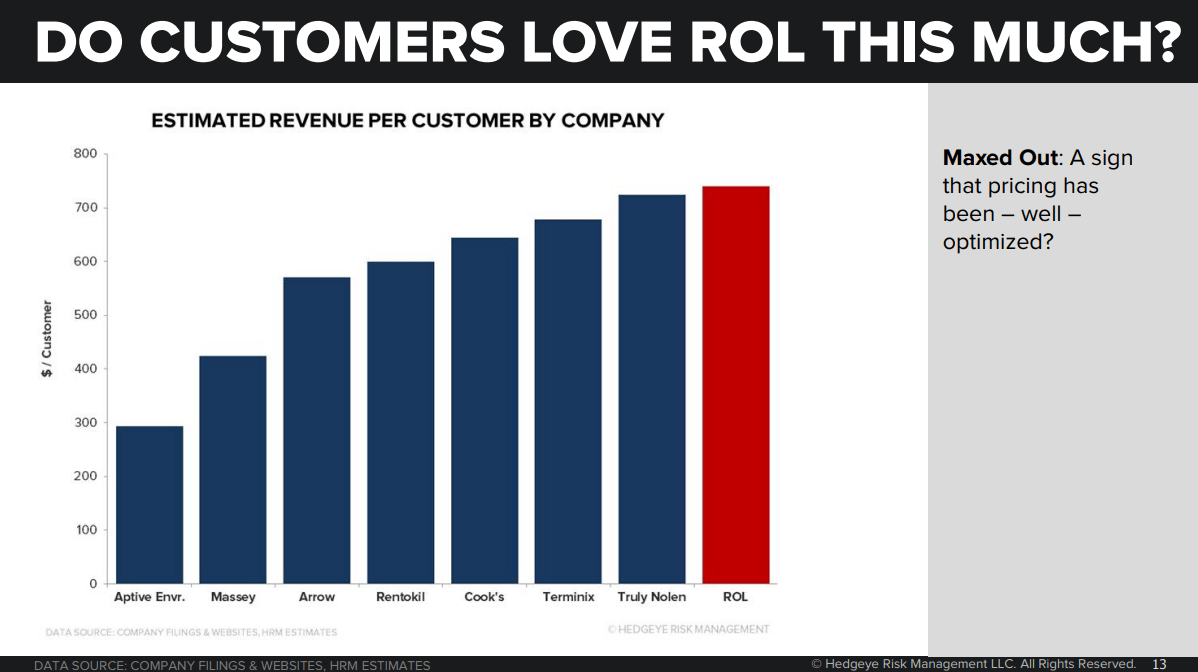

The current share price of Rollins (ROL) makes little sense to us, and we expect a significant downward revaluation by the market.

- Margin gains have stalled amid increasing competitive intensity in a mature, slow growing market.

- Attractive markets for growth and acquisitions – those where route density offers cost advantages – present less runway and higher transaction prices.

- Acquisition spending targets customer contracts, with acquisition spending likely best viewed as an alternative to advertising or other expensed means of growing the customer pool.

With GDP-type organic growth rates, housing headwinds, competitive entry, and a feuding family with a controlling stake, one would reasonably expect ROL to trade at a discount to the market. We expect a growth deceleration, consolidation of leases, a host of yellow/red flags, and broader coverage to generate -50%+ downside, as the S&P 500 addition premium fades from the share price.

DVA

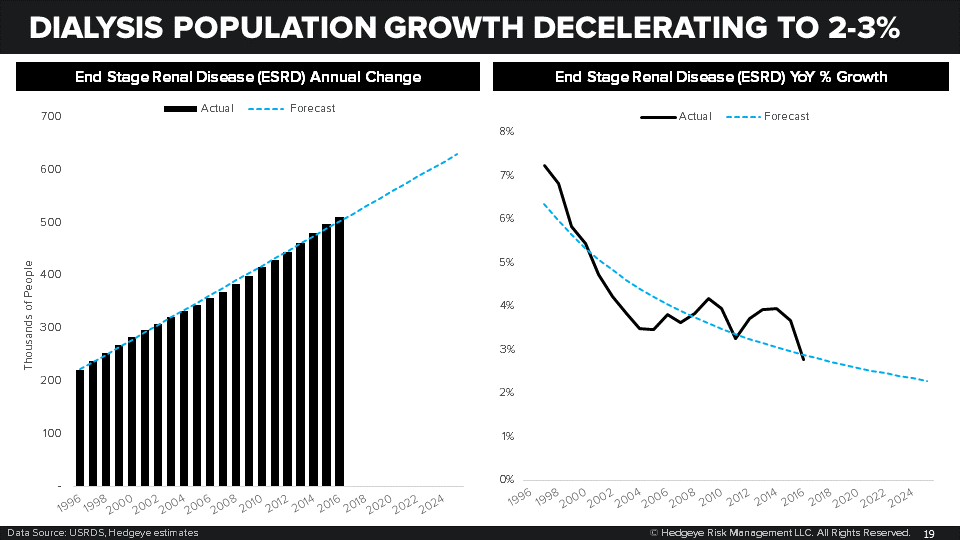

Click here to read our analyst's original report.

The DaVita (DVA) outlook is sufficiently negative. We believe the challenges for DVA are structural in a post roll-up era.

Patient volume was lower than consensus and management expectations. A key driver of our short thesis is our patient and mix model that calls for 2-3% market growth largely coming from growth in the Medicare population, volume that carries a negative margin. While FMS showed 4% volume growth, DVA reported growth of 2.9% volume on a per day basis and 2.4% adjusted, essentially in line with our expectations. Management addressed the volume questions by commenting on share losses and competitive de novo sites. We are at the end of a 20 year roll up in dialysis with 2 large competitors, very little unconsolidated, and excess capacity overall.

TXRH

Click here to read our analyst's original report.

This is a reset year for Texas Roadhouse (TXRH)! How often do you see a casual dining company say that labor inflation is accelerating because traffic growth is better than planned? High quality problem I guess, but the company needs to invest in much needed infrastructure investment to support growth.

TXRH is unique in the restaurant industry for its consistent growth in customer traffic. Still, TXRH will be running 3.2% pricing in 2019 vs 1.3% in 2018. The million-dollar question is, can they maintain traffic growth in 2019 with all this pricing? After the company raised prices aggressively in late 2011 and 2012, traffic slowed meaningfully for the next two years.

EAT

Click here to read our analyst's original report.

We have been saying for months now that the aggressive discounting at Applebee’s is disrupting the Casual Dining industry. One quick example of how the value discussion has changed over the past 12-months occurred on the Brinker International (EAT) conference call.

During the 2Q18 conference call, the word ‘value’ was mentioned 11 times, and now 12-months later on the 2Q19 call ‘value’ was mentioned 38 times. Driving the value proposition for Chili’s is the 3 for $10 platform and we heard that the program “is a relevant and compelling offer that's sustainable into the foreseeable future.” If this is to be true, what will the margin structure of the company look like going forward?

PENN

Click here to read our analyst's original report.

"To be clear on the risk management #process, we have plenty of short ideas - I just don't send you signals to short more of them when both they and SPY are at the low-end of their respective @Hedgeye Risk Ranges," Hedgeye CEO Keith McCullough wrote this week. "Penn Gaming (PENN) remains a Quad 3 Short."

Here's a summary excerpt from Todd Jordan on the thesis:

“PENN remains challenged by its financial structure and secular, macro, and competitive headwinds. We measure a number of proprietary regional gaming metrics and demographic trends that have implications for regional players. Many of these threats are unknown or underappreciated by the Street.”

Here's more from Jordan regarding the most recent quarter:

"While management may provide an optimistic view on April trends on the conference call, we still believe April GGR will decline for the mature markets. Revenue expectations (ex Greektown) may still be too high for the rest of 2019 for PENN. As a result, EBITDAR guidance may be cut again later this year despite higher PNK synergies."

UNH

Click here to read our analyst's original report.

Our Healthcare team maintains its short call on UnitedHealth Group (UNH) based on rebate rule changes, structural headwinds to Medicare Advantage enrollment growth, near term risks of accelerating utilization, and an unfavorable economic growth and stock market environment.