R3: REQUIRED RETAIL READING

April 5, 2010

TODAY’S CALL OUT

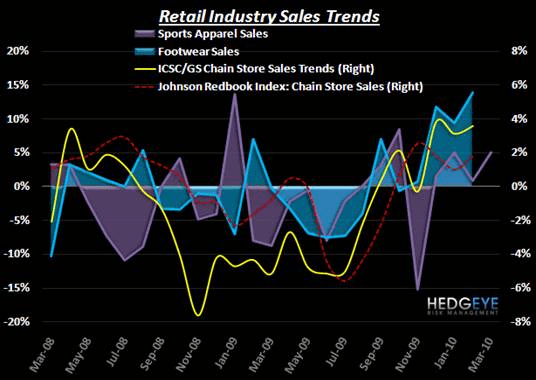

With sales day on the near-term horizon, we released our first monthly Edge on Athletic Trends report capturing the latest market share trends by channel, category, and brand last week. Here are some of the highlights:

- After a long period of underperforming, footwear consistently stood out as a top performer over the past month.

- But over the past two weeks, athletic apparel and footwear have tracked retail in aggregate over the past 2-weeks, suggesting that weather trends are in fact influencing traffic – though all sales remain at a very healthy level.

- We’re seeing Athletic Specialty sales trump Family and Mass channels – exactly what we should see at the start of the cycle we’re seeing develop.

- Nike brand dominating. Jordan status quo. Converse raising yellow flags.

- UA’s numbers will look weak until around the 1Q EPS report.

- The Adibok story hinges on hope and prayer.

- Columbia emerging as potentially good long idea – something to consider into next week’s earnings report.

LEVINE’S LOW DOWN

- Due to overwhelming demand, a sample sale for American Apparel was shut down by police in London. After letting just 100 customers into the event, the unorganized crowd became restless and violent. As people in the crowd began to get crushed, the police stepped in and closed the entire event down. With so many controversial image problems, this yet another black mark for the brand.

- According to Pew Research, in 2008, an estimated 49 million Americans, or 16% of the population, lived in a family household that contained at least two adult generations or a grandparent and at least one other generation. In 1980, this figure was just 28 million, or 12% of the population. The last time this high a percentage of the US population lived in a multi-generational family household was in the late 1950s. Most economist believe the recent recession is the key driver of families consolidating under one roof.

- According to online private sale operator, Gilt Groupe, 7% of the company’s weekend sales are originated from the company’s iPhone app. Interestingly, only 3.8% of consumers used mobile devices to actually purchase goods on Cyber Monday, the busiest online shopping day of the year. It’s no wonder the company has already developed an iPad version of its mobile commerce interface. A bigger and better screen likely means far more shopping…

HEDGEYE CALENDAR

MORNING NEWS

Chinese Labor Squeeze - Chinese labor squeeze could fuel higher apparel prices. A continuing shortage across China’s manufacturing zones, particularly in the lowest-paying jobs, appears to be showing no signs of letting up and could eventually lead to price hikes in Chinese goods as factories are forced to pay higher wages. Labor experts said that as the scarcity of labor increases, companies may need to choose between moving their operations further inland or pay more to attract workers to the Pearl River Delta and other manufacturing hubs. The shortage arose in part because of the government’s aggressive economic stimulus efforts. <wwd.com/business-news>

Stats On Chinese Manufacturing - Nearly 83% of 202 foreign manufacturers in China said that their primary motive for locating there was to access the Chinese marketplace, up from 71% two years ago, according to a recent survey. Yet the survey also shows fewer foreign manufacturers consider China a good export platform for the rest of Asia because of rising labor costs and other factors. <sportsonesource.com>

Japanese Teens Seeing Budgets Tighten - Young people in Japan are some of the most fashionable on the planet, but teenagers and young adults are facing shrinking budgets for apparel and accessories. High school students’ average monthly allowances fell 11.4% in 2009 to $64.68. That’s the lowest level in 19 years. Allowances of university students fell 4%. <wwd.com/retail-news>

Carter’s Launches Two E-Commerce Sites - The children’s clothing manufacturer has launched two e-commerce sites, www.carters.com and www.oshkoshbgosh.com. The sites feature a shopping cart that collects items from both sites, enabling consumers to check out once. <internetretailer.com>

Haggar Clothing Co. Launches E-Commerce Site - Haggar Clothing Co. this week launched an online retail site where consumers can buy such items as pants, shorts, suit separates, outerwear and accessories. <internetretailer.com>

Old Navy Posts a 287% Month-over-Month Traffic Increase in February - Old Navy attracted 6.34 million visitors in February, a 287% increase from February 2008, as it registered the biggest traffic jump among apparel and beauty products during the month, Nielsen NetView reports. <internetretailer.com>

Furniture Retail Orders Up - New retailer orders for furniture rose 4% in January compared with the same month last year, according to the Furniture Insights survey of residential furniture manufacturers and distributors conducted by the High Point accounting and consulting firm Smith Leonard. <hfbusiness.com/news>

Upper Deck and Tiger Woods Items - All the polls might reflect that Tiger Woods is at his lowest approval ratings, but the memorabilia market for Woods' items hasn't cooled in the same fashion. Upper Deck spokesman Terry Melia said that the company will sell range balls hit by Tiger with an autograph in a display case for $499, autographed Black TW Nike hats for $999.99, Tiger autographed 2010 golf cleats for $1,399.99 and the same style Nike Dri-Fit shirt Woods will wear on Masters Sunday autographed for $1,799.99. <cnbc.com>

Children's Trends: Zippers - Zippers are doing double duty this fall. No longer just functional, the metal fasteners are taking on a decorative role, snaked across uppers and cuffs and even twisted into rosettes. <wwd.com/footwear-news>