THE HEDGEYE EDGE

The current state of the cannabis industry can be described as a double bubble. The current valuation of the publicly traded companies participating in the cannabis industry dwarfs the size of the current legal marijuana industry (2018 global legal cannabis sales are expected to be roughly $13B – illicit market is estimated to be $150B globally).

On top of that, there are projections coming from CEO’s of large U.S. publicly traded companies touting the possible TAM in the next 15 years to be $200 billion, and we have heard more bullish estimates of $500 billion from publicly traded cannabis companies. With all the capital flowing into the industry, you now have companies planting enough assets to nearly supply the majority of global demand, all grown in Canada!

The founder of Canopy Growth (CGC), turned a Cannabis start-up into a $14 Billion company in just 4 years - that is a tale you see in the internet and crypto space, not a consumer product company that grows plants. Yes, Cannabis is going to be big business, but it’s not going to be built at internet speeds.

In the early days of Cannabis, just like early days of the internet, the street came up with creative ways to value the industry participants. The internet days had eyeballs or page views as critical metrics. Then the industry matured and fundamentals became paramount. Profitability matters!

Today, the Cannabis industry is still in the stage where profitability doesn’t matter and crazy valuation metrics are rampant (we will go over some of the crazy metrics later in this report). We have focused our stock selection on going LONG the “asset light” models and SHORT the company that has the largest exposure to declining wholesale prices. We put CGC right at the top of this list of shorts.

CANOPY GROWTH = THE EPICENTER OF THE BUBBLE

CGC is a 4 year-old roll-up story, who is the dominate global player in Cannabis. Cannabis is a heavily regulated industry and the largest potential market in the world, the USA, is still federally illegal to operate in and there is no line of sight on it becoming legal.

While CGC has a leadership position in supply agreements and production facilities, it also has the highest cost of production. This will become a problem for CGC when/if wholesale prices begin to decline. If we look at wholesale prices across other regions that have gone recreational, prices have collapsed. The three states in the USA that have been recreational in the USA the longest, wholesale prices are $1.30 to $2.00 per gram versus the current $4.50 in Canada. When Canada becomes oversupplied in 2019/2020, how will the Canadian government respond?

We are putting CGC in a different camp relative to the others in the space. The CEO of STZ justified investing CAD$5B in a 4 year old start up by claiming the Cannabis industry will be a $200 billion dollar industry in 15 years. With that news in the past, now CGC has to deliver the expected financial performance to justify the valuation. Given the shareholder dilution that has occurred over the past three years, CGC is unlikely to generate any meaningful EPS over the next 5 years.

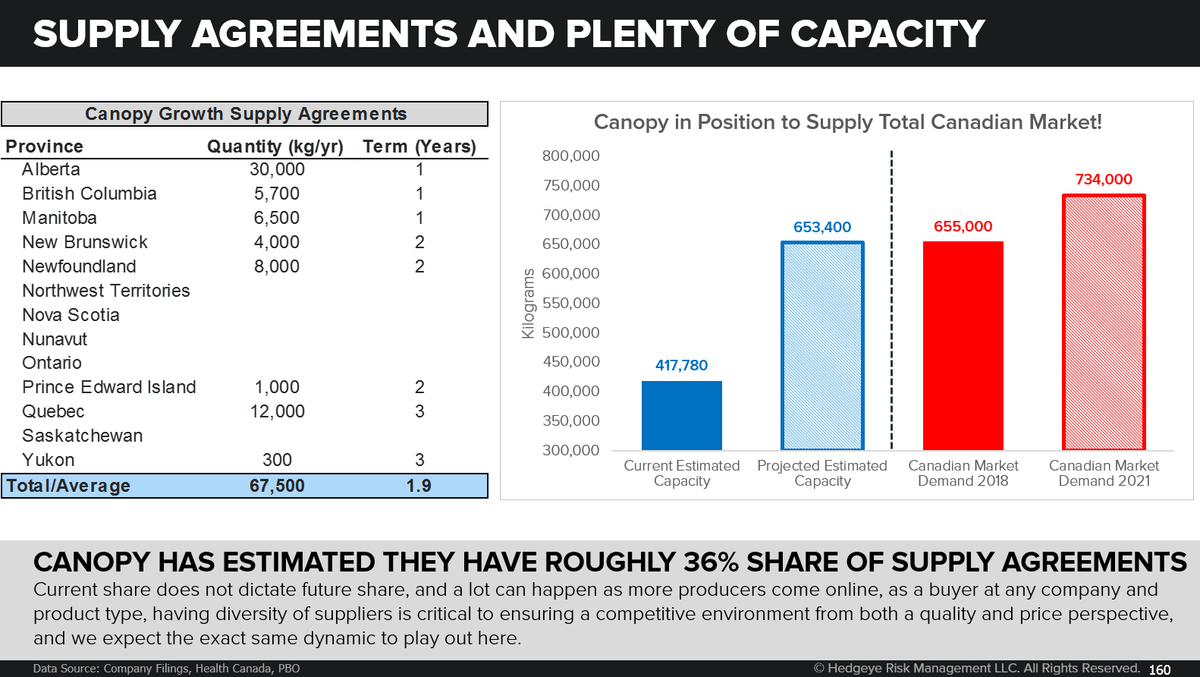

Canopy has estimated they have roughly 36% share of supply agreements. Current share does not dictate future share, and a lot can happen as more producers come online, as a buyer at any company and product type, having diversity of suppliers is critical to ensuring a competitive environment from both a quality and price perspective, and we expect the exact same dynamic to play out here.

ONE-YEAR TRAILING CHART