Below are analyst updates on our fifteen current high-conviction long and short ideas. Please note we added Tenet Healthcare (THC) to the long side and Brinker International (EAT) to the short side of Investing Ideas this week. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

IDEAS UPDATES

GTBIF

Click here to read our analyst's original report.

Green Thumb (GTBIF) is a U.S. MSO headquartered in Chicago, IL, founded in 2014, focused on building both a wholesale and a retail platform across the most attractive medical and adult-use states. GTBIF is focused on putting the consumer first in all aspects of their business, very similar to a traditional packaged goods company, they do this through brands that resonate and have clear meaning, as well as a very inviting retail experience. GTBIF currently has exposure to 11 states (including proposed acquisition of Integral Associates), with 83 retail licenses and 13 production facilities.

GTBIF plays in most of the critical states currently, but is still leaving critical states such as Arizona, on the table, there are some assets for sale there that we wouldn’t be surprised to see them acquire. Looking out further into the future, it wouldn’t be surprising to see them enter more solidified markets such as Washington, Oregon and Colorado through the wholesale channel. Ben Kovler mentioned on the 3Q18 call, that when states flip from medical to adult-use, they experience triple-digit increases in same-store sales.

AMN

Click here to read our analyst's original report.

There continues to be a good long thesis with AMN Healthcare (AMN) despite the disappointing 4Q18 results and 1Q19 guidance. We'd be more concerned if the market dynamics were not as strong as they are; health care wage growth is accelerating, health care hiring and job openings are accelerating, and our model continues to forecast improvement in utilization. Pricing improved in Nurse and Allied sequentially on a one year and two year basis in 4Q18 as the premium placement trend continues to stabilize.

CNQ

Click here to read our analyst's original report.

On Canadian Natural Resources (CNQ) 4Q18 & 2018 Results….. Despite differentials of ~$40 / bbl for WCS and $21 / bbl for SCO, CNQ produced ~C$47MM of unlevered FCF in the quarter and ~C$200MM of FCF after working capital and other cash adjustments. The strength of the company’s updgraded mining operations remained strong, producing 447 Mb/d, ~C$350MM in unlevered FCF, and declining production costs which fell below C$20 / bbl for the first time in the company’s history. In 2018, CNQ generated ~C$5.5B of FCF, paid ~C$1.6B in dividends, reduced debt by ~C$1.8B (net of USD gross up), and repurchased C$1.2B of stock. The company reaffirmed 2019 CapEx and production guidance, increased the quarterly dividend by 12%, and maintained it’s 50% debt reduction / 50% share buyback capital allocation policy.

ITHUF

Click here to read our analyst's original report.

iAnthus Capital's (ITHUF) strong management team was further strengthened by the MPX acquisition due to the addition of Beth Stavola to the team, she is a pioneer in the industry and a true asset for iAnthus. Noticeably, a CMO is currently not on the team, they have someone locked in that is going to be announced at the end of March. Once the CMO is named, they will be releasing a new national retail brand and we are also looking for them to get more aggressive about product branding, Beth also brings experience on this front.

WTRH

We believe the growth of delivery globally in the restaurant industry will be significant, and there are going to be several ways to play the space. Internationally, we like Just Eat and Takeaway.com, while in the USA, GRUB has a significant advantage over its rivals. That's why we added Waitr Holdings (WTRH) to Investing Ideas as a long.

WTRH has about 2.0 million active diners across Waitr and the newly acquired Bite Squad. WTRH has an EV of $800 million and revenue estimates of $250 million for 2019. WTRH is off to a strong start and has a solid management team and backers to become a significantly bigger company.

THC

Below is a note written by CEO Keith McCullough on why we added Tenet Healthcare (THC) to the long side of Investing Ideas earlier this week:

|

Looking for longs that are A) selling off to the low-end of my @Hedgeye Risk Range on B) #decelerating volume? Tenet Healthcare (THC) fits that profile and remains one of Tom Tobin's Best Ideas (Institutional Research product); Here's a summary excerpt from one of Tom's recent research notes on why: "Our THC long thesis continues to call for accelerating volume, in a macro environment that favors domestic health care services exposure. We also like the mix of Ambulatory, particularly USPI, given the positive policy tailwinds." Buy on red, KM |

CCL

Click here to read our analyst's original report.

Carnival (CCL) printed 0.5% net yield growth in Q1 2019, slightly below Street expectations. We also expected better results but Asia (ex. China), and Europe to a lesser extent, was weaker than we modeled. Excluding the $323m due to new accounting, gross yields fell 1.6% YoY, exactly in-line with our estimate, and revenues (adjusted for the accounting) were in-line with us but higher than the Street. Lower ticket yields offset better onboard yields.

Commissions/transportation/other costs were 4% lower than we modeled. Q1 EPS was generally in-line with us but beat the Street as many analysts mismodeled D&A expenses. Q1 NCC ex fuel was lower than expected mainly due to timing of expenses between quarters.

Looking ahead, Q2 2019 flat yield guidance was in-line with our expectations but below the Street. FY yield guidance of 1% was unchanged.

Once again, CCL disappointed investors by failing to raise yield guidance. As confirmed by our proprietary pricing database, the slowdown in Europe is not abating, which has put a lid on their yield growth guidance this year. In fact, 1% yield growth is not that conservative considering all the uncertainties facing the company. CCL is experiencing multi-year yield deceleration, market share losses particularly in the contemporary segment, and negative FCF which hampers their ability to raise the dividend and/or increase the level of share repurchases. The last issue should surely concern its investor base.

TGT | AMZN

Click here to read our analyst's original Target report. Click here to read our analyst's original Amazon report.

Last week we hosted our Hedgeye Investing Summit – part of which included Retail analyst Brian McGough and CEO Keith McCullough riffing on retail for 20 min on camera. Click here to watch. Below is the high-level takeaway from that conversation with bearish implications for both Target (TGT) and Amazon (AMZN).

When all is said and done, I think that 2019 will go down as the year where Brick & Mortar pushes back against pure-play online – most notably Amazon – which will ultimately be to the detriment of margins across the board. This is not an overnight phenomenon – as it’s been building for the past two years, but it’s been simply masked by two factors – 1) a multi-year acceleration in US Retail sales, and 2) an 18-month period where incremental dollars broke a long-term trend and accrued particularly to high-margin B&M as opposed to online. In other words, there’s been more than enough growth to go around – and more of that occurred at the (highly profitable) store-level than the consensus thinks, and more than most management teams will admit. If you talk to the CEOs of Walmart and Target, they’ll tell you that leveraging the store as de-facto DC infrastructure while layering on home delivery tops the list of strategic initiatives by a country mile – and we’re seeing the capital deployment back that up. Their mindset isn’t about hitting numbers in a given year – but is about long-term survival in #retail5.0 and should ultimately lead to tempered margins for particular pockets of retail.

The chart below shows how the ramp in the consumer accrued to brick and mortar, which temporarily moderated online competitive intensity within these players. As brick and mortar dollars slow, the online intensity will heat up pressuring growth and margin for the big players in US retail (TGT, AMZN, WMT).

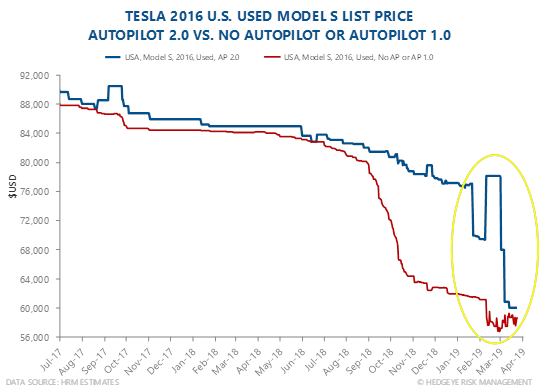

TSLA

Click here to read our analyst's original report.

One consistently valued part of the used Tesla (TSLA) market had been AP 2.0, an argument in favor of a decent valuation for Tesla’s self-driving technology. In the pricing re-shuffle and inventory destock, this premium has collapsed. Causality aside, it looks to be another aspect of the flailing sales strategy of an increasingly isolated management team. Prices in general took a leg down on the mid-February price cut.

ROL

Click here to read our analyst's original report.

We’ve received additional feedback on our Rollins (ROL) short thesis. A few notable inbounds were on the pricing data, which most agreed was on target. ROL is often more expensive, and we suspect longs are underestimating how much of the high multiple depends on ongoing pricing increases.

Many believe that the acquisition strategy, and Clark in particular, can support growth, and discount the potential hurdles of colder weather in the south. ROL is seen as a recession-proof business and remains a name that has rewarded long-term holders.

It will likely take an organic growth deceleration to shake the premium multiple, the catalyst at the core of our short thesis. Given the valuation and obvious risks of the structure, we don’t think it will take a large shift to revalue the shares.

DVA

Click here to read our analyst's original report.

Key drivers of our DaVita (DVA) short thesis are declining to flat growth in commercially insured population on which DVA is disproportionately dependent. Meanwhile the Quad 4 environment of accelerating labor costs is putting pressure on total patient expense, while the pool of acquisition targets has largely been depleted. DVA now faces new challenges to an already deteriorating policy environment. The California legislature will once again take up a bill that would, in effect, limit reimbursement to Medicare rates for patients accepting financial assistance from the National Kidney Fund. We expect the the current EV/EBITDA multiple of 8.8X will violate the long run average of 8.3X, with downside from deteriorating fundamentals and policy environment.

MCD

Click here to read our analyst's original report.

There are a number of structure issues weighing on McDonald's (MCD) and the industry more broadly currently.

Restaurant operators have been continuously impacted by wage rate inflation which remains above both the 5 and 10 year average. Higher wages equal a need to increase prices to maintain margin profile for franchisees, but this is clearly hurting traffic, which is a longer-term problem.

The restaurant industry has a track record of growing faster than both the population and GDP, which is a terrible equation for ever getting traffic growth back. Chipotle along with other fast casual chains have experienced the fastest growth and are undoubtedly stealing share from the QSR's such as MCD, in particular the higher income demographic looking for better/healthier options.

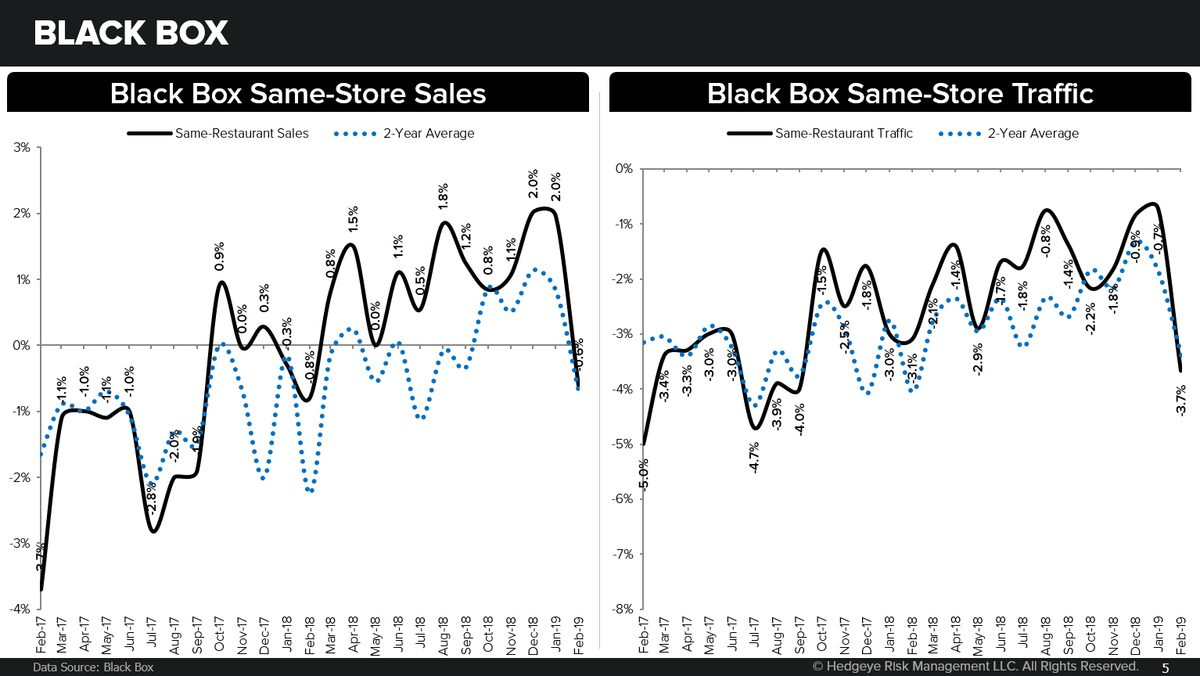

TXRH

We continue to be broadly short the Casual Dining Industry, and that includes Texas Roadhouse (TXRH). We see Casual Dining sales slowing in 2019.

The charts below speak for themselves. The eight-month run of positive same-store sales ended in February with a (0.6%) decline. Weather may be a reason, but I suspect there is more to the decline than just weather. First, one of the biggest issues the industry is facing is aggressive pricing, with guest check up 40bps sequentially to 3.1%. Given the aggressive pricing across the industry, we saw a (3.7%) decline in same-store traffic.

It’s important to note that February was the last month of easy comparisons for the industry. For the balance of 2019, same-store sales increased 1.1% on average per month.

EAT

Below is a note written by CEO Keith McCullough on why we added Brinker International (EAT) to the short side of Investing Ideas earlier this week:

|

Another way to play the same thing (i.e. real consumer spending #slowing as the Fed reflates the cost of living) is shorting the casual dining names that our Restaurants analyst Howard Penney doesn't like. One of those has a great ticker, EAT. Here's an excerpt from one of Penney's often clairvoyant Institutional Research notes: "We have been saying for months now that the aggressive discounting at Applebee’s is disrupting the Casual Dining industry. One quick example of how the value discussion has changed over the past 12-months occurred on the EAT conference call. During the 2Q18 conference call, the word ‘value’ was mentioned 11 times, and now 12-months later on the 2Q19 call ‘value’ was mentioned 38 times. Driving the value proposition for Chili’s is the 3 for $10 platform and we heard that the program “is a relevant and compelling offer that's sustainable into the foreseeable future.” If this is to be true, what will the margin structure of the company look like going forward?" Short the bounce, KM |