The data is getting worse, but the jury is still out until we get past the Easter anomaly. After getting positive datapoints out of both JPM's March subprime unsecured print yesterday and this morning's COF March data (and DFS for that matter), the jobless claims data this morning laid an egg (for the second week in a row). Claims climbed 24k this week, and are now up 42k in two weeks - now 484k. There was no revision to last week's number. The 4-week rolling average rose 7,500 to 457,750. Consensus had expected just 430k initial claims. The chart below shows the rolling average trend line.

The last two weeks of data have been pushing claims farther outside our 3 sigma channel. To be fair, the Labor Department said that there were significant one-time items and Easter-related distortion affecting this week's number to the upside, but that's also the reason they gave last week, which is why the consensus for this week's number was off by a mile. We've said for the last month that we expect claims to improve, and so far we've been dead wrong. We'll reserve more final judgment until we see whether the Labor Department's explanations are valid (i.e. the next two weeks). Census hiring should continue to heat up this month and next. The following chart shows the raw claims data.

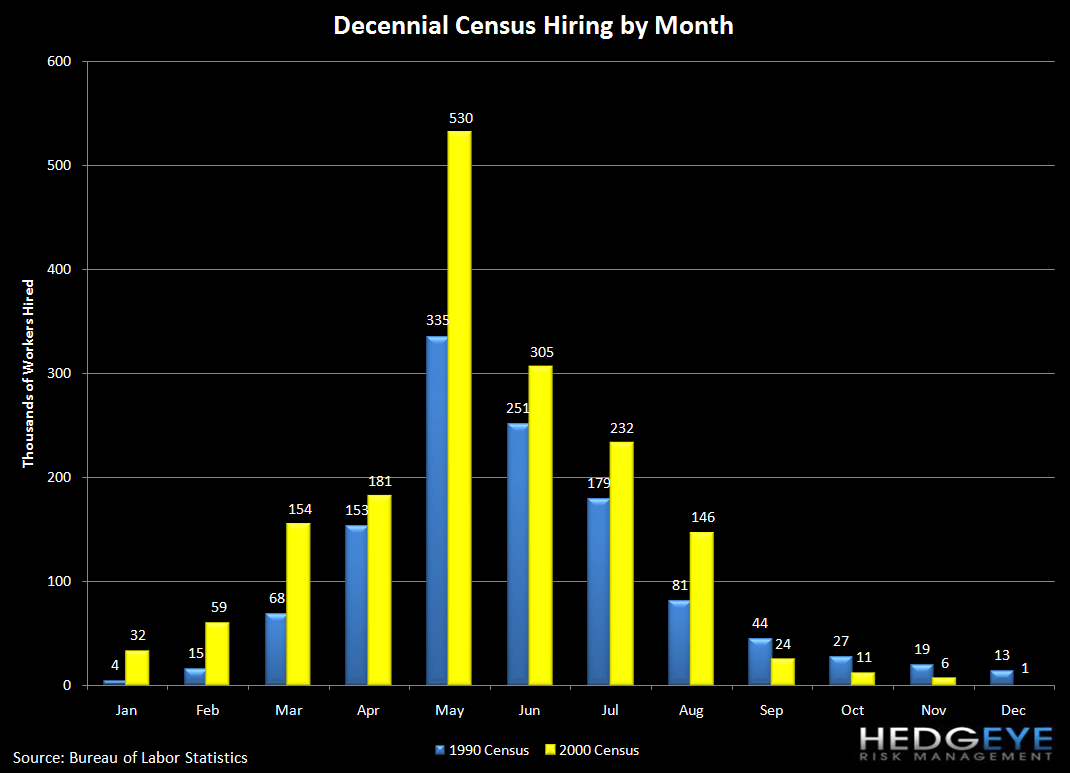

As a reminder, the following chart shows census hiring from the 2000 and 1990 census by month, which should be a reasonable proxy for hiring this spring.

Joshua Steiner, CFA

Allison Kaptur

{kind=link}

{kind=link}

{kind=link}