THE HEDGEYE EDGE

Penn National Gaming (PENN) remains challenged by its financial structure and secular, macro, and competitive headwinds.

We measure a number of proprietary regional gaming metrics and demographic trends that have implications for regional players. Many of these threats are unknown or underappreciated by the Street, in our opinion.

For PENN especially, fierce competition is coming, which will significantly impact its Plainridge property in Massachusetts and Penn National casino in Pennsylvania.

Regional gaming did inflect in 2017 but even with such a robust macro environment in 2018, revs only grew 1% YoY. Total regional gaming admissions haven’t grown since 2015 despite Mississippi soaring 7% in 2H 2018.

Poor demographics, rationalization of marketing, and competition from Native American casinos and other non-traditional operations continue to weigh on patronage.

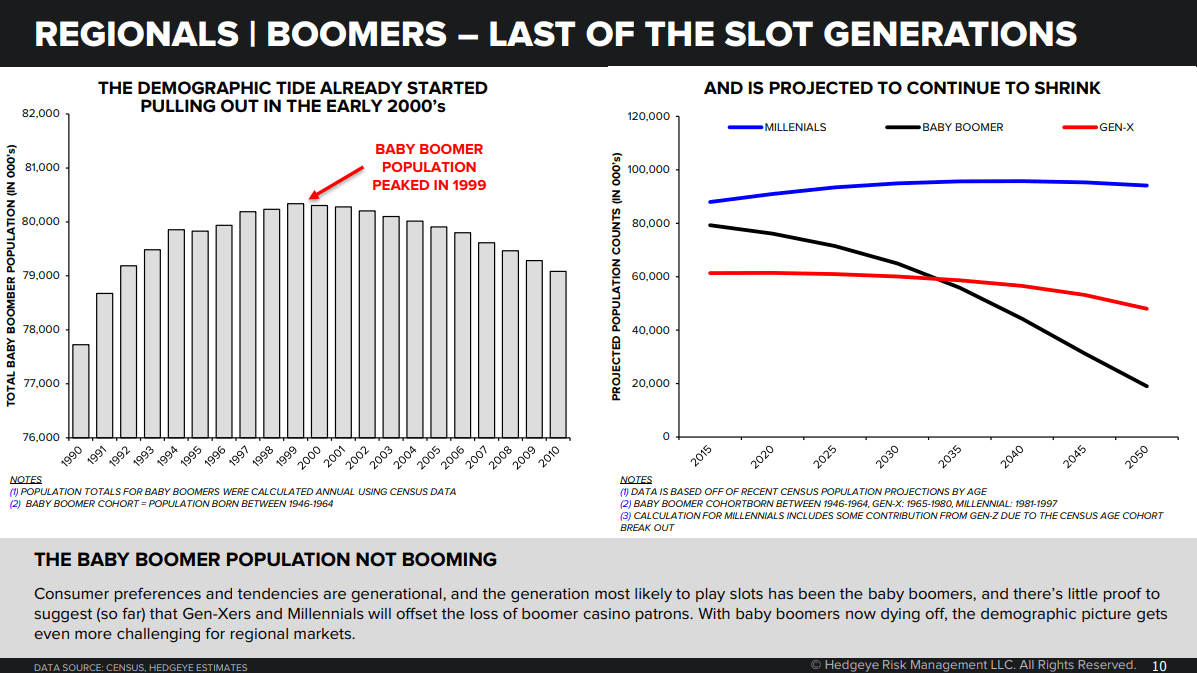

Though there is not a ton of data, our research suggests that the average age of casino patron is 50+ years old. We suspect (from past surveys) the average age of a regional gamer is much older and primarily a Baby Boomer contingent. This is a major challenge for casino operators, and will continue to be so moving forward as population growth in these demographics continues to slow and eventually will turn negative.

Consumer preferences and tendencies are generational, and the generation most likely to play slots has been the baby boomers. There’s little proof to suggest (so far) that Gen-Xers and Millennials will offset the loss of boomer casino patrons. With baby boomers now dying off, the demographic picture gets even more challenging for regional markets.

As not-traditional casinos and slot operations have proliferated, and bad demographics take a toll, casino operators have done what they can to increase productivity of their assets. Reducing slot count and table counts has been a lever that they continue to pull. Still, the casinos would rather experience higher visitation and revenues than shrink operations.

Regional gaming operators have introduced “tighter” games and now offer the worst player odds in the country. How much higher can it go? Over the last few years, slot hold seems to be flattening, suggesting the revenue growth (all of it) associated with slot “price” increases may be less of a tailwind going forward.

Casinos have gotten smarter with target marketing programs and promo allowances, contributing to lower admissions, but higher win and profitability per visitor. They’ve been culling the less profitable bottom end of the database for a few years now. This formula has worked, but we believe the casinos are in the late innings of this strategy. How many more customers are unprofitable? It seems unlikely there are many more. Looking ahead, bad demographics, (potentially) a leveling off of hold %, increasing competition in certain markets, market saturation, and a waning impact from macro growth could be too much to overcome.

Given the overwhelming leverage provided by Penn National Gaming’s OpCo structure, significant multiple contraction is possible as investors come to appreciate the impact of flattish and even negative revenue growth. There are pitfalls to Penn’s current financial structure.

PENN’s 16% 2020 FCF yield is significantly inflated by its high leverage. If we normalize the leverage ratio to be more in-line with other operators, that FCF yield shrinks dramatically. Under this comparison, LVS with a leverage of 2x, commands over 8% in FCF yield, compared with PENN’s 5%. Moreover, PENN will likely pay no federal taxes until mid-to-late 2020 given its ~$270m NOLs. Their state NOLs are $382m post the PNK acquisition. This adds ~30bps more to the FCF yield.

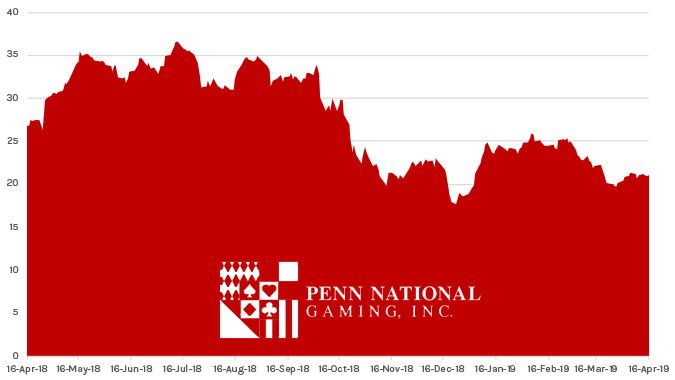

ONE-YEAR TRAILING CHART